SMM News, December 29th

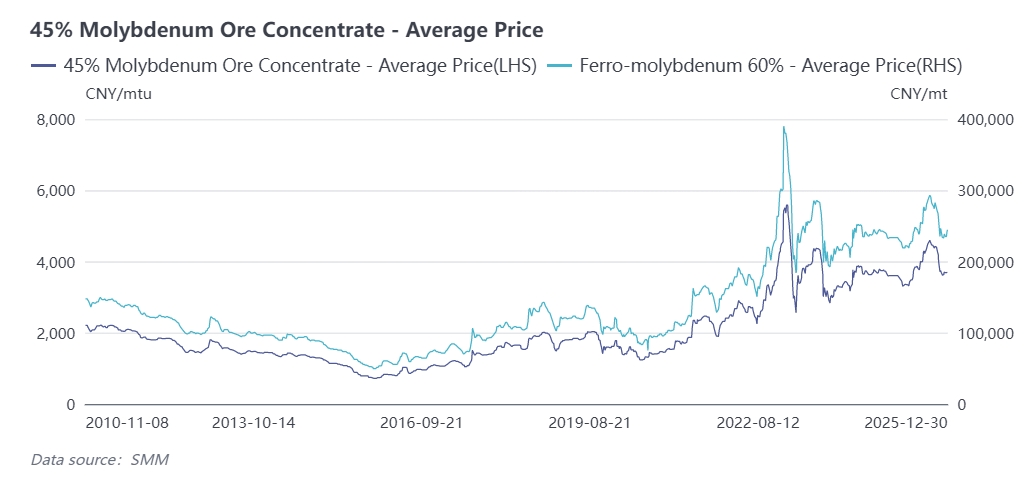

The molybdenum market fluctuated sharply in 2025, generally experiencing a rally followed by a pullback. In the first three quarters, boosted by tight supply and prominent strategic attributes, molybdenum prices kept rising: 45% molybdenum concentrate hit a record high of 4,600 CNY/ton-unit in early September 2025, and ferromolybdenum prices peaked at 293,000 CNY/ton. Thereafter, prices retreated from highs constrained by the impact of imported overseas molybdenum raw materials and the emergence of a demand off-season.

As of December 29th, domestic 45% molybdenum concentrate closed at 3,695 CNY/ton-unit, a year-on-year increase of 25%, with an annual average price of about 3,836 CNY/ton-unit in 2025, up 6.7% year-on-year. SMM ferromolybdenum closed at 243,000 CNY/ton as of December 29th, a year-on-year rise of 10.5%, and the annual average price stood at 247,100 CNY/ton, surging 16.4% year-on-year, reflecting a notable uplift in the annual price core level.

As a strategic scarce metal, the molybdenum market’s supply-demand pattern profoundly reflects the dual impacts of industrial upgrading and resource regulation. In recent years, driven by growing demand for molybdenum-bearing steel, the global molybdenum supply is likely to remain tight. The core theme of "rigid supply hard to break, demand surging from multiple sectors" will prevail, and the molybdenum market is expected to be mainly driven by the supply side with volatile movements before the concentrated

Supply Side First: Limited Output Growth from New Mines, Widespread Grade Decline in the Industry

