【SMM Scrap Aluminium Market Analysis】Southeast Asia's Secondary Aluminum Industry Trapped in "Margin Squeeze": Raw Material Surge Forces ADC12 Plant Cuts, Industry May Enter "Lunar New Year Mode" Early

Since the fourth quarter of 2025, the international aluminum market has experienced a significant unilateral upward trend. Driven by supply-side sentiment stemming from the official implementation of the EU's Carbon Border Adjustment Mechanism (CBAM), combined with the absence of a price correction during the traditional year-end off-season and global holiday disruptions, LME aluminum prices have demonstrated strong resilience and sustained momentum.

According to SMM monitoring data, the LME aluminum cash settlement price soared from 2,683.5 USD/tonne on October 1, 2025, to 3,180 USD/tonne on January 9, 2026. In just one quarter, the price rose by 496.5 USD/tonne, a cumulative increase of 18.5%. The market generally predicts that this strong trend is unlikely to reverse in the short term and will likely persist until after the 2026 Lunar New Year (late February to mid-March 2026).

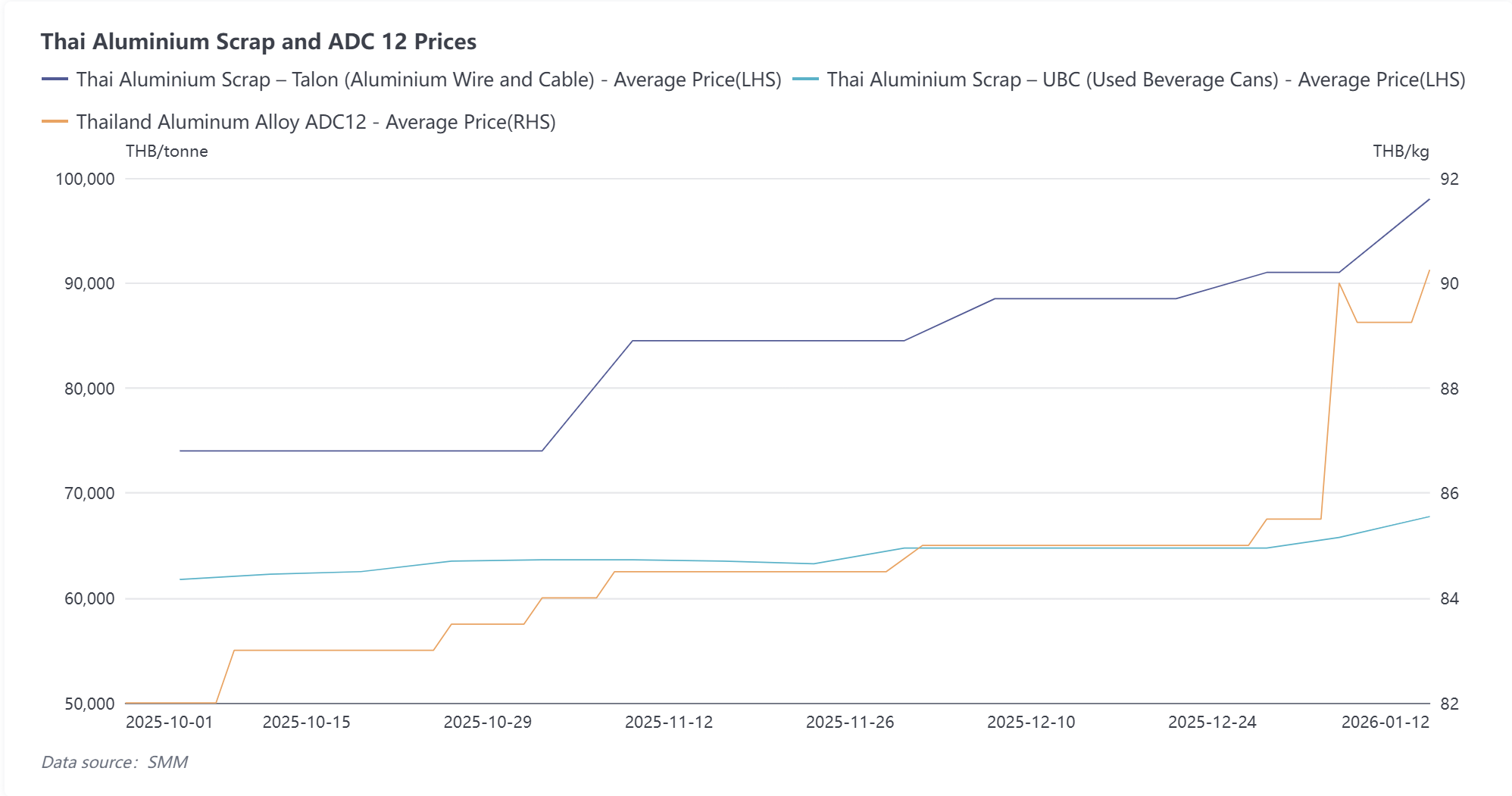

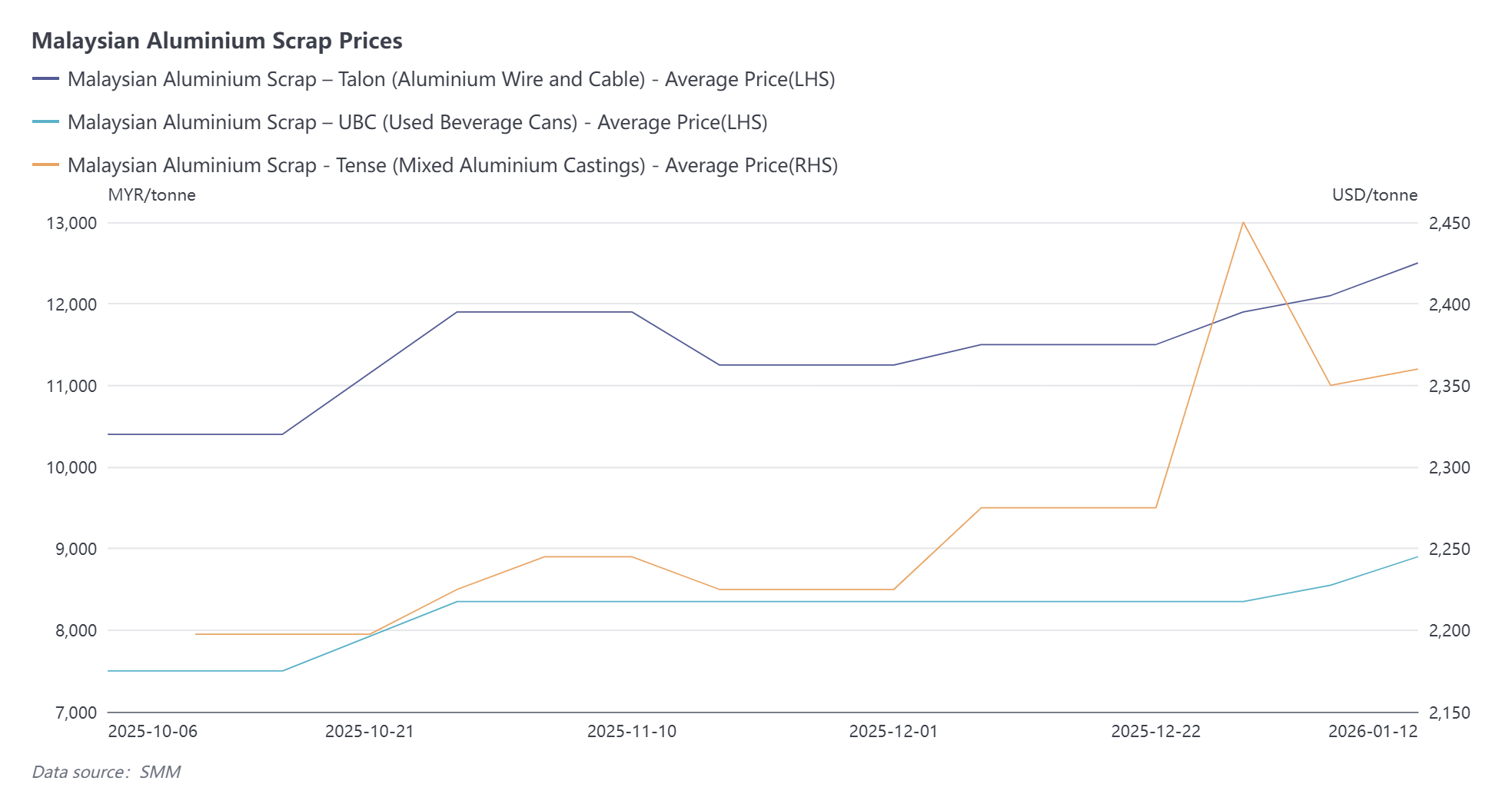

Scrap Prices Surge, Regional Raw Material Costs Hit Highs

Driven by the strong London aluminum price, the Southeast Asian aluminum scrap market responded quickly, showing a fierce "catch-up" trend. SMM market research covering the period from October 1, 2025, to January 2026 highlights significant price increases for major scrap varieties in Malaysia and Thailand:

In the Malaysian market, Tense (Mixed Aluminum Castings) prices shifted up to 2,207.5 – 2,360 USD/tonne (+6.9%). More strikingly, Talon (Clean Aluminum Wire), a high-quality raw material, surged to 10,400 – 12,500 MYR/tonne, a massive increase of 20.2%. UBC (Used Beverage Cans) also recorded an 18.7% growth, reaching 7,500 – 8,900 MYR/tonne.

The uptrend in the Thai market was even more aggressive. Talon wire prices skyrocketed from 74,000 THB/tonne to 98,000 THB/tonne, a staggering 32.4% increase. UBC rose by 11.1%, with quotes reaching 67,750 THB/tonne.

Finished Product Gains Lag Behind Materials; ADC12 Enterprises Face Severe Profit Squeeze

However, the price transmission mechanism along the industry chain has faced significant blockages. SMM research found that while raw materials surged (with wire varieties up over 20%-30%), the price increase for finished ADC12 secondary aluminum alloy ingots was comparatively meager. Malaysian ADC12 prices rose only 7.1% (to 2,850 USD/mt), and Thai ADC12 rose only 8.4% (to 90,000 THB/tonne).

This massive mismatch between raw material and finished product price increases has plunged Southeast Asian secondary aluminum plants into a severe "scissors gap" dilemma. On one hand, ADC12 smelters heavily dependent on scrap face historically high costs; on the other, downstream die-casting and automotive parts enterprises show low acceptance of high-priced alloy ingots. Procurement willingness has dropped to a freezing point ahead of the Spring Festival, making it impossible to effectively pass on the high costs.

Production Cuts and Early Holidays Become Consensus

With profit margins compressed to the limit or even suffering from cost inversion, risk avoidance has become the primary strategy. SMM's latest survey reveals that multiple ADC12 producers in Malaysia and Thailand have adjusted their operating plans. Facing shrinking profits and sharply contracting downstream orders, most companies have decided against maintaining full output, planning to implement production cuts in January 2026 or directly start the Lunar New Year holiday early.

Currently, the Southeast Asian secondary aluminum industry has effectively entered a "dormant period" ahead of schedule. Most manufacturers indicate that decisions regarding resumption or expansion of production will be postponed until after the Lunar New Year, pending the trend of LME aluminum prices and the recovery of downstream demand.

![[SMM Analysis]China's Aluminum Extrusion Exports Hit New Monthly Record in June 2026, Up 29.7% YoY](https://imgqn.smm.cn/usercenter/tkWbz20251217171654.jpg)

![Large Players Bid Up Prices to Make a Market, with Notable Boosting Effect [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/zlIyw20251217171654.jpg)