SMM Ngày 5 tháng 1 Tin tức:

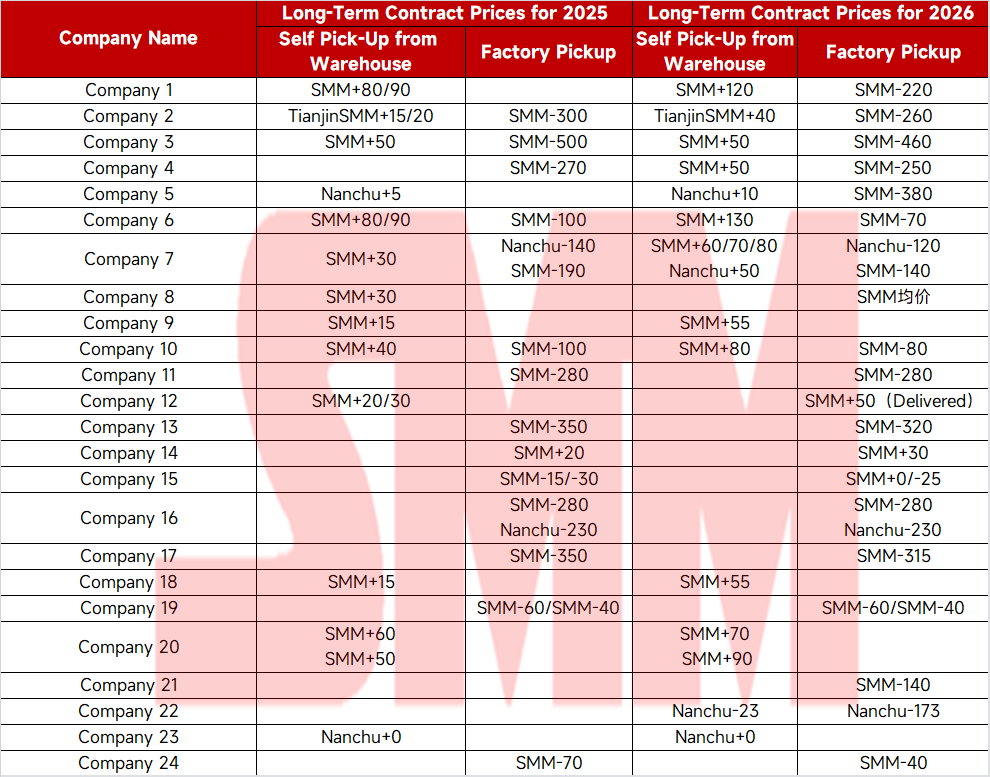

Đầu năm mới, các hợp đồng dài hạn cho năm 2026 hầu như đã được ký kết, và một chu kỳ thực hiện mới đã bắt đầu. Thị trường đang theo dõi sát sao việc thực hiện hợp đồng dài hạn của các nhà máy luyện kẽm trong năm nay. SMM đã tổng hợp và trao đổi thông tin về giá hợp đồng dài hạn của một số doanh nghiệp cho năm 2026 như sau:

Xét từ góc độ ký kết hợp đồng dài hạn, giá hợp đồng dài hạn năm 2026 nhìn chung tăng 10–40 nhân dân tệ/tấn so với năm trước. Điều này chủ yếu do hai yếu tố: thứ nhất, giá giao dịch tự thu gom kho cả năm 2025 trung bình ở mức cao hơn khoảng 50 nhân dân tệ/tấn so với giá SMM, mang lại lợi nhuận năm khả quan; thứ hai, vẫn còn một số cơ hội xuất khẩu kẽm thỏi vào năm 2026, với một số nhà máy luyện kim duy trì mức độ rủi ro nhất định, dẫn đến việc giá hợp đồng tăng tổng thể.

Về mô hình cung-cầu năm 2026, với việc công suất kẽm thỏi mới dần được đưa vào, sản lượng nhà máy luyện kim cả năm dự kiến tăng khoảng 300.000 tấn so với cùng kỳ năm ngoái, tăng hơn 4% so với cùng kỳ. Tuy nhiên, về phía tiêu thụ, khi "Kế hoạch 5 năm lần thứ 16" bắt đầu, nhu cầu tiêu thụ chính dự kiến sẽ xuất hiện ở các lĩnh vực mới nổi như AI, trong khi kẽm, vốn được thúc đẩy truyền thống bởi cơ sở hạ tầng và bất động sản, có khả năng chứng kiến mức tăng trưởng tiêu thụ tổng thể hạn chế. Tiêu thụ cả năm dự kiến tăng 1%–2% so với cùng kỳ, với phía cung trong nước chủ yếu ở trạng thái thặng dư. Mức tăng từ các nhà máy luyện kim nước ngoài có hạn, và tiêu thụ dự kiến sẽ hoạt động tốt hơn so với thị trường nội địa. Với việc LME vượt trội hơn SHFE, các cơ hội xuất khẩu kẽm thỏi không thường xuyên được dự báo, và khối lượng xuất khẩu thực tế cần được theo dõi chặt chẽ.