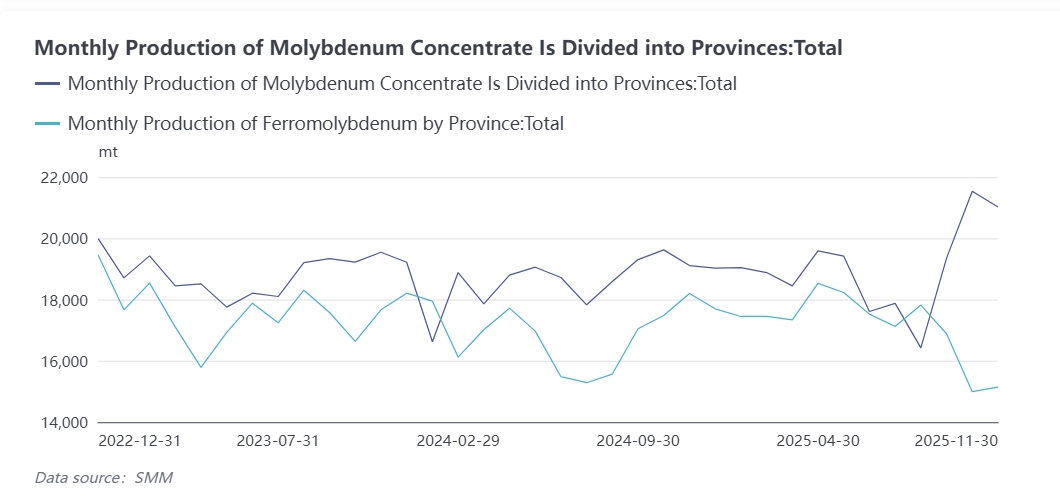

New molybdenum concentrate mines globally were scarce in 2025, with incremental output only from a few new mines in Jilin, Xizang and other regions of China. As a well-known fact, China is the world’s largest molybdenum concentrate producer, playing a pivotal role in the global molybdenum supply system, with its output accounting for 40%-48% of global molybdenum production from 2021 to 2024. Over the past five years, driven by rising molybdenum prices and mine capacity expansion/technical upgrading, China’s molybdenum output has maintained a slow overall growth.In 2025, technical renovations at mines in Henan, Inner Mongolia and other regions in the middle of the year, coupled with lower operating rates at some mines, slowed the growth rate of domestic molybdenum concentrate output again. According to SMM data, cumulative domestic output from January to November reached approximately 295,000 physical tons, a year-on-year increase of 5%, maintaining annual growth momentum.SMM forecasts that China’s total molybdenum concentrate output in 2025 will reach 320,000 physical tons (equivalent to 143,000 metal tons), accounting for 48.4% of global total supply, up 4.2% year-on-year, while the global supply growth rate will stand at about 1.9%.Domestic molybdenum concentrate production capacity is relatively concentrated, mainly distributed in Henan, Inner Mongolia, Shaanxi, Heilongjiang and other provinces, with the specific breakdown as follows:

- Henan Province: The highest output at ~89,000 tons, accounting for 29% of national total output;

- Inner Mongolia Autonomous Region: ~46,000 tons, 15% of national total;

- Shaanxi Province: ~37,000 tons, 12.1% of national total;

- Heilongjiang Province: ~36,500 tons, 11.9% of national total.The four major provinces together account for about 68% of national output, and the remaining provinces account for the other 32%.

Entering 2026, the Phase II project of a mine in Xizang will be put into operation and ramp up production, bringing an annual incremental molybdenum supply of 6,000 tons of molybdenum concentrate. Considering the operating fluctuations of other mines, SMM forecasts that China’s molybdenum concentrate output growth rate will drop to 3% in 2026, reaching around 328,000 physical tons.On the overseas supply side, increments remain limited and highly uncertain. Overseas molybdenum supply growth mainly relies on the capacity ramp-up of Teck Resources’ QB2 project, but the overall scale is limited; copper mining in major producing countries such as Chile and Peru will still face multiple disruptions including environmental protection, water resources and strikes, leading to little room for a sharp increase in by-product molybdenum output, and even the risk of a decline. In addition, insufficient global molybdenum mine exploration investment and a long construction cycle of 3-5 years for new mines mean no significant short-term supply growth.Given these factors, before the commissioning of large domestic new capacity projects such as the Jinzhai Shapinggou molybdenum mine, output growth of existing major mines will continue to slow down due to grade decline and rising mining costs, and annual molybdenum mine output is likely to maintain low-speed growth. SMM forecasts that global molybdenum concentrate output will increase by 2.7% year-on-year to around 303,000 metal tons in 2026.

