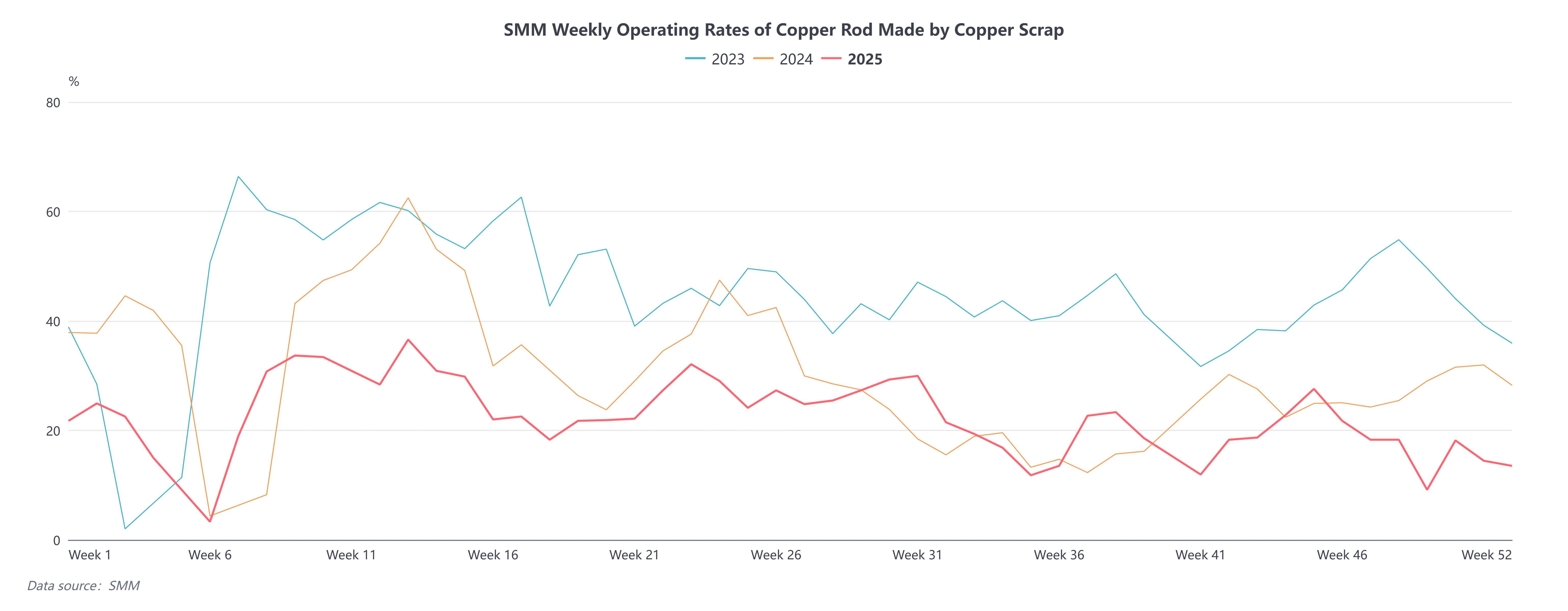

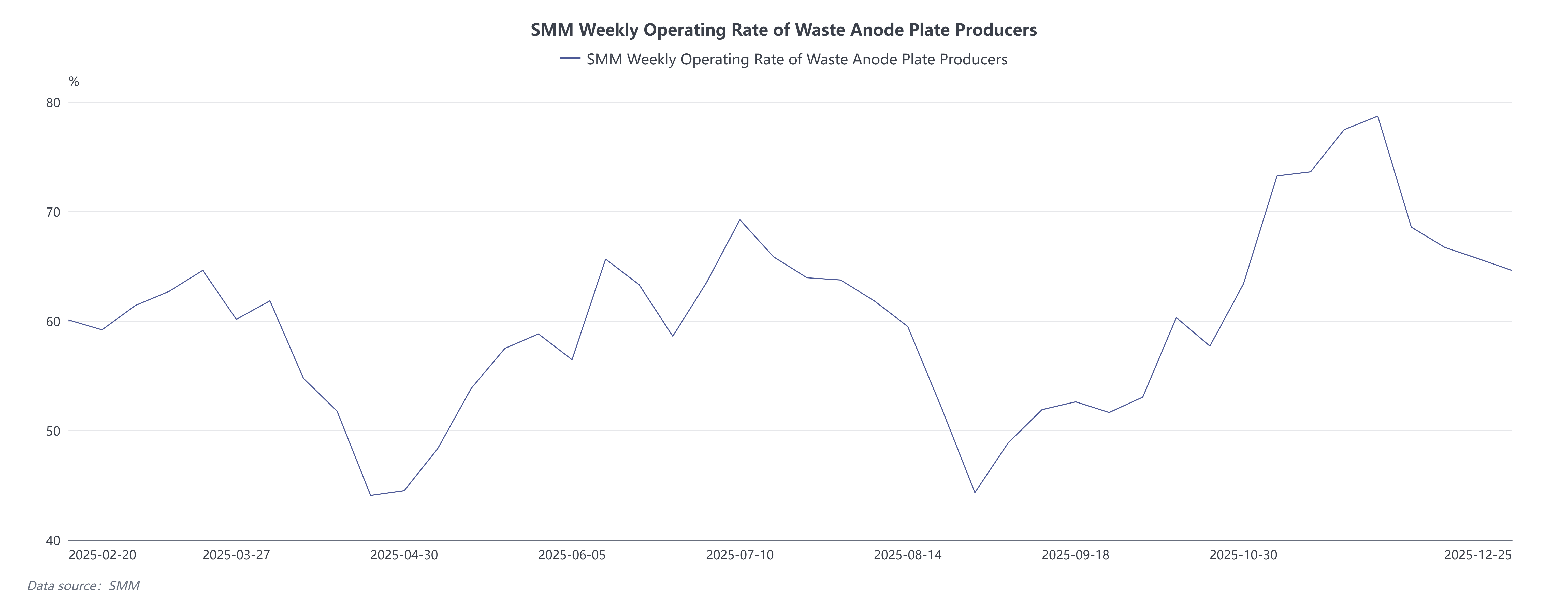

Since mid-to-late September 2025, copper prices have surged strongly and rapidly, repeatedly hitting record highs. As of now, the SHFE copper 2601 contract reached a peak of 99,730 yuan/mt, while the tax-exclusive bare bright copper price climbed to a high of 85,700 yuan/mt. Driven by the rapid rise in copper prices, the tax-inclusive price difference between primary metal and scrap continued to widen, once exceeding 5,000 yuan/mt. Historically, rapid copper price increases have inevitably prompted holders of recycled copper raw materials to increase sales, leading to a widening price difference between primary metal and scrap. This enhances the economic advantage of copper scrap relative to copper cathode, boosts the operating rate of secondary copper rod enterprises, and increases the production of secondary electrolytic copper, thereby raising expectations for higher copper cathode production and restrained consumption. However, the actual situation has significantly diverged from theoretical expectations during the recent copper price rally. According to SMM data, the weekly operating rate of sampled secondary copper rod enterprises in H2 2025 further declined compared to the same periods in 2024 and 2023, even hitting a record low (excluding the impact of the Chinese New Year holiday). This contrasts sharply with the same period in 2024, when rising copper prices drove up operating rates at dismantling enterprises, spurred active sales by suppliers, and fueled strong purchasing sentiment among downstream traders and wire and cable enterprises. Against the backdrop of ample raw material supply, the operating rate of secondary copper rod continued to climb. In 2025, despite copper prices repeatedly reaching new highs, the operating rate of secondary copper rod remained persistently low. Meanwhile, the weekly operating rate for scrap-produced anode plates continued to rise during the copper price increase.

