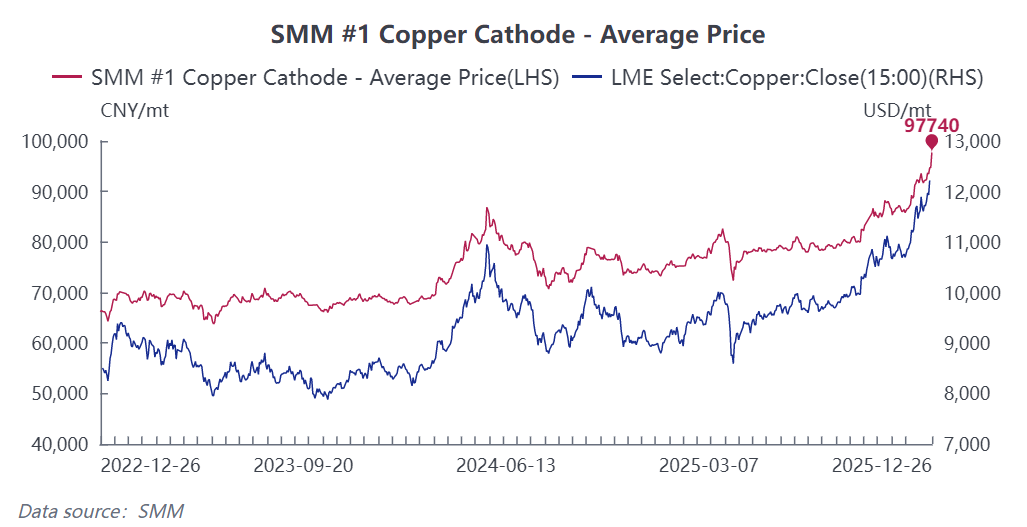

This round of sharp copper price increases resulted from ore supply tightness, the reshaping of global copper cathode trade, the emergence of new demand, and macro-financial resonance. As of December 26, 2025, the SMM spot copper price reached 97,740 yuan/mt, up 33% from the beginning of the year; by the close of that day, the most-traded SHFE copper contract closed at 98,720 yuan/mt, up 34.7% from the start of the year. Downstream semi-finished copper product enterprises generally face challenges such as high costs, pressured processing fees, and shrinking profits. Under pressure from both "continuously rising raw material costs and persistently difficult in raising processing fees," they are struggling to survive. Below are the core reasons for the rise in copper prices and the impact of high copper prices on downstream processing enterprises:

Supply Side: Expanding Ore Supply Deficit and Imbalanced Copper Cathode Inventory Distribution Spark Supply Concerns

1. Frequent disruptions at mines: Incidents such as the accident at Chile's El Teniente mine, the mudslide at Indonesia's Grasberg, and the mine earthquake in the DRC have increased the global mine disruption rate. According to SMM data, the YoY growth rate of global sulfide ore production in 2025 was only 0.13%, significantly lower than the demand growth rate. Additionally, mine grades continue to decline, and the cycle for new mine capacity has extended to 7-8 years. Global copper concentrate supply and demand are expected to remain tight over the next 3-4 years.

