First, a review of the secondary aluminum alloy price trend in December: In the futures market, during early December, the most-traded cast aluminum alloy contract maintained a fluctuating consolidation pattern; in mid-December, it broke strongly above the moving average resistance and entered an accelerated upward channel. After the New Year's Day holiday, the market continued its unilateral upward trend, with prices frequently hitting record highs, and peaked at 23,490 yuan/mt on January 7.

On the spot market side, the SMM ADC12 price generally followed the upward movement of A00 aluminum prices in December, but maintained a discount for most of the period, only briefly switching to a premium at month-end. Entering January, as aluminum prices surged significantly, ADC12 returned to a discount status. As of January 9, the SMM ADC12 quotation was 23,700 yuan/mt, a cumulative increase of 2,200 yuan/mt from early December; the average price in December rose 1.5% MoM.

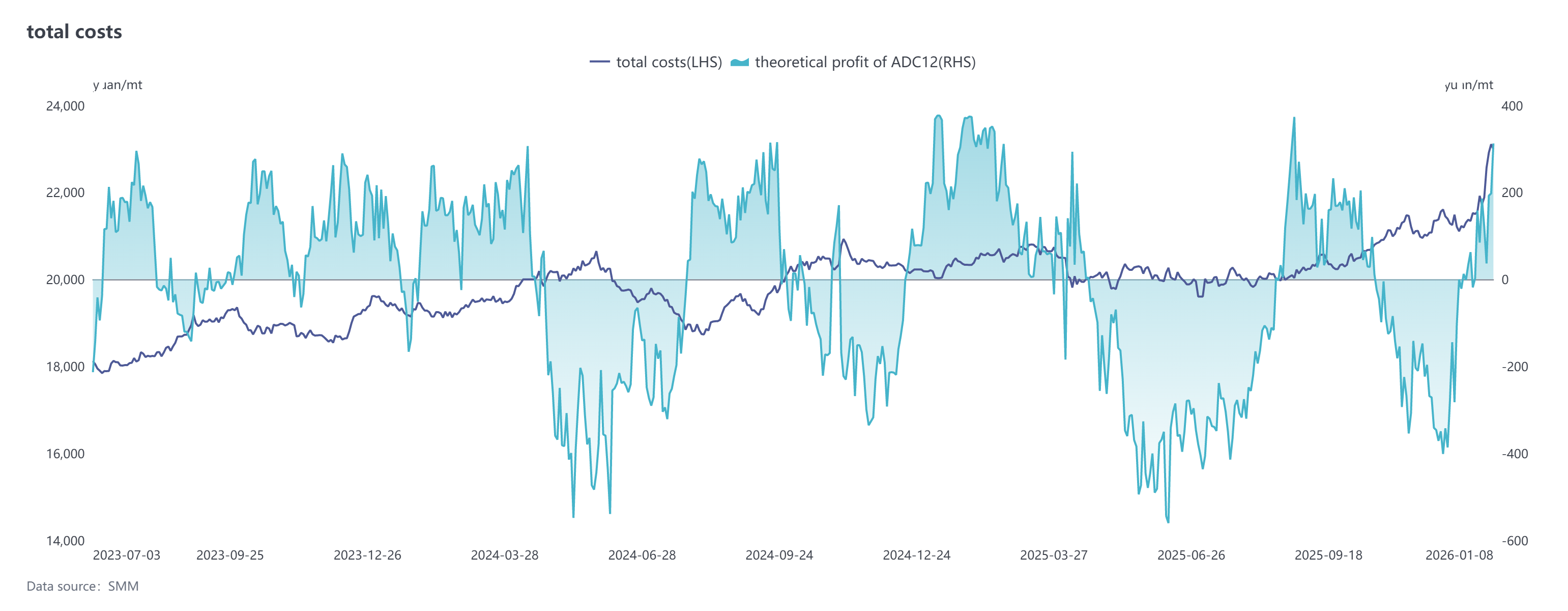

Cost side, according to the latest SMM data, the theoretical total cost of the ADC12 industry reached 21,428 yuan/mt in December, up 1.4 percentage points MoM from November. The full-year 2025 theoretical total industry cost was 20,444 yuan/mt, an increase of 3.4 percentage points YoY from 2024. In December, the aluminum scrap market showed a pattern of being more likely to rise than fall, and coupled with the sentiment boost from copper prices breaking through resistance and rising, prices of raw materials in the aluminum tense scrap category remained high. The cost of aluminum scrap per mt for ADC12 rose to 19,256 yuan in December, accounting for nearly 90% of the comprehensive cost. Cost pressure further transmitted in January: boosted by the dual surge in aluminum and copper, the per mt costs for aluminum scrap and copper rose to 20,647 yuan and 849 yuan, respectively, accounting for 90.2% and 3.7% of the total cost. Only silicon costs showed a downward trend, with the per mt cost dropping to 488 yuan, and its share pulling back to 2.1%. The cost side still provides support for ADC12 prices, but as the price increase of finished alloy ingots outpaced that of raw materials, industry profit margins improved somewhat, leading to a corresponding loosening of the cost support intensity.

