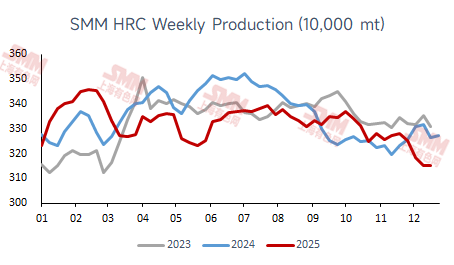

- Hot Rolled Coil Production Fell 2.7% MoM in December, with Output Lower Than the Same Period Last Year

According to SMM data, the average weekly production of hot rolled coils in China was 3.185 million tonnes in December, down from the same period last year and falling 2.7% MoM from November, mainly due to increased annual maintenance at domestic steel mills in December.

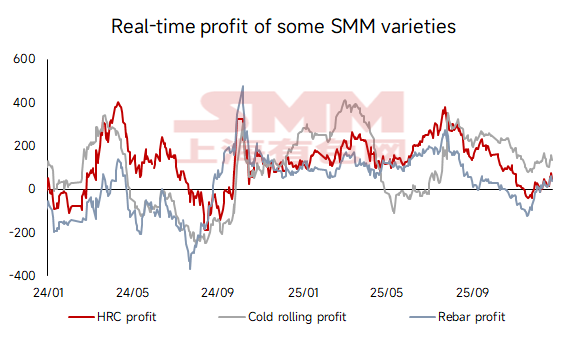

- In December, raw material prices declined while steel prices rose rangebound, and steel mill profits expanded slightly.

In December, on the raw material side, iron ore prices fluctuated rangebound MoM, coke prices experienced two rounds of increases followed by three rounds of decreases, with the monthly average price down MoM, and steel scrap prices dropped slightly. Overall, steel mill costs fell by an average of 1.0% in December. On the finished steel side, amid the off-season, demand support was insufficient, but reduced steel mill production alleviated market pressure to some extent. Steel prices fell first and then rose, with the monthly average increasing rangebound by 0.9%. With costs declining and steel prices rising, steel mill profits expanded slightly in December. Among them, hot-rolled profits recovered from an average of -1 yuan in November to 27 yuan/mt, rebar profits recovered from -82 yuan to 14 yuan/mt, and cold-rolled profits fluctuated rangebound from 125 yuan to 129 yuan/mt.

- Steel mill maintenance impact slightly decreased in January, with production growth pace expected to accelerate in mid-to-late January.

According to SMM statistics on steel mill maintenance, the impact from maintenance on hot-rolled coil production in January is temporarily 649,900 mt, down 1.0129 million mt MoM from December. As maintenance at multiple steel mills concludes successively, hot-rolled coil production is expected to gradually rebound in January.

Overall, with steel mills resuming production in January while downstream demand gradually weakens, attention should be paid to the pace of inventory accumulation ahead of the holiday, guarding against the risk of prices falling due to a larger-than-expected inventory increase.

![[SMM Steel] Jindal Steel wins a new iron ore mine in Odisha with ~38 mt reserves](https://imgqn.smm.cn/usercenter/jUyJR20251217171716.jpg)

![Silicon Metal Prices Tested Higher as Market Transactions Remained in Stalemate, While Polysilicon Prices Trended Downward [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)

![[SMM Daily HRC Trading Volume] Futures Continued to Rise, Spot Trading Continued to Recover](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)