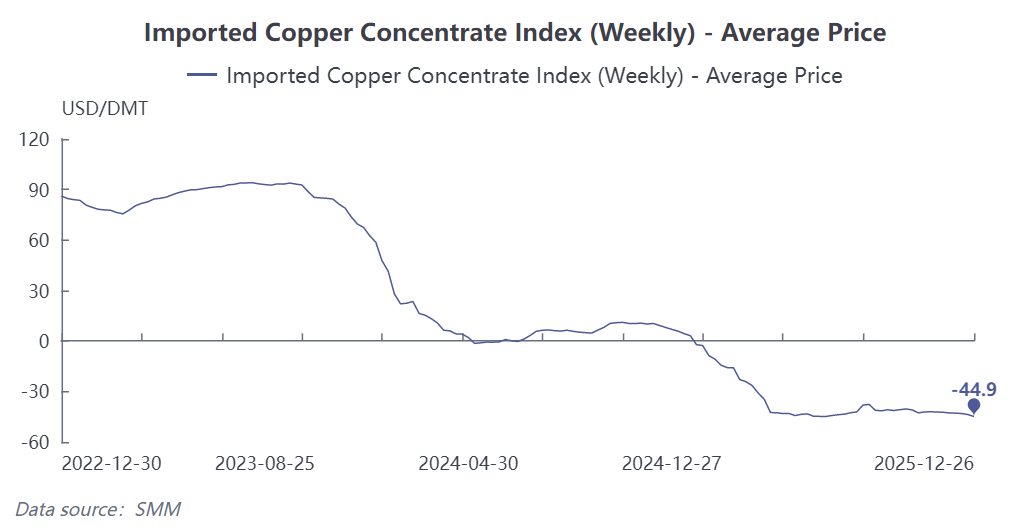

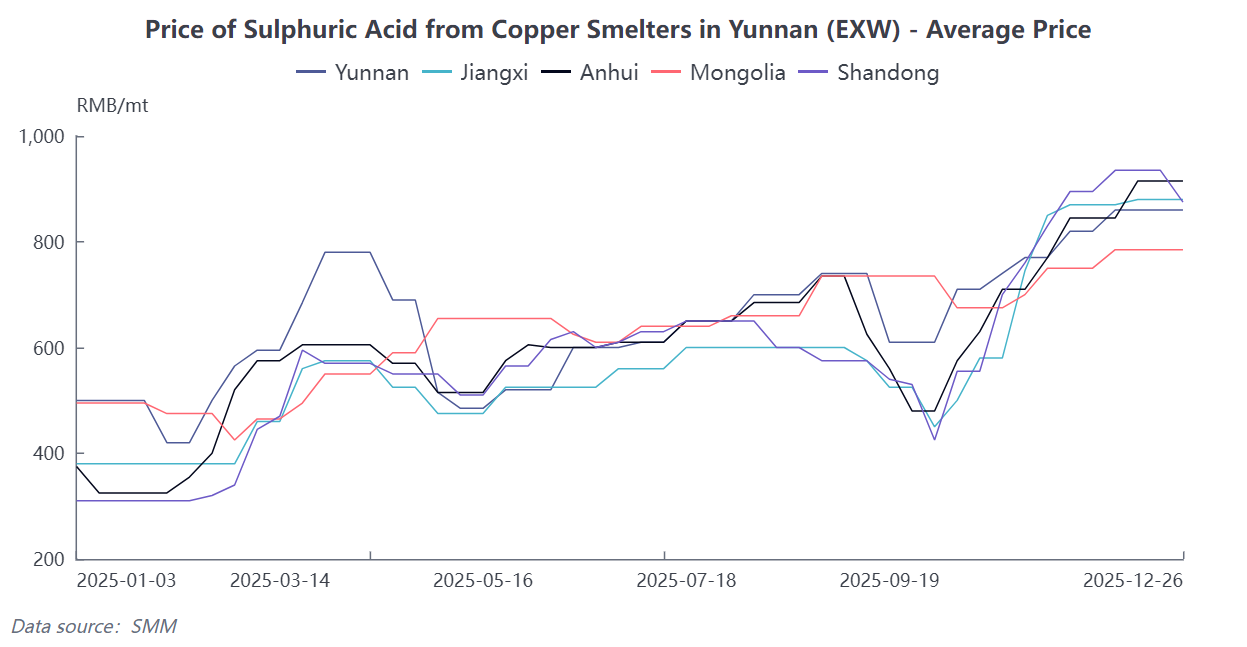

2. Risk of losses in the smelting sector: Copper concentrate TCs have currently fallen to a historical low of -$44.9/dmt, meaning smelters are effectively paying to process ore. However, thanks to high sulphuric acid prices and revenue from by-products such as gold and silver, smelters are either marginally profitable or near break-even. With domestic long-term contracts dropping to $0/mt in 2026 and potential pullbacks in sulphuric acid prices, some smelters may see reduced production, limiting the flexibility of copper cathode supply.

2. Risk of losses in the smelting sector: Copper concentrate TCs have currently fallen to a historical low of -$44.9/dmt, meaning smelters are effectively paying to process ore. However, thanks to high sulphuric acid prices and revenue from by-products such as gold and silver, smelters are either marginally profitable or near break-even. With domestic long-term contracts dropping to $0/mt in 2026 and potential pullbacks in sulphuric acid prices, some smelters may see reduced production, limiting the flexibility of copper cathode supply.

