The recent announcement by China's State Taxation Administration regarding the adjustment of export tax rebates for photovoltaic (PV) products has garnered significant attention across the global market. In this context, a critical question arises: Can non-Chinese enterprises leverage the theoretical increase in Chinese export costs to rapidly narrow the cost disparity with the Chinese supply chain and reshape the competitive landscape?

Source:The State Council Information Office of The People's Republic of China

Currently, there is a significant discrepancy in price and cost between PV products (primarily modules) manufactured in China and those produced in other regions. With the formal cancellation of the export tax rebate for Chinese PV products, the industry is focused on whether this price gap can be closed quickly. According to SMM preliminary statistics, a significant price difference of at least $0.05/W persists between Chinese export modules and those exported from non-Chinese regions such as Southeast Asia and India. The following analysis examines this issue through three dimensions: global supply and demand status, industrial technology strategy, and product manufacturing quality.

Production Scale: Global Supply and Demand Status

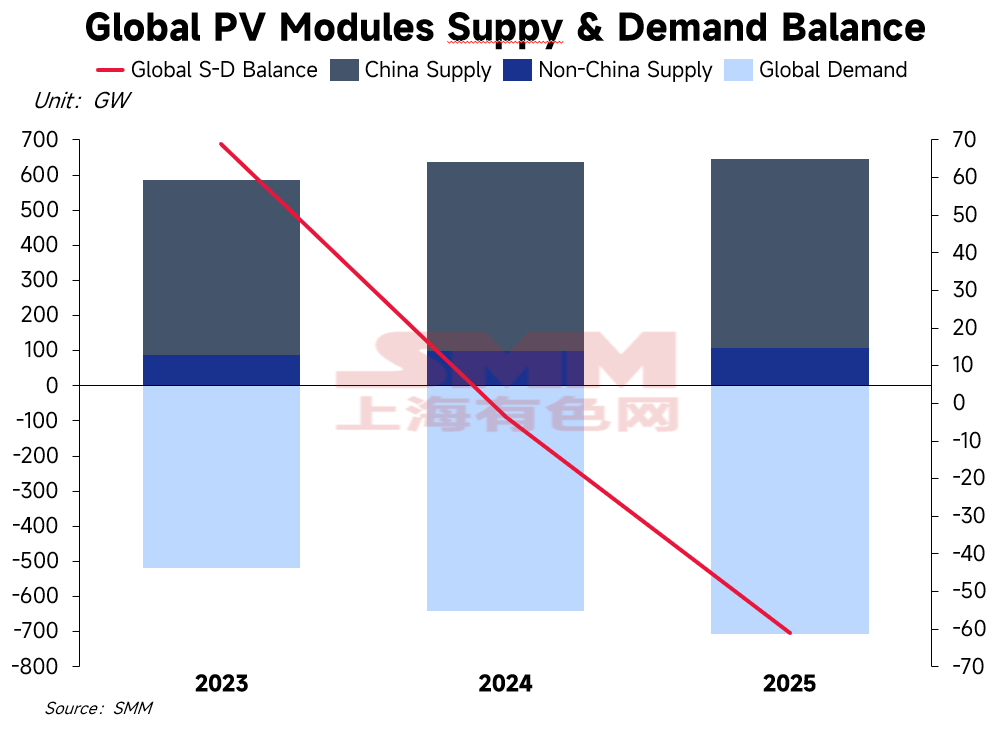

Theoretically, achieving economies of scale by expanding production capacity in non-Chinese regions is an effective pathway to reduce supply chain costs. However, under the current market conditions, this approach lacks commercial viability. The global PV market is currently undergoing a period of supply and demand adjustment, where existing capacity is sufficient to meet market requirements. Without explosive growth in terminal demand, increasing production at non-Chinese bases solely to lower unit costs contradicts basic commercial logic and directly increases the risk of inventory accumulation.

Furthermore, China is the only country possessing a complete PV industrial chain. Its core competitive advantage lies in the cost efficiency derived from industrial agglomeration. From upstream polysilicon and wafers to midstream cells and auxiliary materials, the high geographic concentration of upstream and downstream links drastically reduces intermediate logistics costs and inventory cycles, creating a comprehensive cost advantage that is difficult to replicate.

In contrast, non-Chinese bases often face supply chain fragmentation; the high costs associated with the cross-border allocation of raw materials weaken their overall competitiveness. Simultaneously, factor costs such as labor and transportation cannot be overlooked. China possesses a massive, technically mature industrial workforce and highly developed logistics infrastructure, ensuring extremely high production yields and transport efficiency. Conversely, overseas manufacturing bases require time to accumulate labor skill proficiency and supply chain logistics support. This comprehensive barrier, composed of full-chain synergy and factor cost differences, makes it difficult for overseas bases to offset cost disadvantages through simple capacity expansion in the short term. Consequently, without strong support from new orders, the marginal benefit of increasing output to dilute fixed costs is unlikely to cover potential operational risks.

