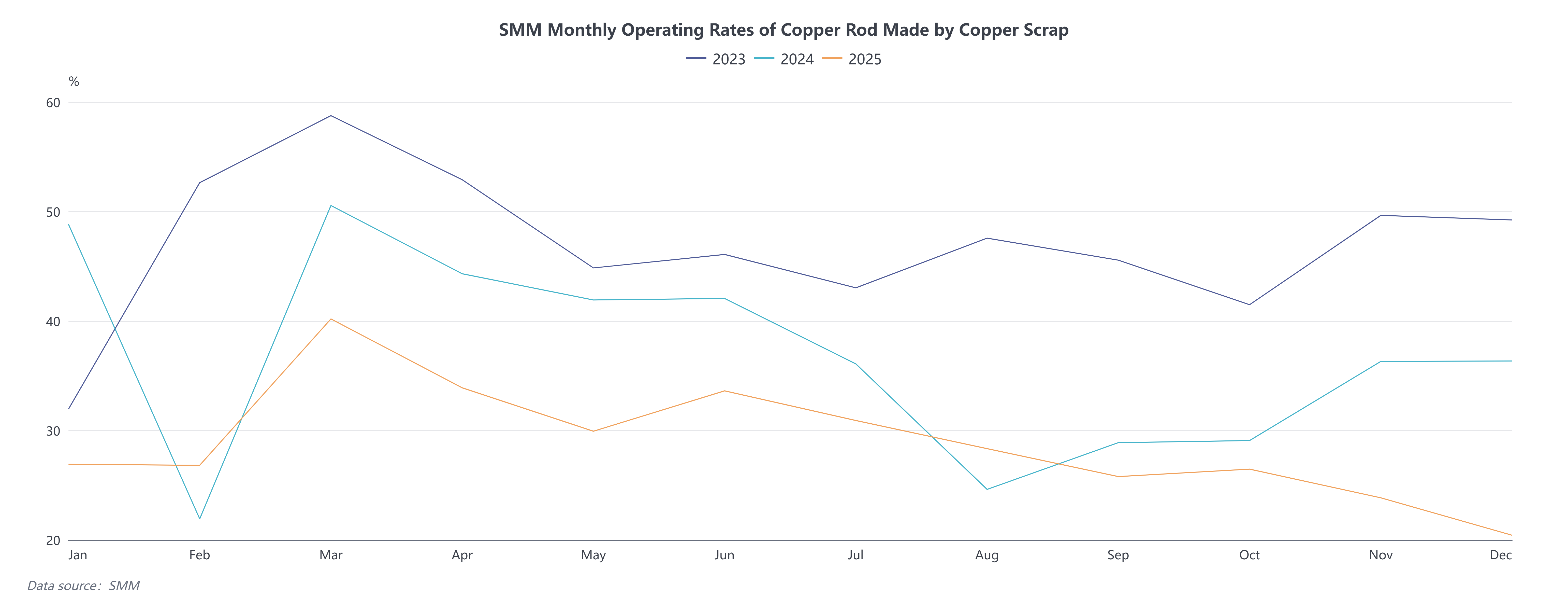

The operating rate for secondary copper rod was 20.42% in December 2025, higher than the expected 19.61%, but down 3.42 percentage points MoM and 15.92 percentage points YoY. The secondary copper rod market fell into a triple dilemma of "high prices, high policy barriers, and low end-use demand" at year-end, operating at a historically low range. Although the most-traded SHFE copper contract once surged above 100,000 yuan/mt, theoretically creating significant substitution potential from the price difference between primary metal and scrap, the market actually showed a deadlock of "deep divergence between price and volume." Even when the price difference between copper cathode rod and secondary copper rod widened to 2,342 yuan/mt, and the gross profit model indicated a weekly profit of up to 1,705 yuan/mt, enterprises' actual production and sales willingness remained weak. The core market conflict has shifted from traditional price competition to a structural deadlock dominated by policy uncertainty and funding difficulties.

