Following the cancellation of China's export tax rebates for photovoltaic products, the global solar trade landscape is undergoing significant restructuring. India, underpinned by massive domestic demand and unwavering policy commitment, is rapidly emerging as one of the most strategic markets outside of China. As a high-growth region with global competitiveness, India accelerated its energy transition throughout 2025, demonstrating remarkable market resilience. By November 2025, India's cumulative PV installed capacity surpassed 130 GW. Notably, the market added approximately 35 GW in 2025 alone, positioning the country as a core driver of renewable energy expansion both regionally and globally.

This analysis reviews the Indian PV sector's performance in 2025 and provides an outlook for 2026 within the new global trade context.

Installed Capacity and Market Structure

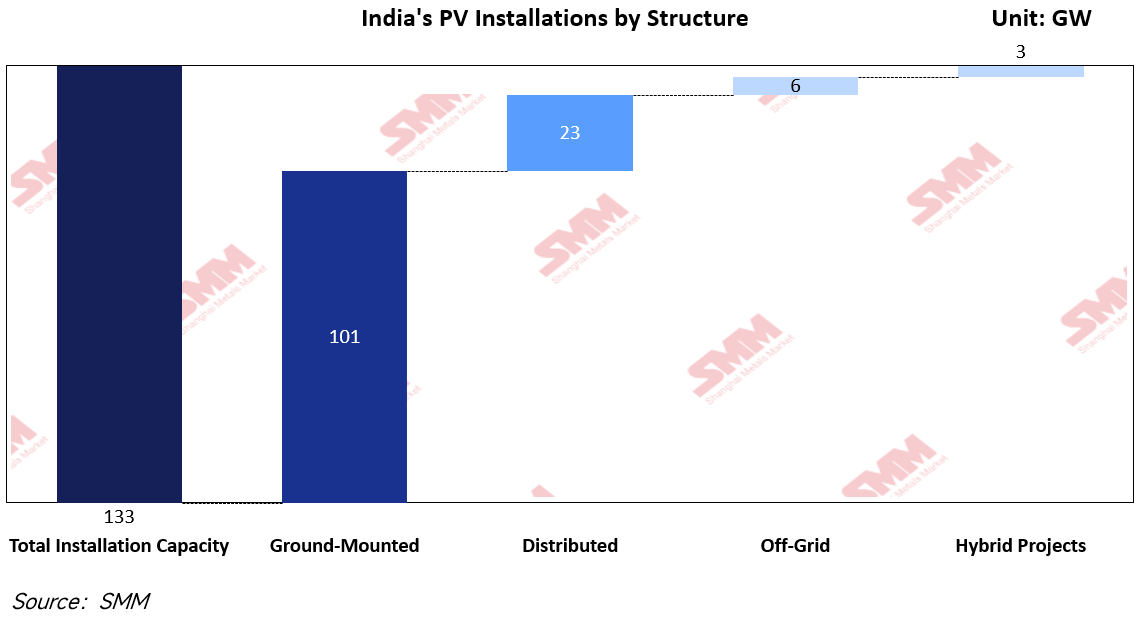

Official statistics indicate that India's cumulative PV installed capacity has reached 132.85 GW. Utility-scale projects constitute the backbone of the market, accounting for 75.8% of the total capacity (approximately 100.8 GW). The remaining capacity is distributed among rooftop solar (23.16 GW), off-grid systems (5.55 GW), and hybrid projects (3.34 GW).