Technology Output: Core Technology Retention Strategy Maintains Competitive Advantage

In a context where scale effects are difficult to leverage, technology synchronization is theoretically another avenue for cost reduction. However, its implementation faces objective limitations due to the protection of corporate core competitiveness and globalization strategies. Synchronizing core cost-reduction technologies or high-efficiency module production processes to international manufacturing bases would weaken the pricing power of the local Chinese supply chain in the global market.

Competitive advantage in the PV industry stems primarily from rapid technological iteration and precise process control. To ensure commercial returns on R&D investment and maintain product differentiation, leading enterprises generally adopt a strategy of ‘technological gradient transfer.’ This involves prioritizing the deployment of the latest cost-reduction processes and high-efficiency technologies (such as cutting-edge N-type iterative technology) at local Chinese bases, which feature comprehensive R&D support and rapid supply chain responses.

This strategy ensures that new technologies are gradually promoted overseas only after their maturity and yield rates have reached optimal levels, while also controlling the risk of core intellectual property diffusion. Therefore, non-Chinese supply chains primarily receive mature, standardized technologies that have been market-verified over a longer period, rather than the latest generation of processes at the forefront of cost reduction and efficiency enhancement. This commercially based technological hierarchy objectively limits the possibility of overseas bases achieving significant cost reductions through technological leapfrogging in the short term.

Product Performance and Manufacturing Consistency: Objective Generational Differences Between Regions

Although leading enterprises implement a unified quality management system across all global manufacturing bases, objective differences exist in specific power ratings and photoelectric conversion efficiencies between Chinese bases, international bases, and overseas PV module manufacturers.

First, performance differentiation is driven by production line equipment iteration. Chinese production bases serve as the launchpad and concentration point for the latest generation of manufacturing technology. The frequency of production line updates is extremely high, with equipment precision and automation levels at the peak of the industry. In contrast, international manufacturing bases constitute a relatively lagging tier regarding production line upgrades, constrained by investment return cycles and equipment import/export processes.

Taking the 210R(G12R) module as an example: the power rating of conventional modules produced in domestic Chinese bases has stabilized in the 650–660W range, with some ultra-high-power products reaching up to 670W. However, the average power of similar products from overseas manufacturing bases is concentrated around 620W or lower.

This significant drop in power rating directly reflects the generational difference in manufacturing processes. Consequently, even when producing the same type of module, the average output performance of international bases remains universally lower than that of Chinese bases.

Secondly, the maturity of supply chain support significantly impacts product consistency. China possesses the world's most complete supply chain cluster; the supply of auxiliary materials is stable and standards are unified, effectively minimizing module encapsulation losses. In regions like Southeast Asia, auxiliary materials partially rely on imports or require integration with local suppliers. Minor fluctuations in the supply chain can lead to a less concentrated distribution of module electrical performance compared to Chinese bases, resulting in a relatively lower proportion of high-power output. Additionally, enterprises tend to prioritize the deployment of production capacity and R&D resources for products with the highest conversion efficiency and latest technical routes in China. International bases currently undertake the manufacturing of mainstream products with relatively mature technology and stable yields. As a result, non-Chinese manufactured products often lag behind Chinese-manufactured products of the same brand in comparisons of top-tier performance parameters.

Conclusion

In summary, the current price differential between the Chinese supply chain and the non-Chinese supply chain is fundamentally the result of the combined effects of the global industrial division of labor, competitive strategies, and generational gaps in product technology.

From a cost logic perspective, global supply and demand fundamentals do not support blind expansion by international manufacturing bases for the purpose of cost reduction.

From a technology logic perspective, the retention strategy for core cost-reduction and efficiency-enhancing technologies ensures that the Chinese supply chain maintains a sustained cost advantage.

From a product logic perspective, the advantages of Chinese bases in production line equipment and supply chain support enable Chinese-produced modules to maintain a lead in power and efficiency.

Therefore, the cancellation of the export tax rebate has not altered this fundamental industrial logic. The cost and technology gap between Chinese and non-Chinese supply chains is expected to persist in the short term, with rapid narrowing being unlikely.

Written by: Ryan Tey Tze Yang | ryan.tey@metal.com

![[SMM PV News] US Solar Faces Labor Shortage Ahead of 'OBBBA' Deadline](https://imgqn.smm.cn/usercenter/xBtJB20251217171738.jpg)

![[SMM PV News] France Unveils 2026 Solar Auction Calendar and New Supply Rules](https://imgqn.smm.cn/usercenter/CpbPE20251217171736.jpg)

![[SMM PV News] Gulf Conflict Shifts Energy Markets, Impacting 'PPAs' and 'BESS'](https://imgqn.smm.cn/usercenter/xAoMy20251217171743.jpg)