Capacity Expansion Meets Demand Gap, Accelerated Domestic Substitution but High-End Breakthrough Under Pressure

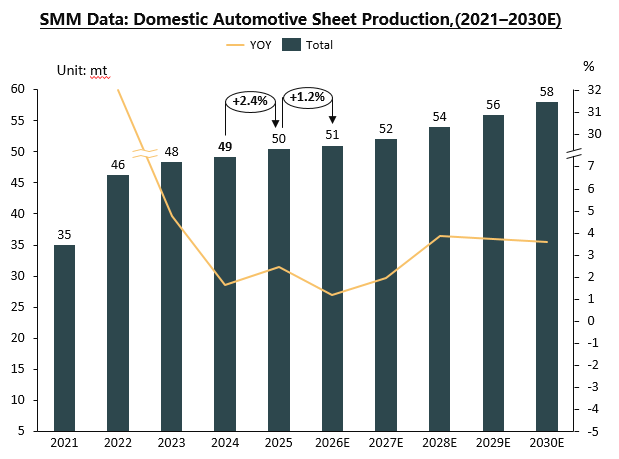

Looking back at 2021-2025, from the supply side, by the end of 2025, there were 8 domestic automotive sheet enterprises with stable production capacity, with a combined annual capacity of about 1 million mt, marking that China has established a large-scale supply system. However, another nearly 400,000 mt of capacity was still under construction or commissioning, indicating that future supply pressure will persist.

In 2025, foreign enterprises' market share was significantly squeezed. In the price-sensitive inner panel market, domestic enterprises, leveraging cost advantages, had successfully achieved large-scale localisation. In the technically more demanding outer panel sector, although leading domestic companies had the capability to supply and to some extent diluted foreign orders, they still lagged behind foreign enterprises in terms of product yield, surface quality stability, and overall production costs. The high-end outer panel market had yet to be fully penetrated.

Moreover, there was a notable gap between the development status of the automotive sheet industry and the terminal automobile production and sales data. Despite the continuous increase in total domestic car production and the rapid rise in NEV penetration rate, the growth in automotive sheet consumption did not completely synchronize. Behind this phenomenon lay a tug-of-war between automakers' strong cost reduction demands and material selection. Some automakers, aiming for sales targets, increased aluminum sheet usage in new models but also substituted steel for aluminum in other components to balance costs, resulting in a moderate rather than explosive growth in overall aluminum sheet demand.

At present, the industry as a whole exhibits characteristics of a "buyer's market," with automakers' cost reduction pressure taking precedence, limiting the bargaining power of material suppliers. Strategies such as jointly holding prices firm, which have been effective in can stock and battery foil sectors, are difficult to implement. At the policy level, while the national "dual carbon" goals are long-term favorable for vehicle lightweighting and aluminum application, in the short term, cost considerations often take precedence over lightweighting demands in enterprise micro-management. Overall, the automotive sheet industry is at a critical stage transitioning from scale expansion to quality improvement, presenting a complex picture of rapid capacity expansion coexisting with structural demand growth and profound adjustments in the competitive landscape, under the joint influence of macro-policy guidance and market demand.

Gear Shift in Growth Rate and Structural Challenges: Restart of Localization and Lightweighting of Outer Panels Shapes a New Cycle

Looking ahead, the automotive sheet industry is expected to enter a mature development phase characterized by a slowdown in growth, structural deepening, and intensified competition. Based on the current capacity layout and demand analysis, domestic automotive sheet production is projected to reach 550,000–600,000 mt annually by 2030, with an average compound annual growth rate remaining in the single digits. The industry maintains a cautiously optimistic outlook on medium and long-term consumption. The main breakthrough in the coming years is anticipated to focus on the comprehensive localization of outer panels. With continuous technological efforts and accumulated production experience by domestic enterprises, by 2027–2030, production efficiency, cost control, and surface quality of high-end outer panels are expected to gradually approach or even reach international advanced levels, achieving further substitution of imported products. Meanwhile, the recent renewed emphasis on "lightweighting" and "high-quality development of the aluminum industry" also signals that material upgrades and application deepening will gain renewed policy and market attention.

Demand-side drivers will become more diverse and uncertain. The sustained growth in NEV production and sales remains the foundation for aluminum sheet demand, but the incremental demand driven by this should be viewed rationally, as the increase in aluminum usage per vehicle is not linear and is significantly constrained by costs. Persistent cost pressure, competition from multi-material routes such as steel-aluminum hybrids, and potential overcapacity risks will test the operational resilience of enterprises. Additionally, changes in the international trade environment and technical requirements introduce variables for export business.

In summary, the Chinese automotive sheet industry from 2025 to 2030 will transition from quantitative expansion to qualitative improvement and structural optimization. For enterprises to secure a favorable position in the future landscape, they must find a precise balance among continuous technological innovation to break through barriers in high-end products like outer panels, extreme cost control to cope with fierce price competition, and flexible market strategies to tap into diverse domestic and overseas demand. At the policy level, if more targeted measures can be introduced to support key technological breakthroughs, guide orderly capacity release, and promote the establishment of a more efficient industrial collaboration system, it will contribute to healthier and more sustainable high-quality development of the industry.

![Aluminum Producers' Operating Rates Rebound to 61.9%; High Prices Challenge "Golden March" Peak Season [SMM Survey]](https://imgqn.smm.cn/usercenter/tXCfs20251217171653.jpg)

![ADC12 Prices Rose Again This Week[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)