China’s Molybdenum Market Maintains a Net Import Pattern

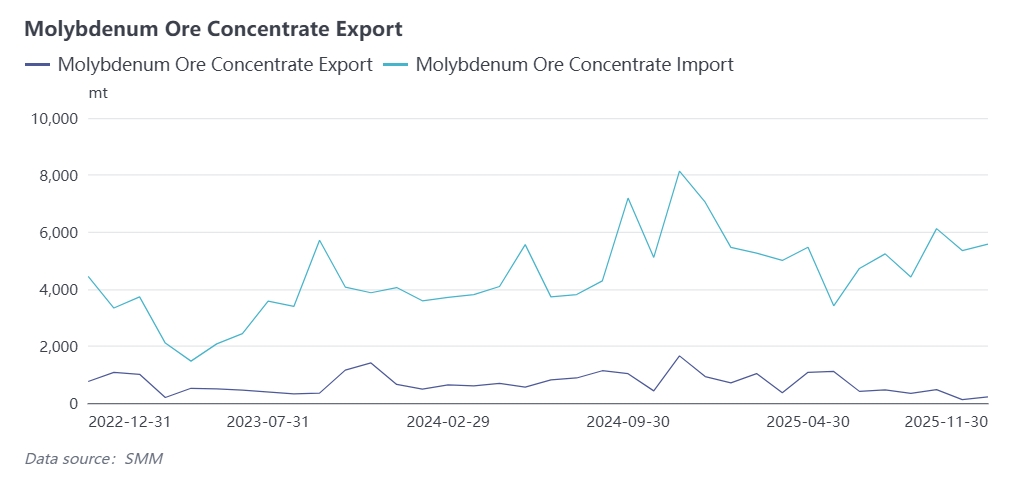

China’s imports of molybdenum raw materials have rebounded significantly and maintained rapid growth since 2023. According to customs data:

- In 2023, total imports of molybdenum raw materials (mainly molybdenum concentrate and molybdenum oxide) reached 50,800 tons, a year-on-year increase of 23.3%, driven by the normalization of supply chains and improved supply stability in major international producing countries, as well as rising downstream demand for molybdenum products boosted by the recovery of domestic manufacturing and steel industries;

- In 2024, imports continued to expand, with total imports of molybdenum raw materials hitting 66,500 tons, a year-on-year rise of 31%;

- In 2025, domestic molybdenum prices fluctuated at high levels, and coupled with exchange rate fluctuations such as RMB appreciation, China’s molybdenum import window remained continuously open, stimulating a sharp growth in imports of molybdenum concentrate, molybdenum oxide and other molybdenum products. According to SMM’s China molybdenum oxide import profit model, the domestic molybdenum oxide import profit from January to October 2025 was about 0.78 USD/lb molybdenum, compared with a slight loss in 2024, which boosted overseas holders’ enthusiasm for shipping to China.

Customs data shows that total imports of molybdenum concentrate and molybdenum oxide from January to October 2025 reached approximately 63,800 tons, a year-on-year increase of 26.6%.

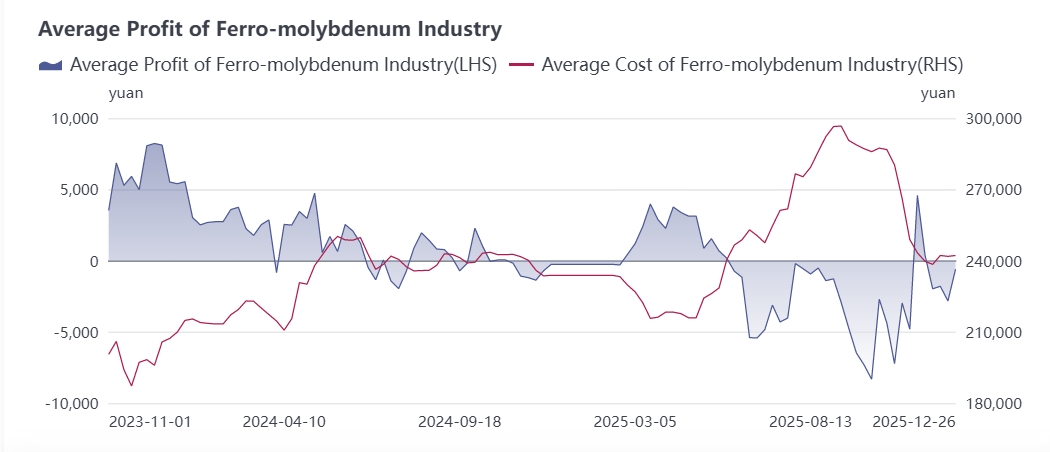

Ferromolybdenum Market: Overcapacity Worsened in 2025, Poor Industry Profitability

