According to the latest data released by the World Steel Association (WorldSteel), global crude steel production reached 140.1 million tonnes in November 2025, representing a 4.6% year-on-year (YoY) decrease. Cumulative production from January to November totaled 1.6622 billion tonnes, down 2% YoY.

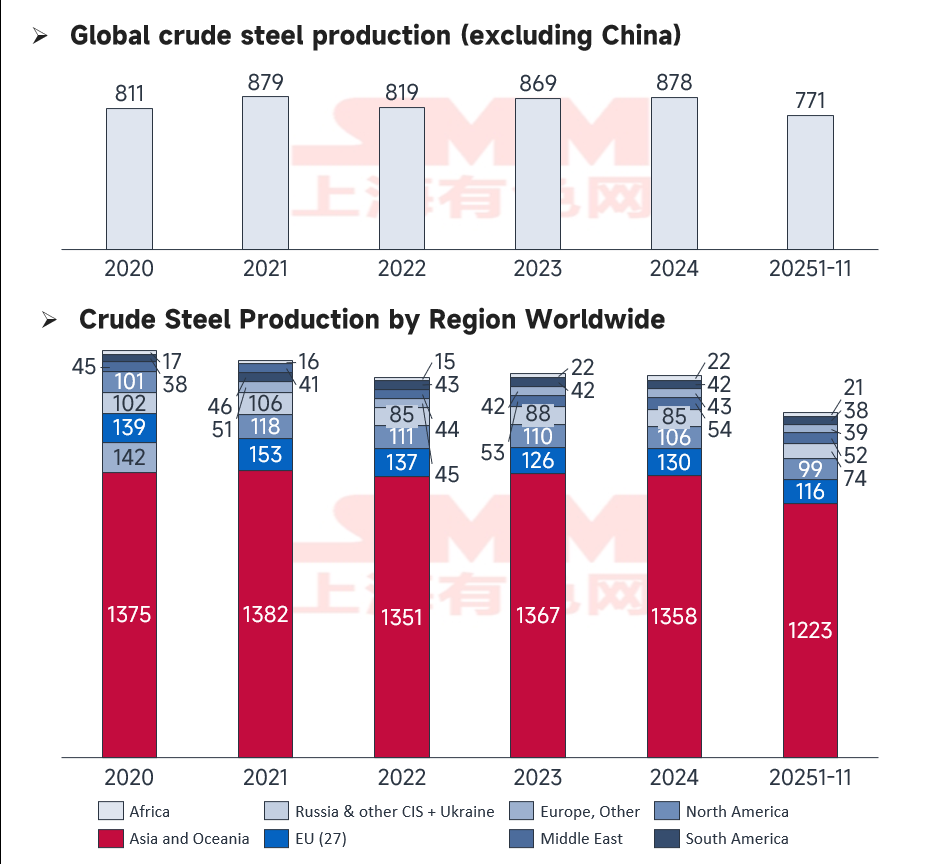

Excluding China, cumulative production in the rest of the world grew by 0.67% during the first 11 months, indicating a modest recovery in overseas markets. However, growth momentum varies significantly across regions. The core trend reinforces a pattern of "Emerging Market Growth vs. Traditional Hub Contraction" with particularly stark performance gaps within the EU, Middle East, Africa, and the Asia-Pacific region.

Source: WSA

Global Performance and Structural Shifts

Source: WSA

While global output remains in a slight contraction on a cumulative basis, regional performance is highly polarized. Production in Asia and Oceania fell by 7.1% in November, primarily due to weak demand in major economies like China and Japan.

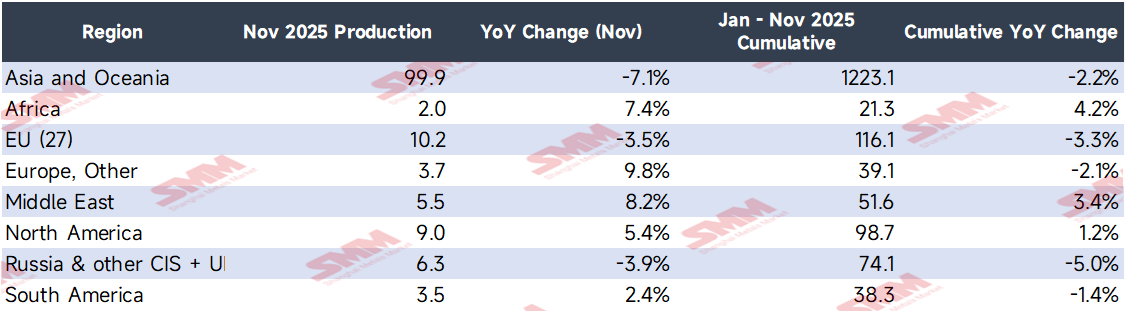

Notably, a "bipolar" phenomenon has emerged within Europe: while the EU (27) saw a 3.5% decline, Other Europe (Non-EU) surged by 9.8%. This structural shift reflects a realignment of production capacity under the EU’s green transition policies. Russia and other CIS countries saw a 3.9% decline, highlighting the persistent impact of geopolitical factors on heavy industry. Conversely, India, the U.S., and the Middle East showed robust performance, bolstered by policy support and infrastructure development.

