In Q4 2025, the lithium battery industry chain underwent a deep transition from "destocking and recovery" to "sentiment-driven pulses." Lithium ore prices experienced wild swings in line with lithium carbonate futures and spot movements. In November, driven by futures limit-ups, prices entered an upward trend. By late December, suppliers, supported by stockpiling costs, continued to exhibit strong sentiment to hold prices firm. Backed by robust demand from the power and energy storage sectors, the lithium chemicals market entered a phase of significant destocking. The waste battery recycling market grappled with losses and price-following increases, while the discount coefficient for ternary black mass rose significantly, driven by cobalt and lithium prices. Looking ahead to Q1 2026, the market is expected to shift from emotional pulses back to rationality, seeking a new balance amid long-term contract negotiations, capacity releases, and seasonal demand pullbacks.

In Q4 2025, the lithium battery industry chain underwent a deep transition from "destocking and recovery" to "sentiment-driven pulses." Lithium ore prices experienced wild swings in line with lithium carbonate futures and spot movements. In November, driven by futures limit-ups, prices entered an upward trend. By late December, suppliers, supported by stockpiling costs, continued to exhibit strong sentiment to hold prices firm. Backed by robust demand from the power and energy storage sectors, the lithium chemicals market entered a phase of significant destocking. The waste battery recycling market grappled with losses and price-following increases, while the discount coefficient for ternary black mass rose significantly, driven by cobalt and lithium prices. Looking ahead to Q1 2026, the market is expected to shift from emotional pulses back to rationality, seeking a new balance amid long-term contract negotiations, capacity releases, and seasonal demand pullbacks.

