Against the backdrop of the US continuing to strengthen its “supply security” and “critical minerals” policy framework, base metals with high import dependency have increasingly come under market scrutiny. Historically, similar logic has already materialised under Section 232 in steel, aluminium and selected key metals. Within this context, zinc has been persistently viewed by the market as a potential candidate for closer policy attention.

Policy timeline and procedural window

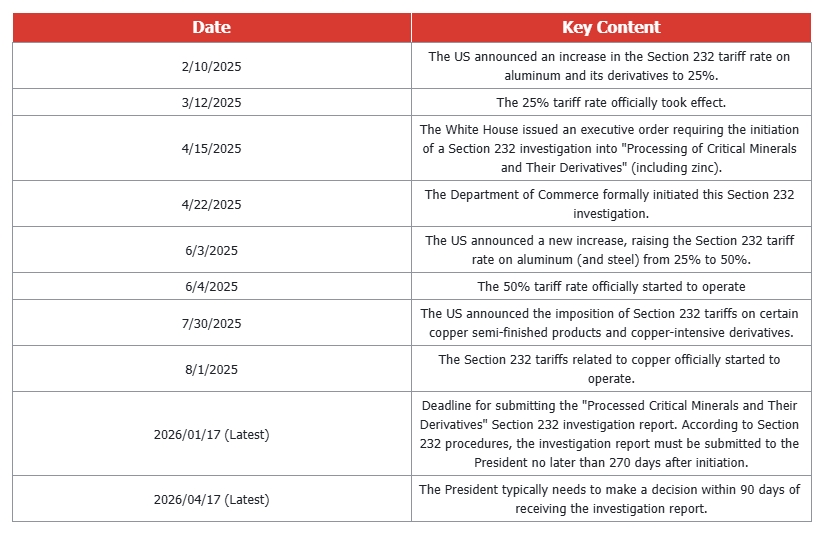

Since early 2025, the US has progressively escalated Section 232 measures on aluminium and related products, and formally expanded the scope of investigation to include processed critical minerals and their downstream products. According to statutory procedures, the investigation report must be submitted to the President within 270 days of initiation, followed by a 90-day decision window. This places the key policy inflection point for zinc-related outcomes broadly between Q1 and Q2 2026.

Until then, the zinc market remains in a phase where the investigation process is ongoing but policy outcomes remain undefined, sustaining a degree of structural uncertainty.

From a fundamental perspective, US zinc consumption is characterised by a relatively high reliance on imports compared with other base metals. This structural feature places zinc naturally within the scope of the “supply security” narrative. Should trade measures targeting zinc or zinc-containing products be implemented, the impact is unlikely to manifest as an immediate global supply shortage. Instead, the more probable transmission mechanism would be:

-

an increase in US regional delivered prices,

-

a widening of regional price differentials, and

-

a re-routing of global trade flows driven by relative pricing signals.

From a fundamentals and structural perspective, the gradual realisation of China’s export volumes, together with the release of previously hidden inventories through delivery, has led to a visible rebound in LME zinc stocks to around 100 kt. The forward curve has shifted into a stable contango, indicating a clear improvement in near-term deliverability and market liquidity. Structural tightness has therefore eased, with pricing dynamics increasingly reverting to inventories and spot supply-demand conditions.

Under this environment, zinc tariff expectations are now more appropriately reflected as a latent policy risk premium, rather than through structural distortions in the curve. Should policy signals become clearer, such premia may be further priced out. Conversely, if trade measures targeting zinc or related products are introduced, their impact is more likely to materialise through higher US regional prices and wider inter-regional differentials.

Cases Framework

-

Base case (50%–70%) The US refrains from introducing explicit, zinc-specific tariff measures in 2026, while investigations and policy uncertainty under the “critical minerals / supply security” framework persist. In this scenario, the zinc curve remains in contango, with inventory recovery and improved deliverability anchoring near-term pricing. Policy expectations are reflected mainly as a latent risk premium rather than structural distortions, with limited impact on price direction.

-

Bull case (policy escalation, 15%–30%) The US implements substantive trade measures targeting zinc or zinc-related products, with tariff levels sufficient to materially raise US delivered costs. As a result, global trade flows may temporarily tilt toward the US, leading to higher US regional premiums and wider inter-regional price differentials. Zinc re-pricing would be driven primarily by regional divergence rather than curve tightening.

-

Bear case (expectations fade, 10%–25%) The outcome of the Section 232 investigation proves relatively benign, or policy focus shifts to other commodities. Against a backdrop of rising inventories and improving liquidity, previously embedded policy risk premia are further priced out. Price formation increasingly reflects underlying supply-demand fundamentals and inventory dynamics, with regional differentials narrowing and policy influence diminishing.

Overall, zinc tariff expectations should be viewed as a marginal influence on regional pricing and cross-regional flows, rather than a decisive driver of LME structure. Going forward, close attention should be paid to developments in the Section 232 investigation, movements in US regional premiums, and the sustainability of inventory recovery to assess whether policy-related risks have been fully cleared.

Author: Yueang He, Zinc & Lead Analyst of SMM UK

Contact: yueanghe@smm.cn | +44 (0)7522 173725

![Macro Sentiment Repeatedly Shifted, SHFE Zinc Saw Wide Swings [SMM Daily Zinc Review]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)