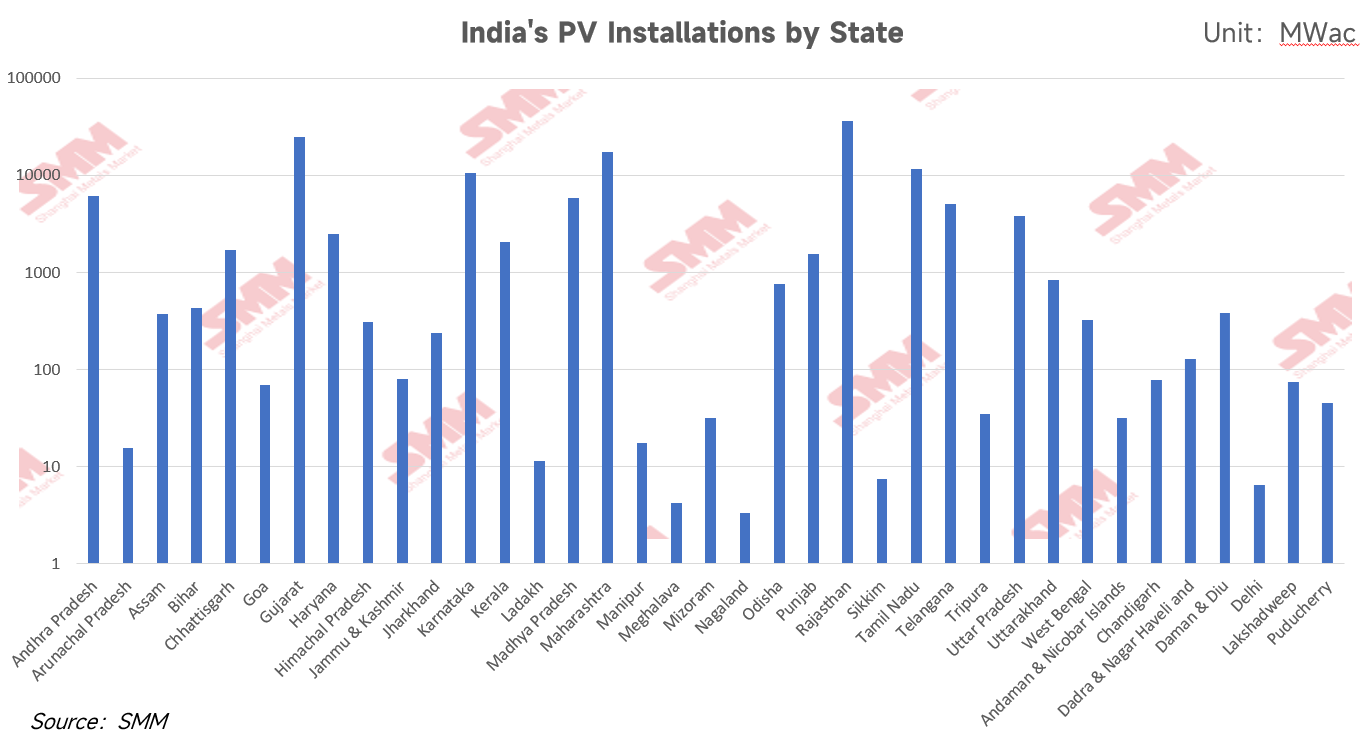

Regionally, industrial clustering is pronounced due to variations in resource endowment and policy direction. Rajasthan, Gujarat, and Maharashtra have established themselves as the leading hubs, collectively accounting for approximately 60% of the national total. Their respective installed capacities stand at 35.91 GW, 24.79 GW, and 17.17 GW.

Manufacturing Capabilities and Supply Chain Dynamics

While India significantly expanded its PV manufacturing capacity in 2025, the supply-demand structure across the value chain remains unbalanced. Module production capacity has exceeded 170 GW, sufficient to meet the majority of domestic demand. However, cell production capacity lags significantly at approximately 29 GW. Furthermore, domestic manufacturing capabilities for polysilicon and wafers remain insufficient to support module manufacturers, resulting in a high dependency on imported raw materials. This lack of vertical integration exposes the supply chain to risks regarding critical mineral export controls and international price volatility.

Price Bifurcation and Trade Policy Environment

Influenced by trade barriers and localization policies, the Indian PV market in 2025 exhibited distinct price bifurcation, with policy uncertainty challenging project economics. According to SMM research, module prices vary drastically based on supply origin. Non-DCR (Domestic Content Requirement) modules maintained a low price range of $0.14–0.15/W. Conversely, due to the scarcity of upstream cell capacity and higher manufacturing costs, DCR modules remained expensive, trading in the $0.27–0.30/W range, showing a price differential of nearly 100%.

As new large-scale government projects are mandated to use modules listed in the Approved List of Models and Manufacturers (ALMM), SMM forecasts that prices for India-made non-DCR modules will likely decrease further. However, if the government moves to completely exclude the Chinese supply chain and enforce strict DCR compliance, solar plant construction costs will rise sharply, potentially eroding the levelized cost of energy (LCOE) advantage of Indian solar power.

Trade Remedy Investigations and Legal Disputes

To address supply chain dependencies, the Directorate General of Trade Remedies (DGTR) under India's Ministry of Commerce previously recommended an anti-dumping duty of up to 30% on Chinese imports. In response, the Rajasthan Solar Association (RSA) filed a legal challenge. The Supreme Court of India subsequently issued an interim order ruling that, pending a final verdict, any tax notification based on this recommendation remains invalid and unenforceable.

While this judicial intervention temporarily preserves access to lower-cost products for developers, the industry remains concerned. The potential future implementation of protectionist tariffs, superimposed on existing Basic Customs Duties (BCD), would increase energy transition costs and potentially delay the achievement of the 2030 targets.

