SMM Steel, December 30 — According to SMM statistics, the estimated total resource shipments in mainstream markets this week were 219,800 mt, down 18.71% WoW from last week’s shipment level. By market:

Table 1: Comparison of Mainstream Market Arrivals

Data source: SMM Steel

Shanghai market: Shipments in the Shanghai market decreased WoW. Specifically, shipments of mainstream resources from Northeast, North, and South China all declined, while shipments to the East China market remained flat. Looking ahead, although Shanghai market prices edged up recently, market transactions remained relatively weak, and merchants’ ordering enthusiasm was moderate. Arrivals are expected to see limited growth next week.

Chart 1: Shanghai Market Arrivals

Data source: SMM Steel

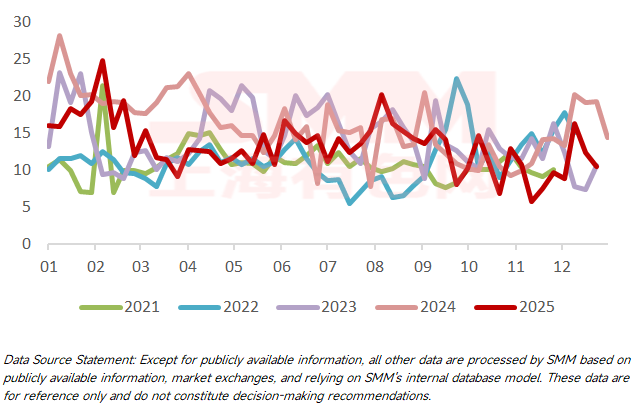

Lecong market: Shipments to the Lecong market continued to pull back WoW. Specifically, at current prices in South China, it is difficult for northern resources to arrive, so the difference in arrivals is mainly affected by local mainstream resources. East China had more backlogged shipments previously, and WG has a stronger tendency to ship to East China. Looking ahead, as other products of mainstream steel mills are more profitable, there are plans to transfer hot metal, so arrivals in the South China market are expected to remain low in the short term.

Chart 2: Lecong Market Arrivals

Data source: SMM Steel

SMM releases hot metal shipment data for mainstream market flows every Tuesday. To subscribe or follow more other data, please scan the QR code below.

![[SMM Steel] Jindal Steel wins a new iron ore mine in Odisha with ~38 mt reserves](https://imgqn.smm.cn/usercenter/jUyJR20251217171716.jpg)

![Silicon Metal Prices Tested Higher as Market Transactions Remained in Stalemate, While Polysilicon Prices Trended Downward [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)

![[SMM Daily HRC Trading Volume] Futures Continued to Rise, Spot Trading Continued to Recover](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)