As the primary smelting product of the molybdenum industry, ferromolybdenum’s operating rate and profitability constrain the upstream molybdenum concentrate market and affect the downstream molybdenum-bearing special steel and 316 stainless steel markets.In 2025, the molybdenum concentrate market led the rally in the molybdenum industry, while downstream industries such as stainless steel faced severe internal competition with slow price follow-up, putting great cost pressure on steel mills, which thus suppressed ferromolybdenum procurement prices. In recent years, new ferromolybdenum capacity has continued to grow, leading to industry overcapacity. Amid market competition, some ferromolybdenum plants with upstream resource advantages enjoy cost edge and large market price spreads, while enterprises without competitive advantages have to cut production due to loss-making orders, leaving the industry operating rate at the range of 50%-60%.

According to SMM data:

- Domestic ferromolybdenum output from January to November 2025 rose 9% year-on-year to around 200,000 tons;

- Total domestic ferromolybdenum tenders from January to November 2025 reached 139,500 tons, a year-on-year increase of 5.5%. With downstream demand for stainless steel and special steel entering the off-season in Q4, ferromolybdenum demand is expected to decline from the previous period. SMM forecasts total domestic ferromolybdenum steel tenders in 2025 will hit 152,000 tons, up 4.8% year-on-year, accounting for about 70% of domestic ferromolybdenum production.

Entering 2026, driven by demand for steel in terminal sectors such as new energy, global steel demand will continue to shift to molybdenum-bearing steel such as special steel, boosting domestic ferromolybdenum market demand. However, against the backdrop of a large ferromolybdenum capacity base, the industry will still face fierce competition and further industrial optimization.

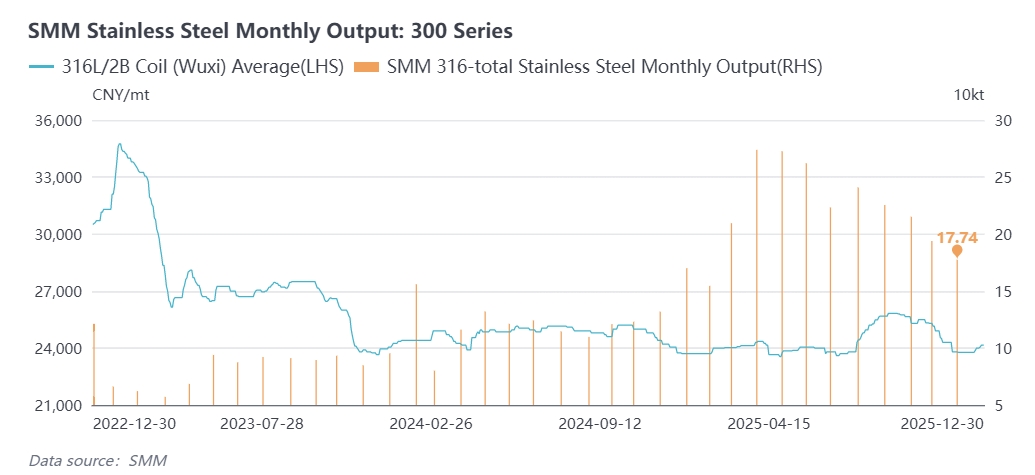

Terminal Demand: Structural Adjustment in Steel Market Demand, 300 Series Stainless Steel Growth to Drive Molybdenum Consumption

The role of molybdenum in steel can be summarized as improving hardenability, thermal strength, preventing temper brittleness, increasing remanence and coercivity, enhancing corrosion resistance in certain media, and preventing pitting tendency. Benefiting from these beneficial effects, molybdenum is widely used in a series of steel grades including structural steel, spring steel, bearing steel, tool steel, stainless acid-resistant steel, heat-resistant steel (also known as heat-strength steel) and magnetic steel.

