SMM Jan 13 News:

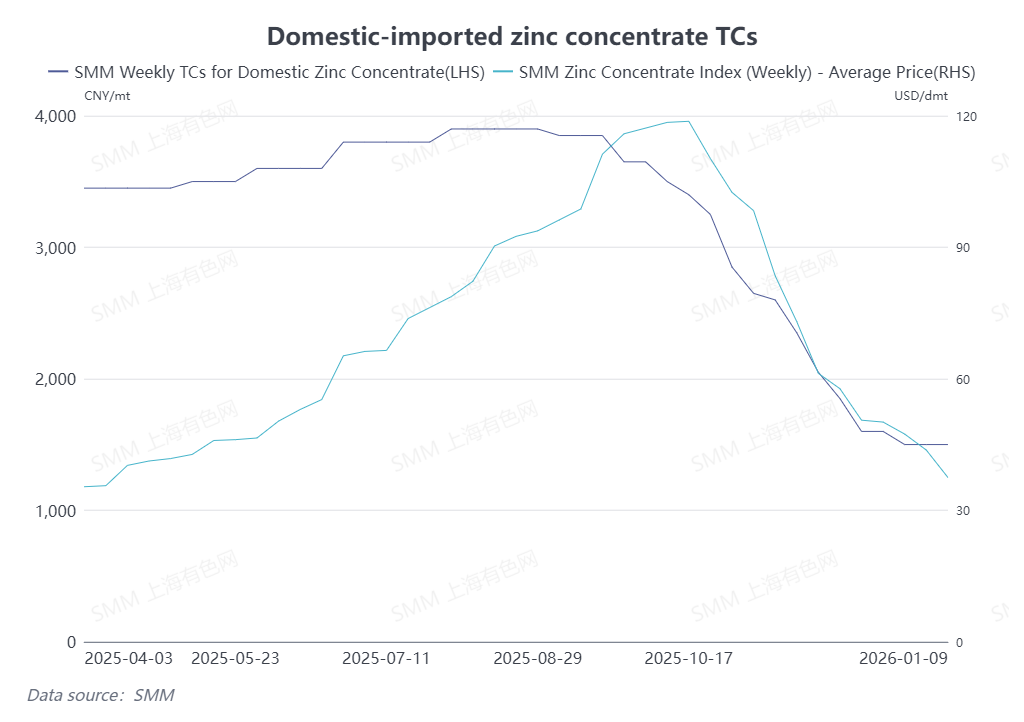

Entering 2026, as of January 6, the average TC for domestic zinc concentrate remained flat at 1,500 yuan/mt in metal content, while the TC for imported zinc concentrate continued to decline to $37.5/dmt. What are the reasons behind this "price spread" phenomenon, and what is the future trend?

The continued decline in TCs for imported zinc concentrate is mainly due to the sustained opening of China's import window for zinc concentrate as the price ratio between domestic and international markets rebounded above 7.5. Coupled with the lack of significant easing in the tight supply-demand situation for domestic zinc concentrate, some traders have shown a continued willingness to lower TCs for imports. Additionally, recent renewed flooding in Australia, although there is no clear indication yet of large-scale disruptions to local non-ferrous metal mine production, has caused road and regional logistics constraints, potentially posing disruptions to the arrival of some imported zinc concentrate shipments.

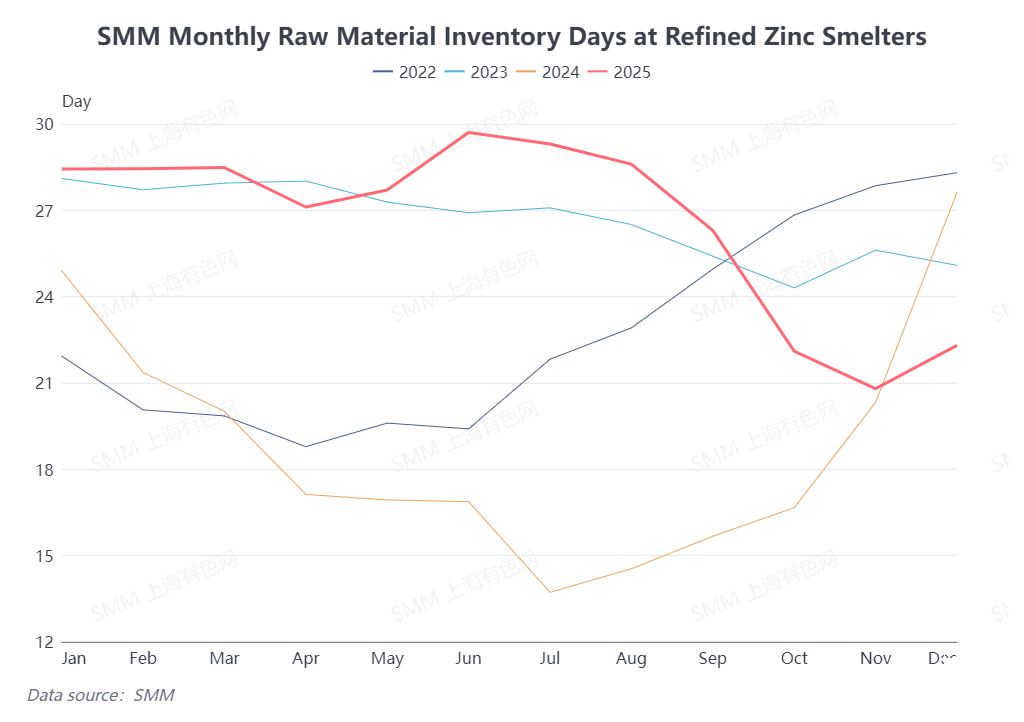

Meanwhile, TCs for domestic zinc concentrate have recently stabilized at low levels. On one hand, smelters conducted concentrated procurement of imported zinc concentrate in November and December for winter stockpiling needs. As these imported zinc concentrate arrived gradually, the days of raw material inventories at smelters have increased slightly MoM. On the other hand, considering the narrowing price spread between domestic and imported zinc concentrate and the persistently low production levels at smelters, the rush to purchase domestic zinc concentrate has somewhat subsided. However, the tight supply-demand pattern for domestic zinc concentrate has not shown significant improvement. In terms of actual trends, TCs for domestic zinc concentrate have only temporarily stopped falling recently, without a substantial rebound.

Overall, TCs for domestic zinc concentrate have remained low recently, while TCs for imported zinc concentrate have fallen below $40/dmt. Looking ahead, although smelter production is expected to increase in January due to favorable by-product prices, some smelters will undergo routine maintenance during the Chinese New Year in February. Monthly production of refined zinc in Q1 is projected to remain relatively low. Considering the overall supply-demand pattern, there is some possibility of a rebound in TCs for domestic zinc concentrate in Q1. SMM will continue to closely monitor subsequent trends.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)