I. Lithium Ore Market: Linkage with Futures and High-Price Firmness Struggles

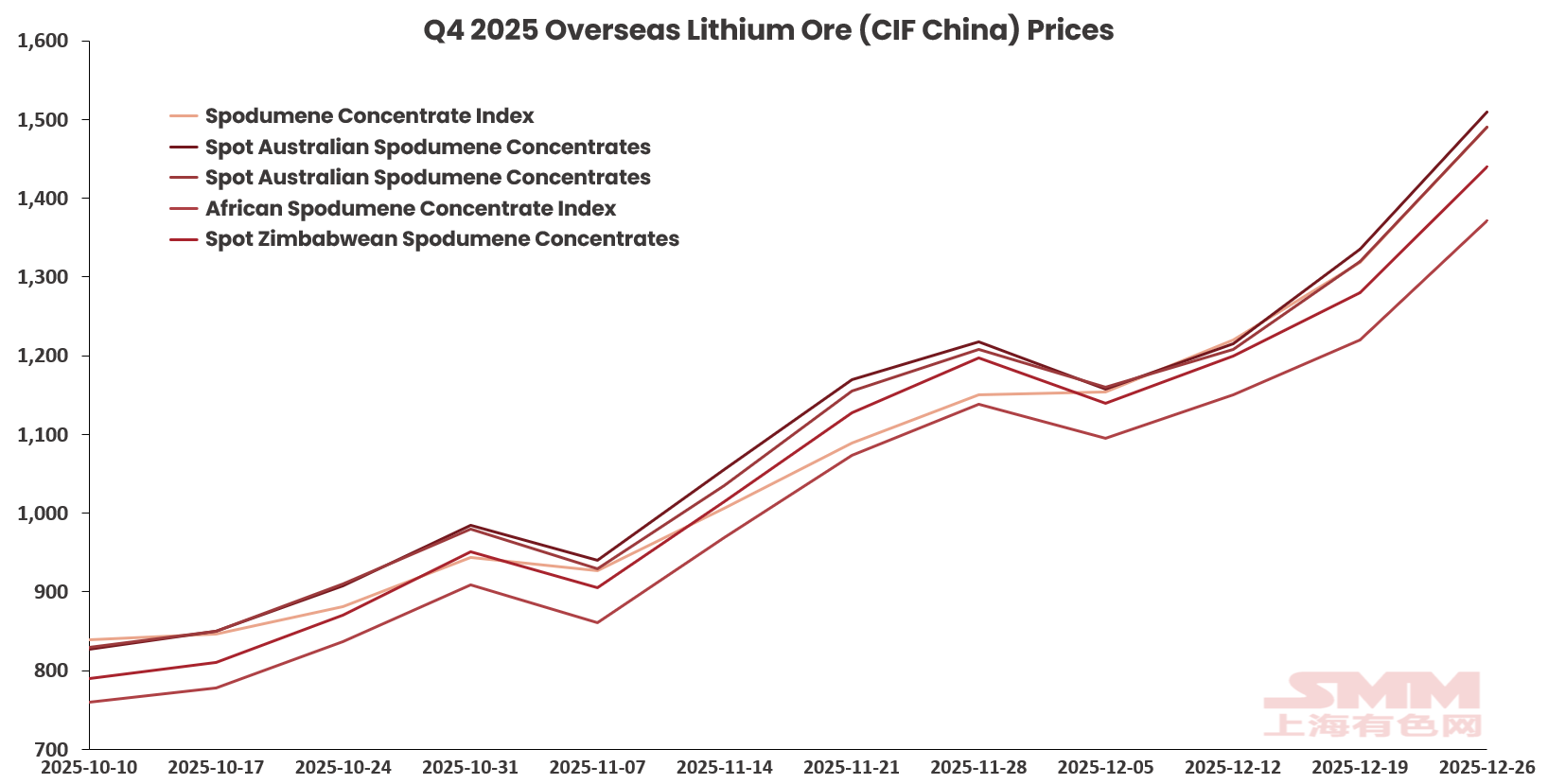

Image 1: Overseas Lithium Ore Price Trends

In Q4 2025, the lithium ore market exhibited strong price-following characteristics, with the price center transitioning from volatile stability to a strong upward trend, tracking lithium carbonate futures and spot movements. At the beginning of the quarter, operating rates at non-integrated lithium chemical plants were high. With lithium carbonate prices at elevated levels at the time, to maintain continuous production, there was sustained procurement demand for raw materials before the holiday and into the new year, leading to frequent inquiries and purchasing activities. This situation also heightened upstream lithium ore suppliers' sentiment to hold prices firm, resulting in fewer shipments. Additionally, port arrivals saw a slight drop back in October, causing the rate of lithium ore consumption in the market to exceed the volume of shipments. Both social inventory and in-factory inventory at lithium chemical plants showed a destocking trend. During this period, lithium ore prices oscillated above $800.

By November, lithium carbonate futures and spot prices continued to climb. Based on cautious observation of subsequent prices, upstream lithium ore mines increased the frequency of auction volumes. Buyers, seeking some hedging action amid the high futures levels, showed significantly increased acceptance of lithium ore prices. Consequently, auction transaction prices largely aligned with futures prices, to some extent guiding lithium ore market prices to remain persistently high. In December, scarce available spot ore for sale in the upstream lithium ore market led to continuously rising offers; suppliers slowed trading activity due to the fiscal year-end. Smelters had largely secured raw materials for pre-holiday production, so purchasing activity slowed. Coupled with lithium carbonate futures breaking through the 110,000 yuan mark, buyers adopted a cautious wait-and-see attitude towards the high lithium ore prices, resulting in mediocre transaction activity.