Policy level has become the most critical variable suppressing market vitality. Under the risks of tax audits, the "reverse invoicing" policy has deviated from its original intention of solving the "first invoice" problem in practice. Enterprises, fearing investigations into the authenticity of transactions with individuals, have become hesitant in procurement and are forced to turn to high-priced tax-inclusive raw materials, directly driving up production costs. At the same time, the "Notice No. 770" regarding the cleanup of local "tax havens" has created significant uncertainty about the continuity of incentive policies. Many enterprises in major production areas such as Jiangxi and Anhui have chosen to suspend production and adopt a wait-and-see approach, awaiting clearer local implementation rules. This "vacuum period" effect of policies, combined with seasonal factors such as the general shortage of enterprise invoice quotas and tight capital chains at year-end, has led to direct production halts in areas like Hubei due to the inability to issue invoices, further drying up market liquidity. As a result, supply-side distortions have emerged: on one hand, unsold raw materials from suspended production in Jiangxi and Hubei have created localized oversupply; on the other hand, compliant tax-inclusive raw materials have maintained firm prices due to structural shortages.

Policy level has become the most critical variable suppressing market vitality. Under the risks of tax audits, the "reverse invoicing" policy has deviated from its original intention of solving the "first invoice" problem in practice. Enterprises, fearing investigations into the authenticity of transactions with individuals, have become hesitant in procurement and are forced to turn to high-priced tax-inclusive raw materials, directly driving up production costs. At the same time, the "Notice No. 770" regarding the cleanup of local "tax havens" has created significant uncertainty about the continuity of incentive policies. Many enterprises in major production areas such as Jiangxi and Anhui have chosen to suspend production and adopt a wait-and-see approach, awaiting clearer local implementation rules. This "vacuum period" effect of policies, combined with seasonal factors such as the general shortage of enterprise invoice quotas and tight capital chains at year-end, has led to direct production halts in areas like Hubei due to the inability to issue invoices, further drying up market liquidity. As a result, supply-side distortions have emerged: on one hand, unsold raw materials from suspended production in Jiangxi and Hubei have created localized oversupply; on the other hand, compliant tax-inclusive raw materials have maintained firm prices due to structural shortages.

On the demand side, high absolute copper prices have almost "eliminated" purchase willingness in the end-use market. Downstream enterprises such as wire and cable manufacturers, constrained by the sluggish real estate sector and their own financial pressures, have widely adopted a "delayed procurement" strategy, only placing orders based on pricing when delivery dates approach. This has led to fragmented and rush orders for secondary copper rod, failing to support a sustained rebound in operating rates. More notably, the market is facing severe issues of "price inversion" and "hidden inventory." To facilitate transactions, secondary copper rod enterprises often need to offer additional discounts beyond the usual futures discounts of 1,000–1,100 yuan/mt. Even so, transactions remain sluggish. A significant volume of already produced secondary copper rod, unable to be sold smoothly, has been converted into financing collateral stored in warehouses, forming a substantial "hidden" social inventory that poses potential pressure on future prices.

Looking ahead, the year-end stalemate is expected to persist into early 2026. The key to market recovery lies not in copper prices themselves, but in whether the fiscal and tax policies that have plagued the industry for months will be clearly implemented. If local subsidies and incentives are explicitly canceled, under the dual pressures of high copper prices and high tax costs, more small and medium-sized secondary copper rod enterprises are expected to opt for long-term shutdowns or complete transformation, further concentrating industry capacity toward leading compliant enterprises. In the short term, as the Chinese New Year approaches and end-users expand their holiday shutdowns, just-in-time procurement volume for secondary copper rod will continue to shrink, and the operating rate is projected to hover within the historically low range of 20%. The market predicament in December marks the end of an era of extensive development in the secondary copper rod industry. The future survival strategy for enterprises will shift entirely from relying on policy dividends and price speculation to competing on cost control, tax compliance capabilities, and supply chain resilience.