SMM Report, February 12

Since January, the domestic molybdenum market in China has seen a slight rebound. At the beginning of January, domestic mines shipped goods intensively. Against the backdrop of low industry inventories, the focus of mine auction prices moved upward, driving a mild rise in market prices early in the month. However, the price increase was constrained by poor profitability of downstream steel mills and the weak import molybdenum oxide market in the middle of the month.

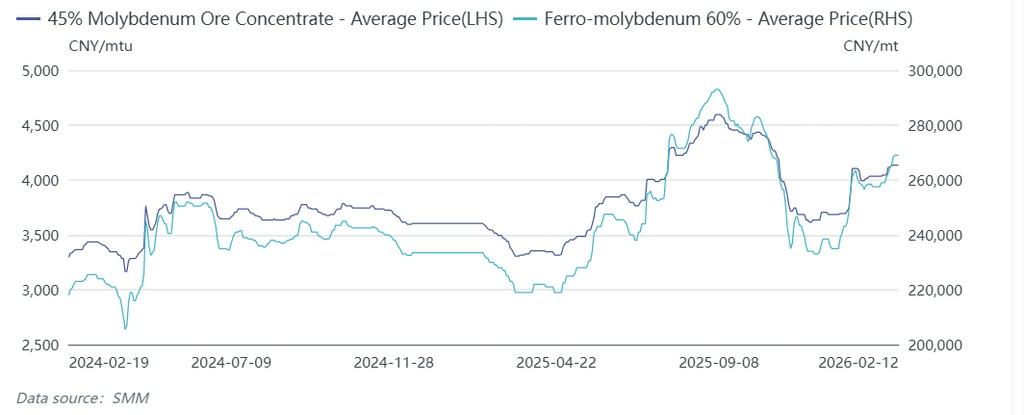

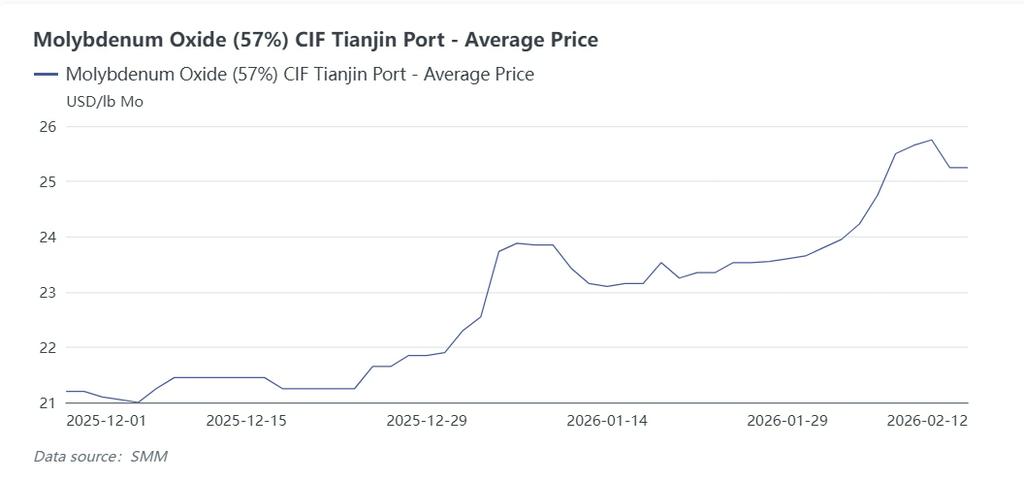

According to SMM data, the average monthly price of domestic 45% molybdenum concentrate in January was approximately 4,036 yuan per ton-degree, up 9.7% month-on-month. The average CIF price of imported molybdenum oxide at Tianjin Port in January was about 23.43 USD/lb Mo, up 9.3% month-on-month.

In January, supported by rising costs and increased winter stockpiling demand from downstream steel mills, ferromolybdenum prices rose compared with earlier levels. However, sharp increases in nickel, chromium and other raw material costs squeezed stainless steel margins significantly. Most stainless steel enterprises adopted price-suppressing tenders for ferromolybdenum, resulting in smaller gains for ferromolybdenum than for raw materials. The average monthly price of domestic ferromolybdenum in January was around 258,750 yuan per ton, up roughly 9% month-on-month.

Entering February, supply disruptions in overseas molybdenum raw material markets have intensified, and international molybdenum oxide prices have risen rapidly, boosting the domestic molybdenum market. In addition, as the Spring Festival approaches, downstream molybdenum smelting and chemical enterprises have restocking demand. Supported by multiple positive factors, the molybdenum concentrate market has moved higher again. Nevertheless, gains are limited due to weak downstream steel demand during the seasonal off-season.