As the 14th Five-Year Plan concludes, the most critical change in the steel industry focuses on the historic shift in downstream demand structure: steel consumption in traditional sectors such as real estate has declined, while demand for alloy steel for infrastructure, new energy installed capacity, high-strength steel and superalloys in new energy vehicles has surged, driving the demand outlook for molybdenum-bearing special steel and stainless steel.

On December 12, 2025, the Ministry of Commerce and the General Administration of Customs jointly issued Announcement No.79, deciding to adjust the Catalogue of Goods Subject to Export License Administration (2025). The document includes 300 customs commodity codes for steel products under export license administration, covering the entire industrial chain from raw materials to finished products, among which about 64 codes are related to stainless steel.The core objective is to rely on the export license management system to drive the export structure toward high value-added and high-tech products, achieving the dual goals of industrial upgrading and trade quality improvement, rather than adopting a one-size-fits-all total volume control approach. During the policy transition period, exports of low-end ordinary stainless steel products may decline, leading to an expected reduction in molybdenum demand in the stainless steel market to a certain extent. In the long run, as a key raw material for stainless steel, the molybdenum market will witness corresponding changes, with demand for high-quality molybdenum products rising alongside the growth of high-end stainless steel.

Domestic steel mills are continuously upgrading their product structure from ordinary steel to high-grade special steel, which directly increases molybdenum consumption per ton of steel. SMM forecasts that China’s molybdenum consumption growth rate will reach 4% in 2026, hitting around 172,000 metal tons, and global molybdenum consumption is expected to reach 316,000 metal tons.

Macroeconomic Policy: Federal Reserve Remains in Rate Cut Cycle, Boosting Nonferrous Metals Market

The Federal Reserve launched an interest rate cut cycle in the second half of 2025: it cut rates by 25 basis points (bp) in September, lowering the target range for the federal funds rate to 4.00%-4.25%, and another 25bp in October, further reducing the range to 3.75%-4.00%. According to the latest CME FedWatch Tool, there is a 71% probability of a 25bp rate cut in December, and on this basis, there is a high probability of an additional 50bp rate cut in 2026.The independence of the Federal Reserve’s monetary policy is questionable, and its monetary easing policy has boosted the metals market, indirectly benefiting the development of the molybdenum industry.

Comprehensive Outlook

The global molybdenum market supply-demand pattern underwent a fundamental shift in 2025, with supply contraction and demand differentiation creating a supply-demand gap of 18,000 metal tons; in 2026, rigid supply constraints will remain unresolved, and demand will grow synergistically in both traditional and emerging sectors, leaving a supply-demand gap of 10,000-20,000 metal tons. This tight supply-demand balance will provide strong support for molybdenum prices, and the medium-to-long-term molybdenum price core is expected to continue moving upward, ushering the industry into a high-quality development stage driven by supply-demand gaps and structural upgrading.

As the world’s major molybdenum producer and consumer, China will mainly rely on net imports to supplement supply amid tight global supply and demand. Fluctuations in overseas molybdenum prices and domestic seasonal demand changes will cause volatility in the domestic molybdenum market.

2026 marks the first year of the 15th Five-Year Plan, and infrastructure investment is the key to underpinning the economy. China will continue to stabilize investment, increase central budgetary investment, optimize major projects in key fields, and implement major projects in urban renewal and strategic backbone channels during the 15th Five-Year Plan period (including the already under-construction hydropower project in the lower reaches of the Yarlung Zangbo River and Xinjiang-Xizang Railway). SMM forecasts that infrastructure investment growth rate will stabilize and rebound in 2026, which will also boost the demand outlook for the molybdenum market.