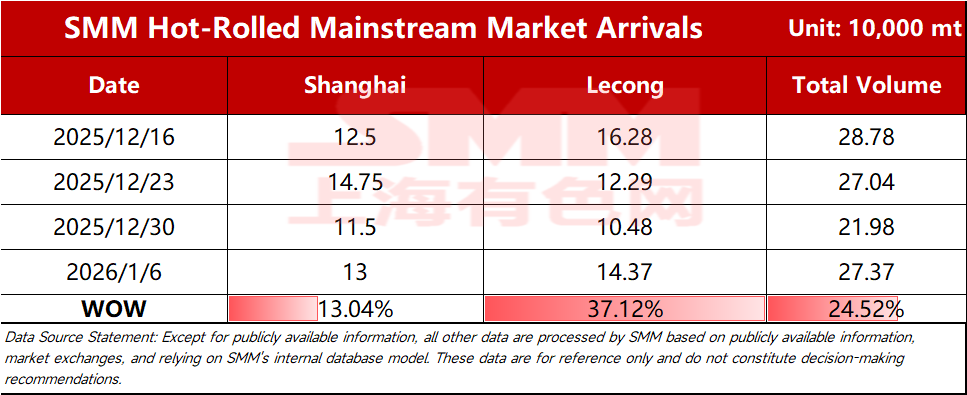

SMM Steel, Jan 6 – According to SMM statistics, estimated total resource shipments in mainstream markets this week reached 273,700 mt, up 24.52% WoW. By market:

Table 1: Comparison of Mainstream Market Arrivals

Data source: SMM Steel

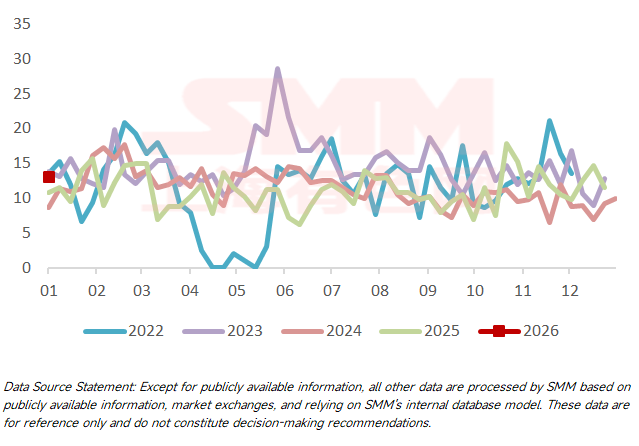

Shanghai market: Shipments in the Shanghai market rose slightly WoW. Specifically, the increase mainly came from the Northeast market, while shipments from North and South China remained basically stable. Looking ahead, recent hot-rolled coil prices fluctuated rangebound, and end-use demand saw periodic increases. Merchants' ordering enthusiasm was relatively moderate. However, due to recent adjustments in shipment pace by some steel mills in South China, arrivals in the Shanghai market may fluctuate rangebound in the short term.

Chart 1: Shanghai Market Arrivals

Data source: SMM Steel

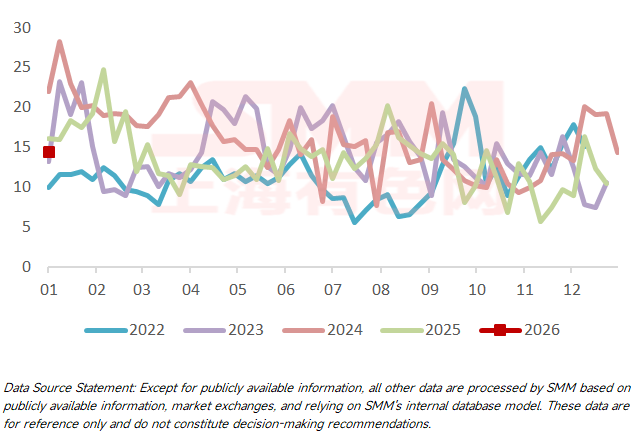

Lecong market: Shipments to the Lecong market rebounded WoW. Specifically, current prices in South China remain relatively low, making it difficult for resources from North China to flow south. The difference in arrivals is mainly influenced by local mainstream resources. WG's export orders were limited, leading to a relative increase in domestic sales resources. Looking ahead, mainstream steel mills plan to shift hot metal production, so the likelihood of a continued increase in arrivals in the South China market is expected to decrease in the short term.

Chart 2: Lecong Market Arrivals

Data source: SMM Steel

SMM releases hot-rolled shipment data for mainstream market flows every Tuesday. To subscribe or follow more data, please scan the QR code below.

![[SMM Steel] Indonesian Billet Edges Down as Chinese Offers Weigh](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)

![[SMM Steel] Alang Scrap Stable, Mandi Market Rises](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)