Trends in Project Tendering

In 2025, tender activity evolved toward technologically complex, composite projects:

- Shift in Tender Typology The proportion of standalone solar tenders has declined. The majority of grid-scale tenders now incorporate energy storage systems (ESS) or adopt wind-solar hybrid models to enhance peak-shaving capabilities. Project configurations are accelerating toward highly integrated models such as Round-the-Clock (RTC) and Firm and Dispatchable Renewable Energy (FDRE). Despite increased complexity, winning bid tariffs have maintained a downward trend, driven by significant reductions in storage costs and the optimization of multi-energy complementary solutions. This indicates that leading Indian enterprises have successfully navigated the initial learning curve regarding cost control and technical integration for complex energy systems.

- Tightening of Energy Storage Localization The Ministry of Power has stipulated that energy storage projects funded through Viability Gap Funding (VGF) must satisfy a local content requirement of at least 20%. Additionally, the Ministry rejected waiver applications from several states regarding the "Public Procurement (Preference to Make in India)" (PPP-MII) order, establishing a unified enforcement threshold. While aimed at forcing supply chain localization, the limited availability of compliant supply sources may inflate tender costs in the short term.

Structural Obstacles to Industry Development

Despite the growth in installed capacity, the Indian solar sector faces four major structural constraints at the execution level:

-

Delays in Power Purchase Agreements (PPA): As of September 2025, Power Sale Agreements (PSA) for approximately 44 GW of awarded projects remain unsigned. Fluctuating demand from Distribution Companies (Discoms) and delays in grid construction have extended the cycle from bid award to financial closure.

-

Grid Absorption and Transmission Constraints: High-growth regions like Rajasthan and Gujarat are experiencing delays in the construction of the Inter-State Transmission System (ISTS) relative to generation capacity. This misalignment has resulted in curtailment rates ranging from 10% to 30% in these areas.

-

Supply Chain Uncertainty: The scarcity of upstream raw material manufacturing capability leaves the Indian PV industry vulnerable to external supply fluctuations. Export control policies from major raw material exporting nations pose a direct threat to supply chain stability.

-

Regulatory Volatility: Regulatory instability remains a risk. For instance, certain state-level regulators (e.g., in Maharashtra) adjusted banking and wheeling charge policies in July 2025 (subsequently stayed by the High Court). Such frequent changes increase financial modeling risks for Commercial & Industrial (C&I) and Open Access projects.

2026 Market Outlook

Based on a neutral expectation regarding the implementation of ALMM List 2, SMM forecasts that new PV installations in India will reach approximately 45 GW in 2026. This represents a year-on-year growth rate of 24%, a significant deceleration compared to the robust 41% growth observed in 2025.

The core constraint driving this slowdown is the ALMM List 2 regime, scheduled for mandatory enforcement in June 2026. If domestic cell production capacity cannot effectively meet downstream demand in terms of cost-performance and technical specifications, supply chain bottlenecks will ensue, leading to project delays and suppressed growth.

Facing the rigid assessment of the 2030 target (500 GW of renewable energy), the Indian government must navigate the delicate balance between protecting domestic manufacturing and achieving installation targets. SMM assesses that to prevent supply shortages from dragging down overall progress, the government is highly likely to introduce pragmatic amendments to ALMM List 2, effectively moderating the mandatory requirements for domestic cells. Concurrently, the shift of procurement focus toward Southeast Asia is expected to accelerate to bridge the supply-demand gap during this transition and mitigate geopolitical tariff risks.

On the pricing front, as leading Indian enterprises accelerate their upstream expansion into wafers and other components, improved vertical integration will drive cost reductions. Consequently, the price differential between domestic DCR modules and non-DCR modules is expected to narrow gradually.

Looking ahead, while the growth potential of the Indian PV market is undeniable, the continuity and flexibility of the policy environment, specifically the ability to timely remove supply-side obstacles will be decisive. Furthermore, improvements in supporting infrastructure, particularly grid access capabilities and the contract compliance rates of PPAs, are indispensable cornerstones for realizing India's ambitious 500 GW vision.

Written by: Ryan Tey

![[SMM PV News] US Solar Faces Labor Shortage Ahead of 'OBBBA' Deadline](https://imgqn.smm.cn/usercenter/xBtJB20251217171738.jpg)

![[SMM PV News] France Unveils 2026 Solar Auction Calendar and New Supply Rules](https://imgqn.smm.cn/usercenter/CpbPE20251217171736.jpg)

![[SMM PV News] Gulf Conflict Shifts Energy Markets, Impacting 'PPAs' and 'BESS'](https://imgqn.smm.cn/usercenter/xAoMy20251217171743.jpg)