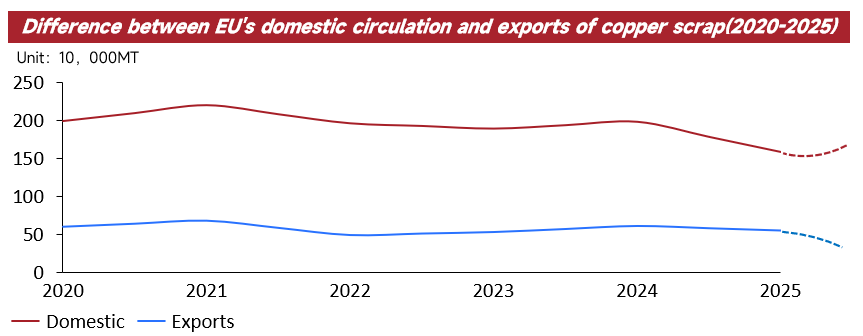

Internal Trade Shrinks Far More Severely Than Exports

Data from 2025 indicates a significant downturn in the circulation of copper scrap within the European Union, with the decline in internal trade far outstripping the drop in exports to external markets. This suggests that despite policy efforts to retain resources within the bloc, the market’s reality is a rapid erosion of internal consumption capacity. This structural divergence demonstrates that the outflow of copper scrap is driven not only by external demand but also by the stagnation of Europe’s own industrial needs.

Causes of Stagnated Internal Demand: Manufacturing Slump and High Costs

The "cliff-like" drop in EU internal copper scrap trade is primarily driven by a collapse in consumption. Led by Germany, Europe’s industrial powerhouses are seeing sustained weakness in copper-intensive sectors such as automotive, construction, and electrical equipment. As orders plummet, factories have slashed raw material procurement to a minimum.

Simultaneously, high energy prices have saddled European smelters with cost structures significantly higher than those of their Asian counterparts. To remain operational, these smelters are forced to lower their purchase prices for copper scrap. Consequently, scrap flows toward overseas markets that offer higher bids and faster capital turnover.

The "Front-Running" Effect of Policy Tightening

Market behavior is being further distorted by the anticipation of looming regulations. Starting in July 2025, the EU launched systematic customs monitoring of cross-border metal scrap movements. Stricter regulatory frameworks will take effect in May 2026, culminating in a total export ban to non-OECD countries by May 2027. This clear regulatory roadmap has triggered a "front-running" effect. To bypass future compliance costs, complex auditing processes, and the eventual ban, traders are accelerating liquidations during the current window of opportunity.

The European Recycling Industries’ Confederation (EuRIC) has voiced urgent concerns, stating that the European Commission must extend the deadlines related to the new Waste Shipment Regulation (WSR) to prevent a collapse of the regional scrap market. Under the WSR, non-OECD countries must submit applications to the EU by February 21, 2025, to continue importing materials classified as waste."If applications are not submitted by the deadline, the EU will implement a total export ban on recycled materials to nearly 150 countries starting May 21, 2027," EuRIC warned. The federation noted that while it is pushing for compliance, most non-OECD countries are ill-prepared for the EU’s "cumbersome application procedures," which involve massive datasets and complex questionnaires that place an immense burden on foreign administrations. Furthermore, EU outreach has been insufficient, leaving these nations largely unaware of the economic impact the WSR will have on global trade and the supply of recycled materials. EuRIC argues that if the export market collapses, the EU’s own recycling industry will shrink, leading to recyclable waste being landfilled and undermining public trust in waste sorting.

Attempting to retain resources solely through restrictive export policies addresses the symptoms rather than the root cause. Resource retention is only viable if there is sufficient domestic capacity to process and consume them. Without a recovery in European manufacturing competitiveness, copper scrap forcibly kept within the bloc via tariffs or bans will merely turn into unmarketable inventory rather than economic value. Furthermore, administrative intervention risks decoupling European internal prices from the global market, artificially suppressing local purchase prices. This will directly discourage investment in the recycling industry and undermine the circular economy.

Final takeaway

The outflow of copper scrap is a consequence of Europe’s deindustrialization, not its cause. Relying on administrative force to redirect resource flows will only amplify internal structural contradictions. The solution lies not in sealing borders, but in restoring the competitiveness of European manufacturing. Only when European industry is competitive again will copper scrap remain within the region through the natural logic of the market.