As of today, domestic 45% molybdenum concentrate is quoted at 4,120–4,150 yuan per ton-degree, up 6.4% from early January. Asian molybdenum oxide prices have climbed to 26 USD/lb Mo.

In the US, a fire incident at a major molybdenum producer triggered a sharp jump in domestic US molybdenum prices, with molybdenum oxide offers reaching 36 USD/lb Mo. Strong reluctance among overseas molybdenum oxide producers to sell is evident. The molybdenum market is expected to remain in a strong oscillation trend after the Spring Festival.

① Frequent news of production cuts at overseas copper-molybdenum mines in Chile, Peru and other regions has tightened supply in overseas molybdenum concentrate and molybdenum oxide markets.

In early January, workers at Capstone Copper’s Mantoverde copper mine in Chile failed to reach a collective bargaining agreement, leading to a strike and production suspension on January 2, with associated molybdenum recovery restricted.

In early January, Finning Union #2 intermittently blocked the La Negra access corridor (a key transportation and utility hub), affecting shift changes and material delivery. Major mines including Escondida and Zaldívar saw temporary declines in operating efficiency. An agreement was reached on January 25 and the corridor resumed operation. Although no substantial production loss occurred, it exposed the vulnerability of transportation in northern mining areas, tightened short-term molybdenum concentrate circulation, and stimulated a rapid rally in overseas molybdenum oxide spot prices, with strong linkage between domestic and overseas prices.

As international molybdenum oxide prices rose, Tianjin port molybdenum oxide and molybdenum concentrate quotes followed higher, import margins narrowed, and domestic buying interest weakened. China’s imports of molybdenum raw materials are expected to drop month-on-month in January–February.

② A fire at a US molybdenum plant further stimulated market gains.On the evening of January 29, 2026 (local time), an explosion occurred at The Langeloth Metallurgical Facility in Pittsburgh, Pennsylvania. The plant mainly produces molybdenum oxide and ferromolybdenum, with monthly capacities of about 1,200 tons and 500 tons respectively. It is currently the only major operating ferromolybdenum producer in the US, holding a prominent position in the supply chain.

The incident led to a rapid rise in US molybdenum oxide and ferromolybdenum prices with firm offers, drawing some overseas molybdenum products into the US market. According to market feedback, US molybdenum oxide prices rose to 36 USD/lb Mo, more than 10 dollars above the Asian market.

③ In February, mine shipments declined ahead of the Spring Festival, tightening market availability.According to SMM data, the operating rate of domestic molybdenum concentrate mines in January was around 73%, with output rising only 2.2% month-on-month. A large mine in Heilongjiang underwent maintenance for 10–15 days at the end of January and has not yet resumed production.

Although some mines in Xizang and Inner Mongolia expanded production, domestic molybdenum concentrate supply is expected to contract slightly in February. Tightening supply, coupled with partial mine shipments in early February, pushed up spot transaction prices. Meanwhile, environmental controls in Henan and other regions affected mill operations, further tightening spot availability.

④ Off-season demand before the holiday; sharp decline in stainless steel scheduling; restocking demand expected to rebound after the holiday.In January, sharp increases in nickel, chromium and other raw material costs squeezed stainless steel profits significantly. Most stainless steel enterprises suppressed ferromolybdenum tender prices, leading to narrower ferromolybdenum gains relative to costs and poor industry profitability.

According to SMM, the average cost of domestic ferromolybdenum in January was about 260,500 yuan per ton, with an average industry loss of 1,700 yuan per ton during the month.

Affected by poor profitability and weakening pre-holiday demand, domestic ferromolybdenum operating rates fluctuated narrowly in January. Based on SMM sample data, domestic ferromolybdenum output in January rose 0.72% month-on-month but fell 12.3% year-on-year, with an industry operating rate of around 47%. Some small and medium-sized ferromolybdenum producers actively reduced operating rates, while leading processors with own mines maintained operating rates above 85%.