Why has this phenomenon occurred? SMM analyzes several reasons:

1. Supply Side

Raw Material Issues: Copper scrap supply did not increase as usual with rising copper prices. After the National Day holiday, the traditional off-season and suppliers' expectations of a future price pull back led to reluctance in building new inventory, instead prompting active destocking. High copper prices suppressed new scrap generation from processing enterprises, while the pullback in scrap supply in Q4 significantly reduced dismantling volumes at dismantling enterprises, collectively resulting in insufficient circulating supply in the recycled copper raw materials market.

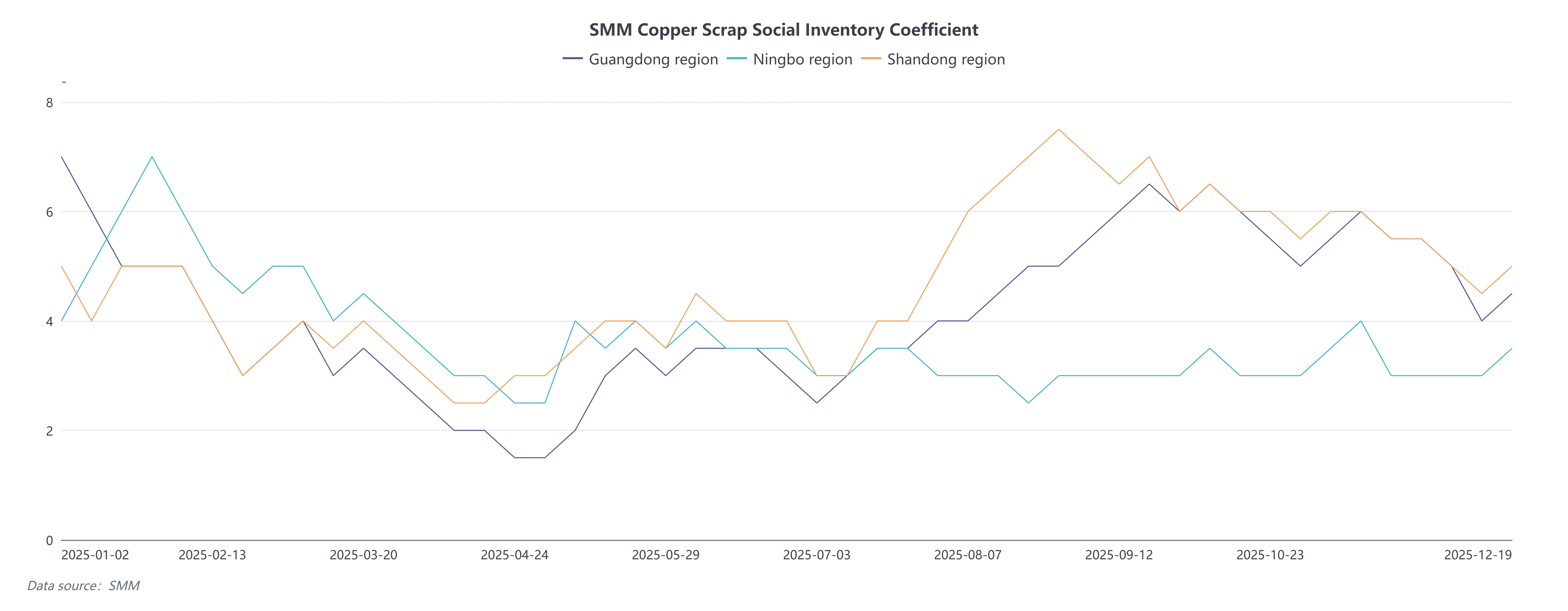

According to the SMM inventory coefficient of recycled copper raw materials in three regions, the inventory coefficient of recycled copper raw materials declined significantly in Q4. Even though copper prices continued to hit new highs, it was still difficult to increase the circulation of recycled copper raw materials. At the same time, when the selling price of anode plates was 500-1,000 yuan/mt higher than that of secondary copper rods, enterprises preferred to produce anode plates from recycled copper raw materials.