Detailed Analysis of Regional and National Changes

High-Growth Regions

-

Other Europe (+9.8% in Nov): Production rose to 3.7 million tonnes. This surge is attributed to:

-

The implementation of the Carbon Border Adjustment Mechanism (CBAM), causing EU buyers to shift orders to non-EU mills like those in Turkey.

-

Turkey's strategic geographic advantage in securing EU infrastructure contracts.

-

A recovery in the UK steel industry driven by industrial subsidies and electricity cost offsets for energy-intensive sectors.

-

-

Africa (+7.4% in Nov): Output reached 2 million tonnes, driven by the completion of technical upgrades at South African mills and accelerated infrastructure projects in Egypt, including the New Administrative Capital and Suez Canal Economic Zone expansions.

-

Middle East (+8.2% in Nov): Production reached 5.5 million tonnes. Saudi Arabia led this growth due to Saudi Aramco's localized procurement for oil and gas pipelines, the full-scale construction of the NEOM mega-city, and new capacity coming online from SABIC.

Analysis of Key Growth Countries

-

India (+10.8% in Nov): Output hit a record 13.7 million tonnes. The National Highways Authority of India (NHAI) projects reached peak construction for the Delhi-Mumbai Industrial Corridor, increasing monthly steel procurement by 30%. Additionally, Tata Steel's new blast furnace reached full capacity, and EV subsidies boosted automotive steel orders by 22%.

-

United States (+8.5% in Nov): Output reached 6.8 million tonnes, supported by Inflation Reduction Act (IRA) tax credits for clean energy production lines, expanded anti-dumping investigations on imported steel, and demand from EV plant construction by GM and Ford.

-

Turkey (+10.0% in Nov): Production reached 3.3 million tonnes, benefiting from a shift in construction steel orders from Germany and Italy due to rising carbon costs, as well as post-earthquake reconstruction demand.

-

Iran (+9.2% in Nov): Production rose to 3.4 million tonnes, driven by NIOC refinery upgrades, peak construction in government affordable housing, and increased export competitiveness due to currency depreciation.

Source: WSA

Analysis of Declining Countries

-

China (-10.9% in Nov): Production fell to 69.9 million tonnes. Beyond annual "Winter Environmental Restrictions" local governments (particularly in Hebei and Tangshan) enforced stricter "Flat Control" (zero-growth) targets for 2025. Daily average hot metal production fell to 9.57 million tonnes (down 1.6% YoY). Low market prices and thin margins also prompted mills to extend maintenance cycles for blast furnaces.

-

Russia (-6.6% in Nov): Output fell to 5.2 million tonnes. This was caused by the 11th EU Sanctions Package technical embargo affecting equipment maintenance, fiscal budget adjustments slowing domestic infrastructure, and supply chain issues in the automotive sector.

-

South Korea (-4.8% in Nov): Output dropped to 5.0 million tonnes due to a lack of new orders for shipbuilders like Hyundai Heavy Industries, environmental retrofitting at POSCO plants, and a slowdown in the construction sector caused by high interest rates.

-

EU (27) (-3.5% in Nov): Decline was driven by rising Carbon Emission Allowance costs (impacting majors like Thyssenkrupp), high energy prices forcing Electric Arc Furnaces (EAF) to reduce operating rates, and a rapid decline in traditional automotive steel demand during the EV transition.

Source: WSA

Outlook and Forecast for December

Looking ahead to December:

-

India is expected to maintain strong growth as year-end fiscal spending on infrastructure accelerates.

-

The Middle East and Africa will likely see stable growth driven by mega-projects and year-end construction deadlines.

-

The U.S. is expected to remain steady under tariff protections and infrastructure act implementations.

-

The EU will remain under pressure due to the dual burden of carbon costs and peak winter energy demand.

-

China is projected to see a further month-on-month (MoM) and YoY decline. Production constraints remain tight, and the market is entering the traditional "off-season" for winter demand.

Conclusion: The global steel market is in a phase of deep structural adjustment. Regional policies, the energy transition, and supply chain "near-shoring" will remain the defining factors for capacity layout. The development of Green Steel technology and regional trade agreements will fundamentally reshape the competitive landscape.

![[SMM Steel] Jindal Steel wins a new iron ore mine in Odisha with ~38 mt reserves](https://imgqn.smm.cn/usercenter/jUyJR20251217171716.jpg)

![Silicon Metal Prices Tested Higher as Market Transactions Remained in Stalemate, While Polysilicon Prices Trended Downward [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)

![[SMM Daily HRC Trading Volume] Futures Continued to Rise, Spot Trading Continued to Recover](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)