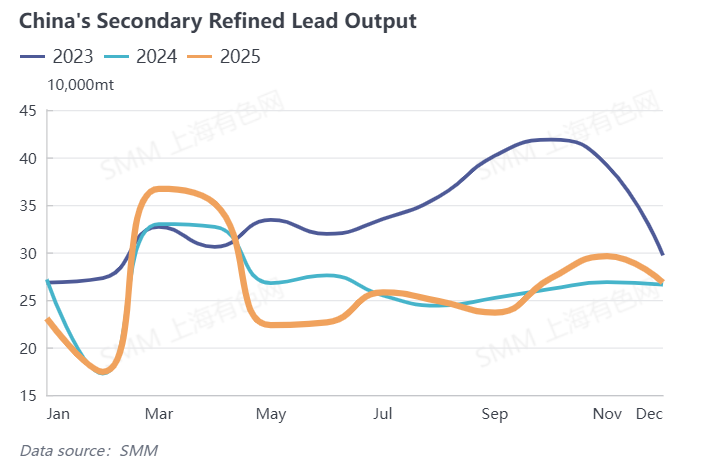

Secondary lead production fell in December 2025, down 5.03% MoM but up 10.3% YoY. Secondary refined lead production dropped 9.33% MoM and increased 0.84% YoY.

Main Reasons for Production Fluctuations

1. Impact of Environmental Protection-Related Controls

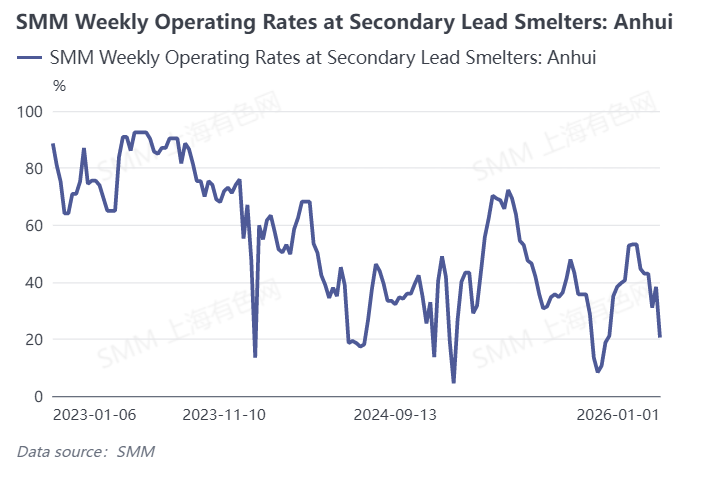

In December, many areas in east China and north China implemented environmental protection-related controls due to severe air pollution, with significant production cuts at smelters in Anhui, a major secondary lead production region.

2. Tight Raw Material Supply

Colder temperatures in north China reduced the volume of retired lead-acid batteries from e-bikes, and poor arrivals of waste lead-acid batteries constrained secondary lead output. Large smelters in regions such as Inner Mongolia and Guizhou cut production due to critically low raw material inventories.

3. Decline in Smelting Profits

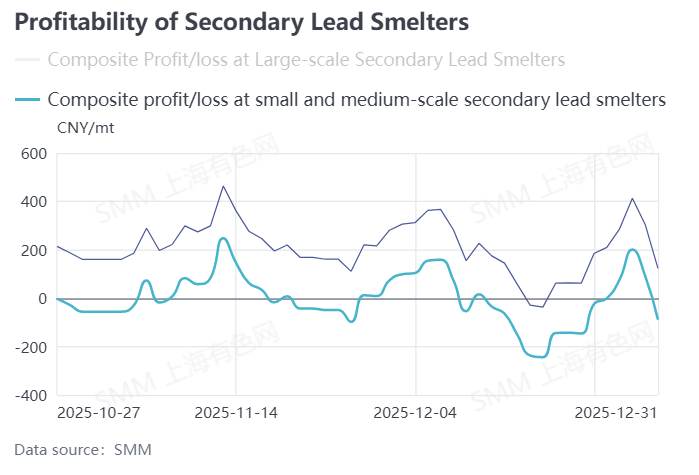

Mid-December saw a noticeable drop in profits for secondary lead smelters, and loss-making conditions dampened production enthusiasm.

4. Equipment Maintenance and Other Factors

Some smelters in central and south-west China saw output affected by technological transformation of equipment. Individual secondary lead smelters in east and central China halted production due to the renewal of hazardous waste operation permits.

SMM Expects Low Production Levels in January 2026

Unfavorable Factors

- Ongoing environmental protection-related controls: Frequent winter smog implies potential restrictions on secondary lead smelter output.

- Raw material supply pressure: Reduced retirement of waste lead-acid batteries makes it difficult to ease the tight supply situation.

- Proactive production cut plans by enterprises: For example, a medium-sized secondary lead smelter in south-west China plans to reduce output by 20%–30% in January in response to raw material pressures.

Favorable Factors

- Production resumptions: Enterprises affected by equipment maintenance in December are expected to resume normal production in January.

- Demand support: Downstream enterprises are expected to maintain normal restocking demand after the New Year holiday, providing some support for lead prices and potentially slowing the narrowing of secondary lead profit margins.

Overall Forecast

SMM data indicate that secondary lead production in January 2026 is expected to increase slightly. However, environmental controls, tight raw material supply, and limited profit margins remain potential constraints on production growth in the short term, and actual secondary lead output is likely to remain low in January.

![Geopolitical Tensions Escalate Lead Prices Give Up Previous Gains [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![Energy Supply Pressures and Lead Ingot Inventory Buildup Coexist Lead Prices May Continue to Consolidate [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)