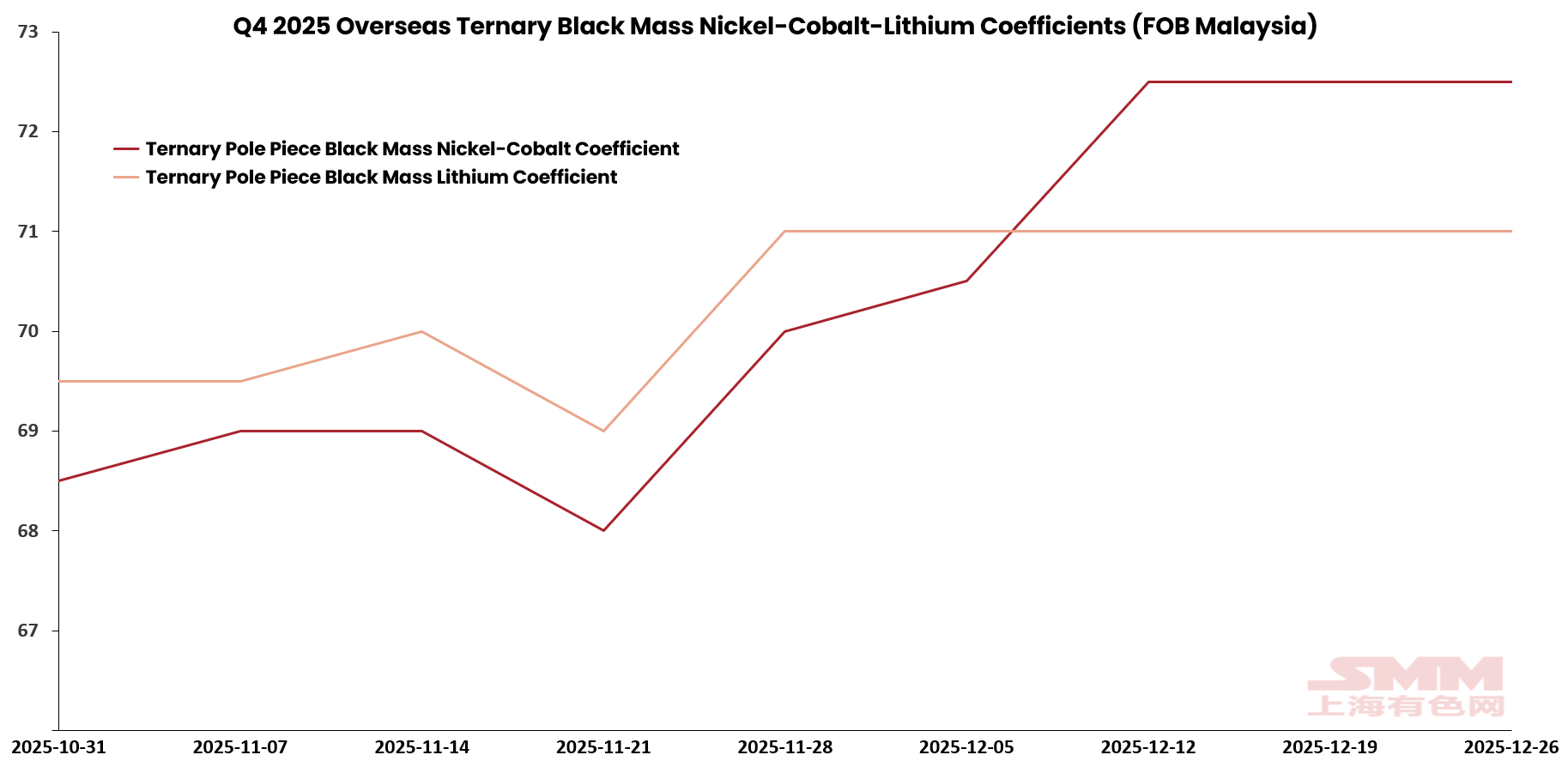

II. Waste Battery Market: Coefficient Struggles Amid Losses and Price-Following IncreasesFigure 2, FOB South Korea Ternary Black Mass Coefficient Trend

Image 2, FOB Malaysia Ternary Black Mass Coefficient Trend

Image 3: FOB Malaysia Ternary Black Mass Coefficient Trend

In Q4 2025, the recycled battery market was in a fierce tug-of-war between costs and profits. From October to early November, due to continuous losses from externally purchased LFP black mass for lithium carbonate production, profit margins remained at -5% to -6%. Apart from a few newly commissioned enterprises, most LFP recycling companies chose to halt production or only maintain B-end toll processing under the condition of losses. The situation in the ternary hydrometallurgy sector was similar, with profits hovering around 1% to 3%.

As lithium chemical prices surged significantly in mid-to-late November, recycling end profits improved with the recovery of salt prices. Due to advanced purchasing, the trading activity of LFP black mass increased substantially, and prices strengthened rapidly along with the rise in lithium chemicals. The price of LFP pole piece black mass rose from 3,050-3,300 yuan/mtu to 4,300-4,650 yuan/mtu by the end of December. Ternary and LCO black mass were supported by the continuous increase in cobalt sulphate prices, with discount coefficients showing a clear rise in December. The nickel-cobalt coefficient of FOB South Korea ternary pole piece black mass increased from 90% in early October to 95% by the end of December; the nickel-cobalt coefficient of FOB Malaysia ternary pole piece black mass also rose from 68.5% at the end of October to 72.5% by the end of December.

III. 2026 Q1 Outlook: Supply-Demand Tug-of-War and Rational Valuation Repair in the Industry Chain

Ore, Looking ahead to Q1 2026, global lithium ore supply is expected to exhibit characteristics of fluctuating at highs and releasing price elasticity. Although the main source of incremental lithium carbonate production will come from the release of integrated capacity, with an estimated YoY growth rate of around 30%, during the initial phase of the tug-of-war, the firm price-holding intentions of overseas ore suppliers will provide strong cost bottom support for lithium chemical prices. As the market gradually digests the emotional premium in December, ore trading activity is expected to return to a rational range amid the tug-of-war between "fluctuating at highs" and "restocking demand."

Salt, The core operation of the lithium chemical market in Q1 2026 will shift from "sentiment pulse" to "fundamental pricing." Domestic demand will be affected by the Chinese New Year holiday and the seasonal slowdown in the NEV market, leading to a significant contraction in cathode material production schedules in January, and destocking will slow down considerably compared to the strong momentum in November. It is expected that lithium chemical prices in Q1 will find a new balance under the combined influence of high-cost support and seasonal demand pullback.

Recycling, The recycled battery market in Q1 2026 will face a dual test of profit repair and off-season. As lithium chemical prices stabilize, the bargaining over discount coefficients in the recycling end will become more rational. Affected by the downward production schedules of downstream LFP and ternary material factories in January, the procurement pace of black mass and spent batteries is expected to slow down. The future market will focus on whether the recycling end can achieve long-term profit stability through a supply relaxation and stable salt prices after lithium prices return to fundamentals. It is expected that the prices of products such as LFP pole piece black mass will enter a fluctuating at highs range as lithium chemical prices stabilize.