In terms of stainless steel scheduling:

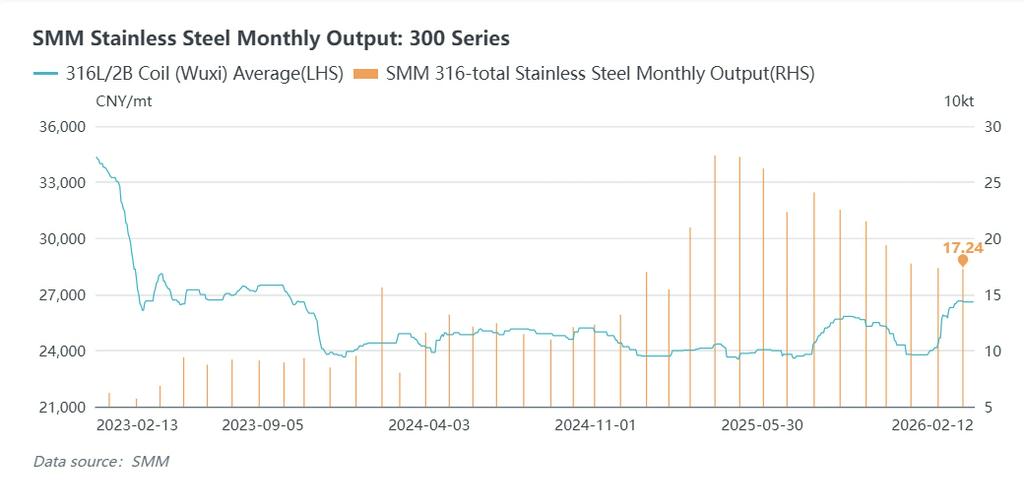

- January national stainless steel output: 3.381 million tons, up 4.64% month-on-month and 12.53% year-on-year.

- 200 series: 990,000 tons (+9.63% MoM)

- 300 series: 1.787 million tons (+1.71% MoM)

- 400 series: 604,000 tons (+5.78% MoM)

Steel mills entered the market intensively for tenders in January, with total tender volume around 14,300 tons.

February stainless steel scheduling is set to drop sharply under multiple pressures.Estimated February national stainless steel output: 2.567 million tons, down 24.08% month-on-month.

- 300 series: 1.246 million tons, down 30.27% (the largest drop)

- 200 series: 808,000 tons, down 18.38%

- 400 series: 513,000 tons, down 15.07%

Part of the follow-up demand was front-loaded in January. February stainless steel demand is expected to remain weak, constraining ferromolybdenum market performance.

Overall View

From January to date, the domestic molybdenum market has been characterized by “dual constraints from supply and demand, with oscillating price rebounds”. The core driver is the game between positive overseas supply disruptions and weak domestic downstream demand, leaving little room for a one-sided market. Prices trended upward but with limited gains.

Molybdenum concentrate was the main driver of the rebound, supported by tighter overseas supply, lower domestic mine shipments, and rigid downstream restocking demand. Ferromolybdenum was underpinned by costs but capped by stainless steel price suppression. Widespread industry losses limited operating rates and ferromolybdenum gains lagged those of molybdenum concentrate.

In the short term, the approaching Spring Festival will continue to weigh on domestic mine shipments, keeping molybdenum concentrate circulation tight. Uncertainty over the restart of the fire-hit US molybdenum plant and lingering transportation risks at Chilean mines will keep overseas molybdenum prices high, supporting domestic market sentiment.

After the holiday, reduced imported ore arrivals and slow domestic mine shipment schedules are expected to keep molybdenum concentrate supply tight. While weak February steel scheduling will cap ferromolybdenum demand, post-holiday resumption and restocking, plus long-term demand growth from manufacturing upgrading, will support molybdenum-containing stainless steel and molybdenum chemical consumption.

Medium to long term, the global molybdenum market will remain in a tight supply-demand balance in 2026, driven by sustained demand from new energy and high-end manufacturing amid limited new mine capacity. SMM estimates a global supply-demand deficit of around 13,000 metric tons in 2026, providing strong fundamental support for molybdenum prices.

In early February, Chile included molybdenum among its first-tier critical minerals, with a 14.6% share of global supply. The country aims to strengthen resource development as a stable supplier and diversify its mining sector beyond copper. This strategy elevates molybdenum’s strategic status in Chile’s mining industry and the global critical mineral landscape, benefiting the long-term molybdenum price floor and supply chain resilience, while intensifying global competition and cooperation over molybdenum resources.

![Overseas Molybdenum Market Rises Along with Increased Stocking Demand from Domestic Steel Mills, Molybdenum Market Advances [SMM Molybdenum Daily Review]](https://imgqn.smm.cn/usercenter/gKDYO20251217171723.jpeg)

![Post-Holiday Molybdenum Ore Rebounds, Ferromolybdenum Tender Center Rises [SMM Molybdenum Daily Review]](https://imgqn.smm.cn/usercenter/eThpo20251217171723.jpeg)