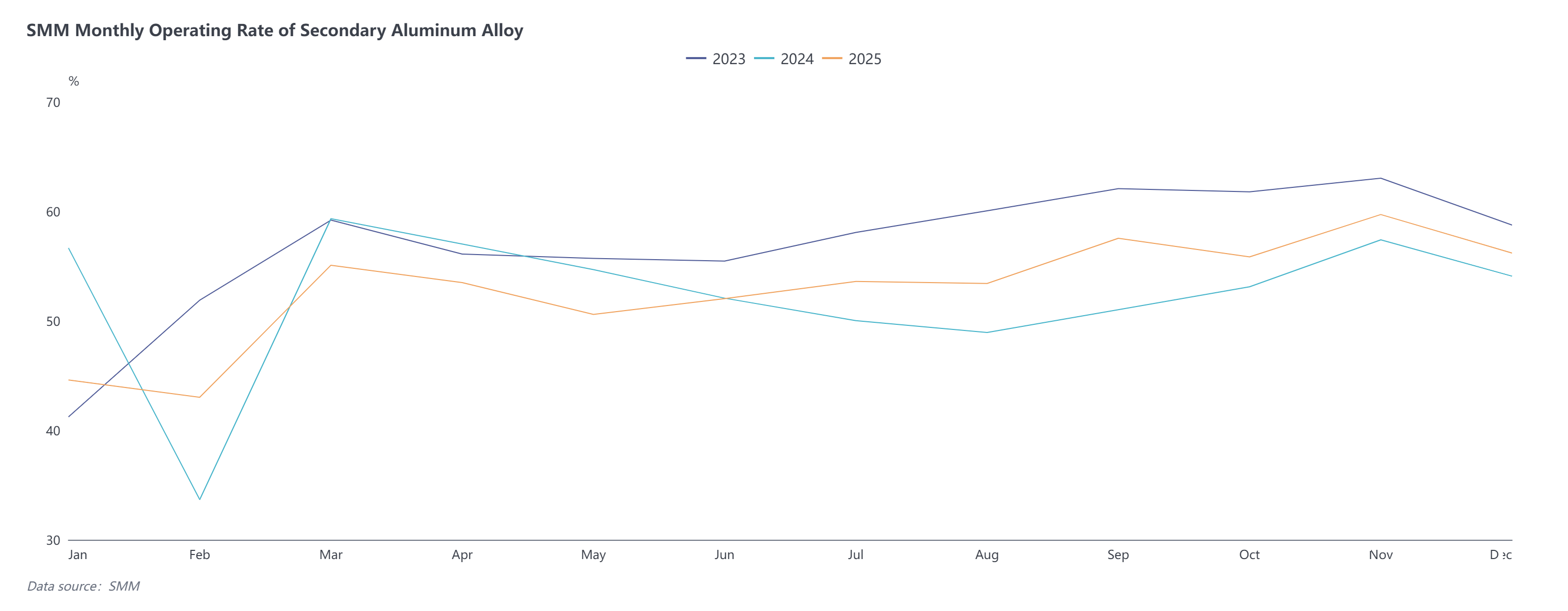

Supply side, the operating rate of the secondary aluminum alloy industry in December was 56.2%, down 3.5 percentage points MoM but up 2.1 percentage points YoY. The weakening operating rate during the month was mainly constrained by the following factors: first, demand weakened after mid-month, and aluminum prices hitting new highs intensified downstream fear of high prices, suppressing procurement and putting production under pressure; second, tight raw material supply and high costs eroded profits, with aluminum scrap supply continuing to tighten toward the end of the year, and rising aluminum and copper prices driving rapid increases in aluminum scrap prices, leaving enterprises facing procurement difficulties and cost pressure; third, environmental protection-related controls in multiple regions led to production restrictions or halts at some enterprises, compounded by unclear details of fiscal subsidies in some provinces, causing continued shutdowns at some producers and dragging down the recovery in operating rates. Since January, market demand has continued to weaken, and rapid increases in aluminum prices have hindered cost pass-through, forcing downstream players to increase production cuts and shutdowns due to operational pressure. As the Chinese New Year approaches, market expectations for stockpiling have cooled significantly. If aluminum prices continue to fluctuate at highs, the production and sales pace in the secondary aluminum industry may slow down further. The industry's operating rate in January is expected to show a clear pullback.

Entering January, prices showed an accelerated upward trend, with the ADC12 price surging 1,250 yuan/mt to 23,700 yuan/mt in a single week. However, industry chain contradictions became evident: on one hand, prices were driven up by the release of macro tailwinds and tight aluminum scrap supply; on the other hand, fear of high prices intensified among downstream buyers, who generally delayed purchases, and some even planned to halt production early, leading to a "price without market" situation. It is expected that the ADC12 price will fluctuate at highs in January, ranging from 23,000 to 24,200 yuan/mt. Cost support and tight supply will continue to provide a floor, but reduced pre-holiday stockpiling willingness and production reduction risk among enterprises will limit the upside room. In the short term, high prices and seasonal factors will jointly suppress the pace of production and sales, potentially further reducing market activity.

Entering January, prices showed an accelerated upward trend, with the ADC12 price surging 1,250 yuan/mt to 23,700 yuan/mt in a single week. However, industry chain contradictions became evident: on one hand, prices were driven up by the release of macro tailwinds and tight aluminum scrap supply; on the other hand, fear of high prices intensified among downstream buyers, who generally delayed purchases, and some even planned to halt production early, leading to a "price without market" situation. It is expected that the ADC12 price will fluctuate at highs in January, ranging from 23,000 to 24,200 yuan/mt. Cost support and tight supply will continue to provide a floor, but reduced pre-holiday stockpiling willingness and production reduction risk among enterprises will limit the upside room. In the short term, high prices and seasonal factors will jointly suppress the pace of production and sales, potentially further reducing market activity.

![Worsening Supply Concerns and Gradual Demand Recovery Stabilized the Geopolitical Premium and the Center of Aluminum Prices [SMM Aluminum Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/tkWbz20251217171654.jpg)

![Slightly Pessimistic Demand Expectations Weigh on ADC12 Prices’ Upside [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/ifCaw20251217171652.jpg)

![High-Level Consolidation in Secondary Aluminum[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)