Recently, the Industrial Development Department of the National Development and Reform Commission (NDRC) released the article “Vigorously Promoting the Optimization and Upgrading of Traditional Industries.” It explicitly states that for resource-intensive sectors such as alumina and copper smelting, management must be strengthened, layouts optimized, and large backbone enterprises encouraged to carry out mergers and reorganizations. After this policy signal was issued, the subsequent trajectory of the alumina industry has attracted widespread attention. This article will analyze the likely development paths for alumina refineries from three dimensions: policy orientation, current industry status and future trends.

I. Policy orientation: layout optimization and M&A become the core

The NDRC’s latest document highlights the government’s resolve to regulate resource-intensive industries. Alumina, a sector typified by high energy consumption and heavy resource dependence, has long suffered from irrational geographical distribution and intense environmental pressure. The policy requires each region to build distinctive productivity layouts that reflect local industrial foundations, resource endowments and environmental carrying capacity. This means alumina-project approvals will be stricter, curbing blind investment and inefficient expansion. At the same time, large backbone enterprises are encouraged to merge or acquire, integrating resources to raise industry concentration and overall competitiveness. This policy thrust will accelerate sector reshuffling and channel superior resources toward the leading producers.

II. Current landscape: an alumina industry squeezed by costs, over-capacity and environmental compliance

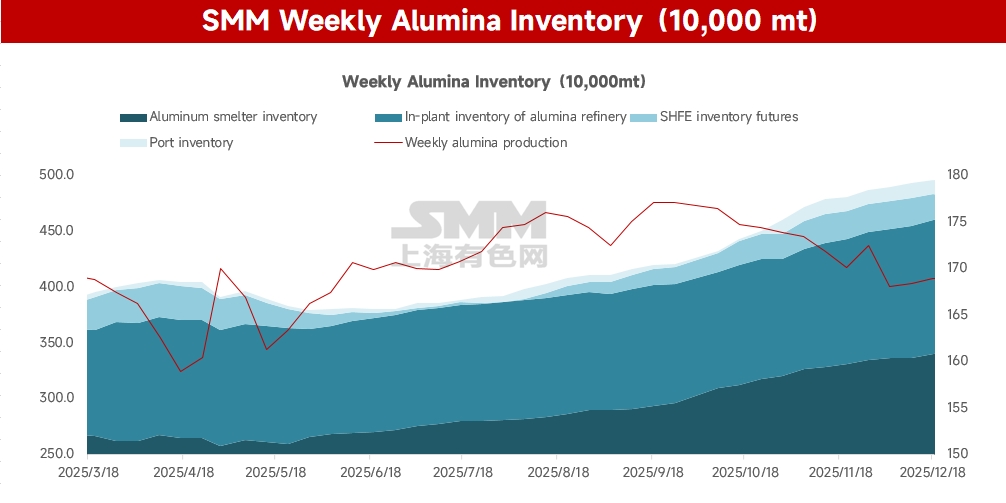

China’s alumina sector is under triple pressure. SMM data show that, as of last Thursday, the country’s installed metallurgical-grade alumina capacity stood at 110.32 million tpy, with operating capacity at 88.09 million tpy—an operating rate of 79.85%. Against this backdrop, inventory pressure is mounting: refineries currently hold about 1.2 million mt of product, while smelters sit on 3.42 million t of feed, both at their highest levels this year.

On the cost side, the industry remains highly import-dependent; its fragile bauxite supply chain leaves it exposed to swings in international resource prices, rising freight rates and geopolitical risk. Meanwhile, the “dual-carbon” target is pushing energy and environmental-compliance costs steadily higher, eroding profit margins. In terms of supply and demand, over-capacity is entrenched. Social inventories have climbed to record highs, keeping prices under constant pressure; cut-throat competition has left the sector mired in razor-thin or negative profitability. Environmental constraints are also tightening. Red-mud disposal and other ecological challenges impose heavy financial and environmental costs, while strict carbon-emission controls force producers to pour large sums into green, low-carbon retrofits. Transformation remains a long and arduous task.

III. Future trajectory: consolidation amid surplus, transformation under constraints

Guided by policy orientation and market fundamentals, China’s alumina sector is entering a profound structural adjustment. Its next decade will be defined by four hallmarks—excess capacity, a falling cost curve, and constraints from environmental protection—forcing the industry to seek a way out through integration, optimization and upgrading.

1. Accelerated scale-driven consolidation: integration becomes the dividing line

Spurred by both policy incentives and bare-knuckle survival pressure, large producers will use mergers & acquisitions to forge several cross-regional, full-chain giants. This is not merely a route to higher concentration; it is becoming a prerequisite for competing at all. The decisive watershed will be whether a company owns “alumina + smelter” integration. Integrated players, cushioned by stable internal supply and cost synergies, enjoy far stronger risk resilience, whereas stand-alone medium-sized refineries risk being squeezed out by volatile costs and prices.

2. Over-capacity to persist; domestic layout shifts to counter overseas supply

Surplus supply will persist over the next five years. Domestic installed capacity is still climbing and could reach ~126 million tpy by 2026-2027. Simultaneously, overseas—especially Indonesian—ramp-ups will add ~5 million tpy in the same period; because matching smelters there lag, most of this material will flow to China. To meet the pincer movement, capacity is migrating toward coastal clusters such as Guangxi, leveraging port logistics to lower combined input-output costs and build industrial agglomerations that can compete more efficiently with seaborne resources. Yet this relocation will further entrench structural surplus.

3. Cost logic dominates prices, outdated capacity to exit

Pricing will revolve around a shifting cost curve. Expectations of looser bauxite and caustic-soda supply will drag the entire curve downward, sharpening producer differentiation. Plants with coastal location, energy or technological advantages will keep a berth; inland, non-integrated refineries relying on imported ore will see cash costs chronically above market prices, sink into losses and eventually exit.

4. Growing environmental protection pressure threatens enterprise survival

Environmental protection rules—especially large-scale valorization of red mud—have moved from a cost issue to a hard constraint on whether capacity can run at all. Traditional ponding is no longer viable, and environmental stockpiles are rising. Firms that fail to achieve breakthroughs in emission-reduction and comprehensive red-mud utilization risk harsh output curbs or outright shutdowns. In Guangxi and other concentration zones, regional environmental capacity could trigger more frequent restrictive measures. Green technology and compliance capability now determine operational continuity.

Conclusion

Going forward, China’s alumina sector will be deeply reshuffled amid persistent surplus. The competitive battleground will shift from simple scale expansion to a combined contest of cost control, integrated synergies, green technology and locational advantage. The ultimate outcome will be higher concentration, better geographical layout and more sustainable development—completing the arduous transition from quantity-led growth to quality-based competition.

The NDRC’s policy stance has set the course for “optimization and upgrading.” Driven by both resource constraints and green-development imperatives, alumina refineries will inevitably move toward greater scale, intensification and sustainability. Companies must actively embrace the trend, strengthen technological innovation and refine resource allocation if they are to remain standing after the shake-out. Future alumina industry—more efficient, cleaner and more resilient—will provide solid underpinning for the high-quality development of China’s manufacturing economy.