2. Demand Side

2. Demand Side

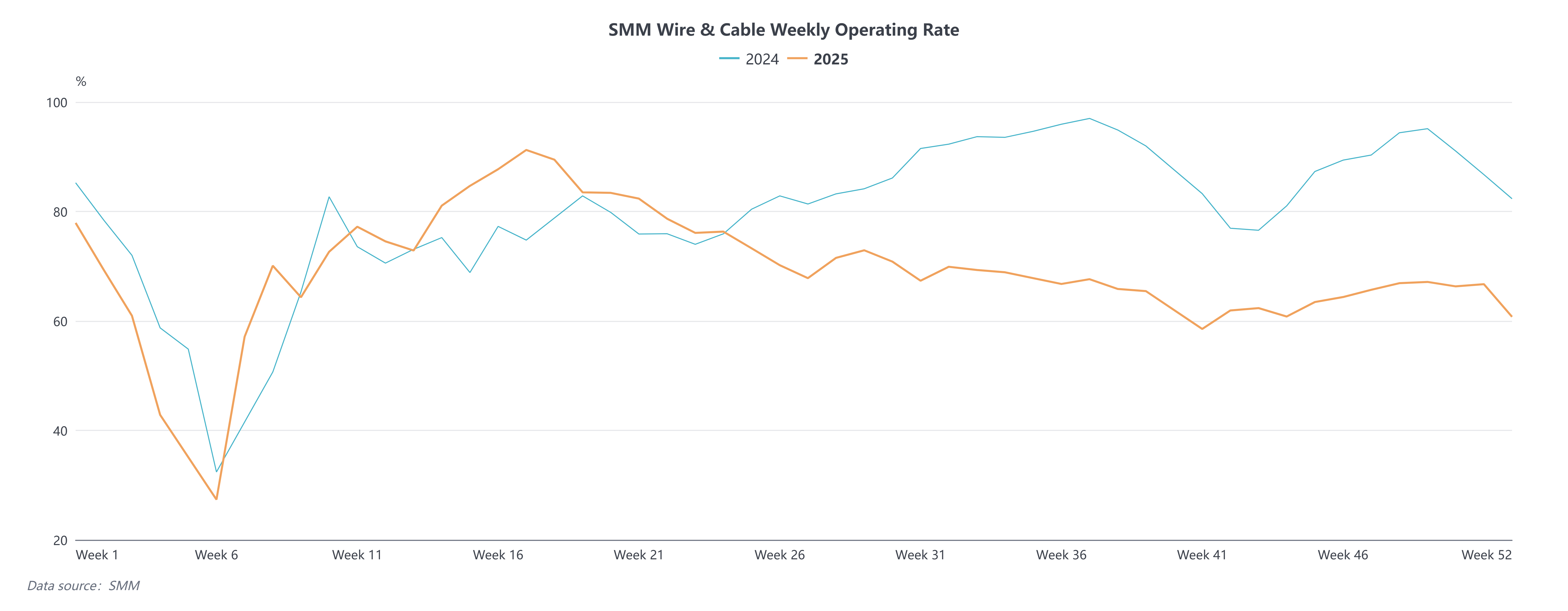

Enterprises generally adopted a "delayed procurement" strategy in the high copper price environment, purchasing only when delivery was imminent, which made it difficult for price increases to effectively boost immediate consumption. According to SMM, the operating rate of sampled wire and cable enterprises in the weekly survey showed a significant decline compared to the same period in previous years, as high copper prices suppressed end-use consumption demand.

