SMM January 5 News:

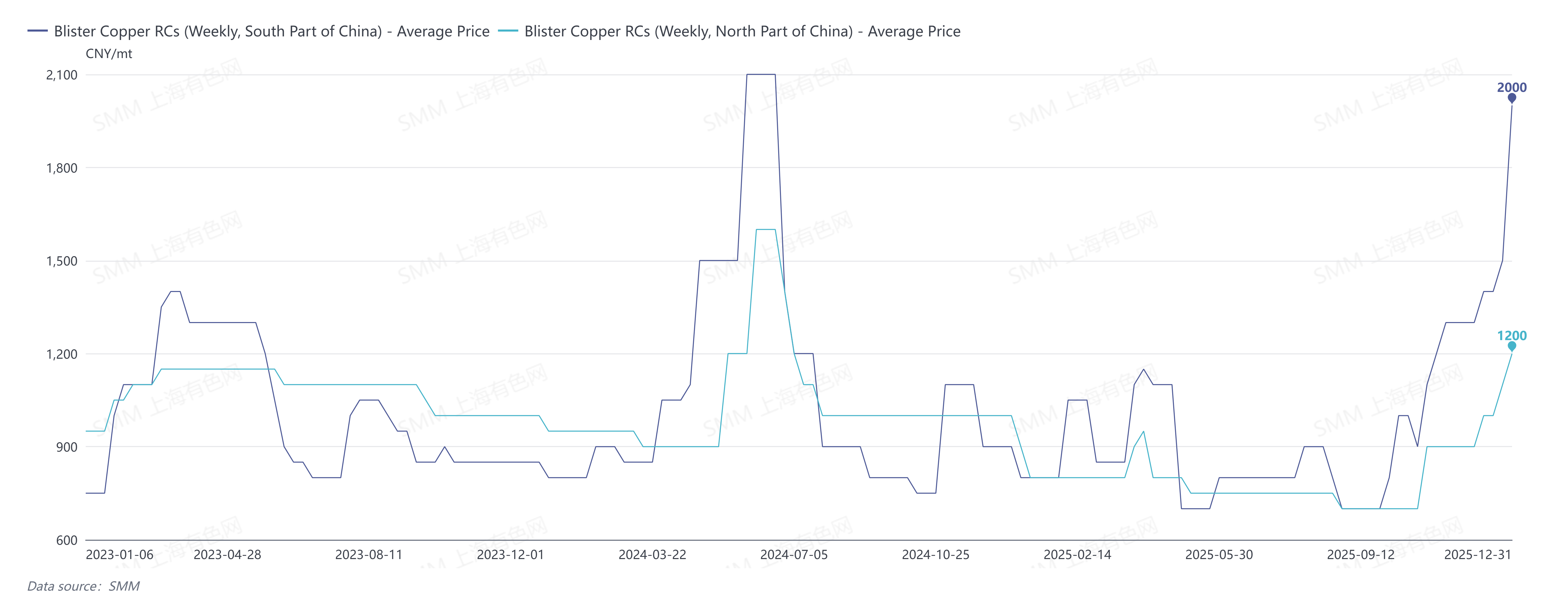

SMM's December 2025 blister copper RCs in south China were quoted at 1,400-1,600 yuan/mt, with an average of 1,500 yuan/mt, up 250 yuan/mt MoM; blister copper RCs in north China were quoted at 900-1,200 yuan/mt, averaging 1,050 yuan/mt, up 150 yuan/mt MoM; blister copper RCs, CIF China were quoted at $90-100/mt, averaging $95/mt, flat MoM.

Since Q4, blister copper RCs have continued to rise, with supply-side expansion as the core driving factor. Copper prices surged significantly in December, boosting the price difference between primary metal and scrap to widen notably; meanwhile, Copper scrap rod faced severe discounts, with the price spread between Jiangxi's 8mm Copper scrap rod and Chinese Copper Anode RC spot exceeding 1,000 yuan/mt. This boosted the supply of raw materials such as secondary copper, scrap-derived blister copper, and copper anodes. On the demand side, smelters scaled back procurement volumes during the year-end period due to inventory control and capital flow needs, leading to a looser secondary raw materials market and supporting higher RCs.

SMM's latest weekly blister copper RCs in south China were quoted at 1,900-2,100 yuan/mt, averaging 2,000 yuan/mt; weekly blister copper RCs in north China were quoted at 1,000-1,400 yuan/mt, averaging 1,200 yuan/mt; Chinese Copper Anode RC spot were quoted at 1,100-1,300 yuan/mt, averaging 1,200 yuan/mt.

SMM expects the blister copper market to maintain a loose pattern in January 2026, with RCs fluctuating at highs. Demand side, after the year-end period and before the Chinese New Year holiday, smelter restocking demand will gradually release, and market demand expectations are set for a mild rebound. However, on the supply side, the wide price difference between primary metal and scrap will persist, secondary copper will continue flowing into smelting ports, and the supply of scrap-derived blister copper and copper anodes in the Chinese market will remain the core support for RCs.

In the import market, upstream and downstream players are in the window for signing 2026 long-term contracts. Chinese RCs hold a relative competitive advantage, and activity in the import spot market remains low. According to SMM, CNMC International Trading Co. Ltd. and Jiangxi Copper Corporation reached an agreement on the 2026 blister copper RC, CIF China benchmark at $85/mt on December 23, 2025 Beijing time, compared with $95/mt in 2025. This long-term contract outcome also indicates that despite expected new copper anode capacity overseas next year, tight copper ore supplies have raised market expectations for global copper anode demand in 2026.