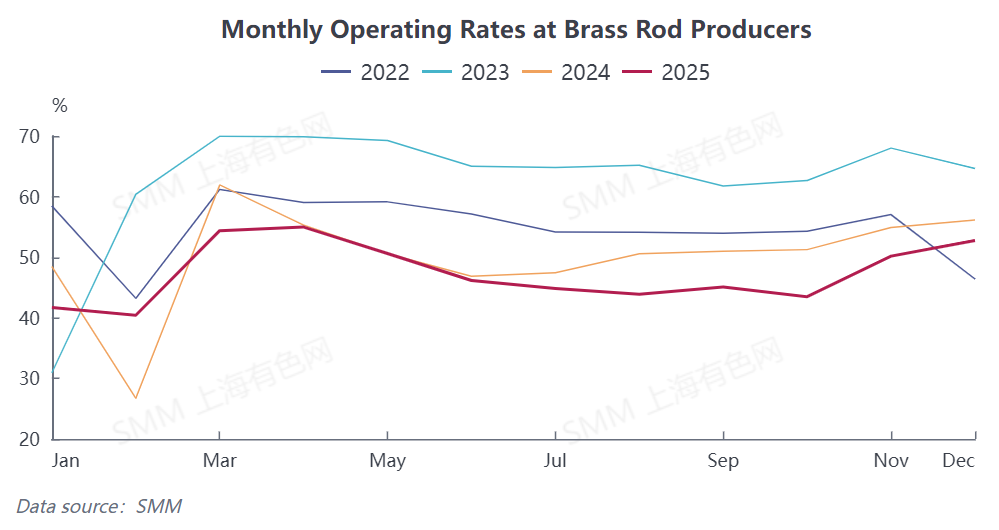

According to SMM data, the comprehensive operating rate for copper billet producers was 52.74% in December, up 2.56 percentage points MoM but down 3.4 percentage points YoY. Among them, the operating rate for large enterprises was 58.6%, medium-sized enterprises 44.22%, and small enterprises 36.88%.

Approaching the year-end closing stage, most brass billet producers focused on hitting annual output value targets, driving a temporary rise in the industry's operating rate through increased production scheduling—this was the core driver behind the MoM increase in the December operating rate. However, copper prices continued to fluctuate at highs during the month, pushing up brass billet production costs and significantly compressing gross profit per metric ton. Downstream procurement costs surged, prompting many buyers to voluntarily reduce order sizes and slow down their procurement pace to avoid cost fluctuation risks. In terms of industry inventory performance, cost pressure and cautious demand have translated into inventory changes: finished product inventories at SMM's sampled brass billet producers increased by 0.49 day MoM to 6.36 days, reaching a medium-high level within the year, indicating mounting pressure from inventory buildup. Meanwhile, raw material inventories fell by 0.12 day MoM to 4.01 days, reflecting producers' cautious stance on future copper price trends.

From the perspective of profitability and cost pass-through, the brass billet industry currently faces a dual challenge of "cost-side squeeze and demand-side pressure." Against the backdrop of continuously rising copper prices, the extent of price increases in downstream applications such as hardware accessories, electronic connectors, and sanitary fittings has lagged far behind the rise in copper prices, severely hindering cost pass-through. On one hand, fierce competition in end-use product markets weakens companies' willingness and ability to raise prices; on the other hand, some downstream customers have prices locked in through long-term agreements, further restricting cost pass-through space. This directly leads to profit margins being squeezed at both ends—for both end-processing enterprises and brass billet producers—resulting in a decline in overall industry profitability, with little chance of short-term improvement.

Additionally, amid high copper prices, substitution effects such as "aluminum as a substitute for copper" and "stainless steel as a substitute for copper" have emerged. In low-end hardware accessories and general machinery parts, some downstream customers are switching to aluminum alloys or stainless steel instead of brass, further diverting brass billet orders and putting additional pressure on the operating rates of small and medium-sized brass billet producers.

Looking ahead to January 2026, SMM expects the copper billet operating rate to pull back to 51.31%, down 1.43 percentage points MoM but up 9.62 percentage points YoY, mainly because the same period last year coincided with the Chinese New Year break, resulting in a low base. Specifically, according to feedback from brass billet producers, order intake since the start of accepting January 2026 orders from late December has fallen short of expectations. Most downstream customers plan to begin Chinese New Year holidays around late January, with weak pre-holiday stockpiling willingness. Expected order declines will directly lead to lower operating rates for brass billet in January, with some small producers even planning to start holidays early in late January. Combined with the continued suppression of demand from high copper prices, the usage proportion of alternative materials downstream may further increase, likely shrinking brass billet order volumes and raising operating pressure in the industry.