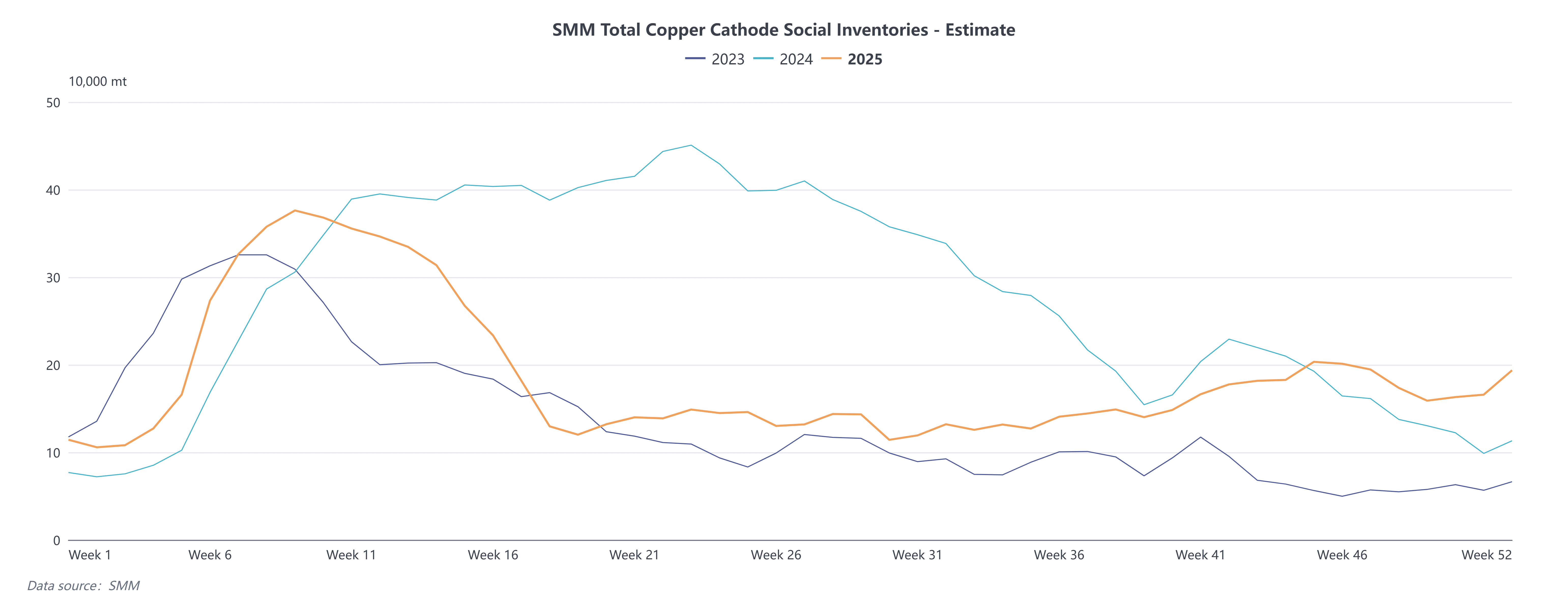

In summary, during this round of soaring copper prices, the supply of secondary copper raw materials fell short of expectations, while end-use demand was affected by fear of high prices, leading to delayed deliveries. The postponement of raw material procurement demand resulted in reduced consumption of both secondary copper raw materials and copper cathode. However, due to long-term contract delivery requirements for anode plates, scrap utilization enterprises maintained normal anode plate production, and more secondary copper raw materials flowed to the smelting sector. Coupled with ample raw materials at smelters and sluggish end-use consumption of copper cathode, copper cathode production remained stable, leading to an increase in spot copper cathode inventory.

Looking ahead, as policy-related issues in the recycling industry remain unresolved, the price difference between primary metal and scrap is expected to remain wide. Policies will continue to impact the decline in secondary copper rod production while boosting anode plate production. The price difference between primary metal and scrap is projected to maintain a range of 3,000–4,000 yuan/mt in the medium and long term.

![Market Risk Appetite Weakened, the Most-Traded BC Copper Contract Closed Down 0.84% [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/grvgR20251217171710.jpg)