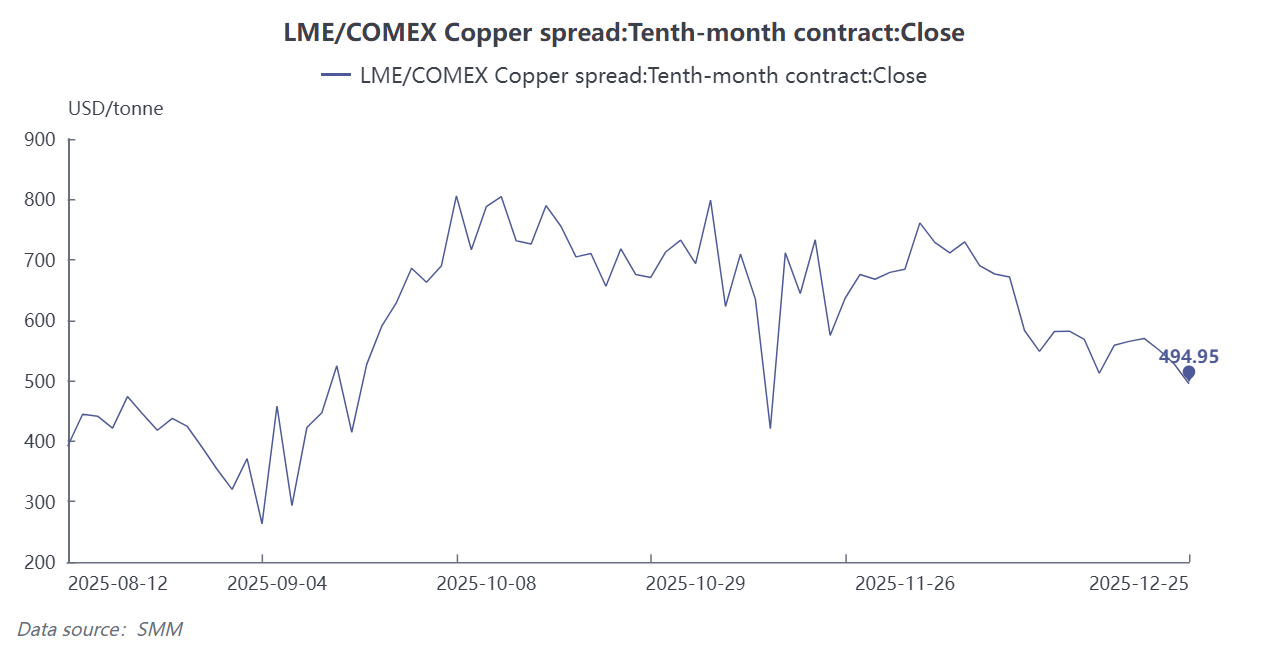

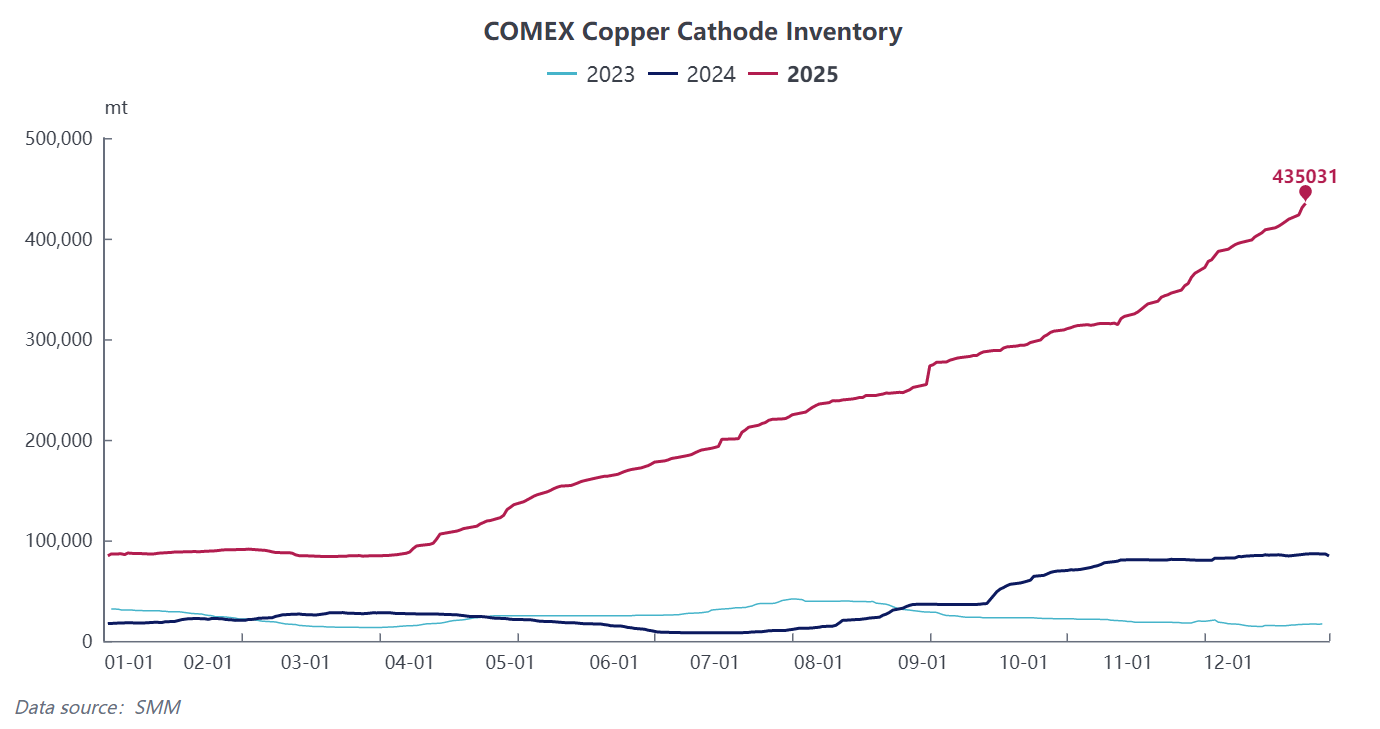

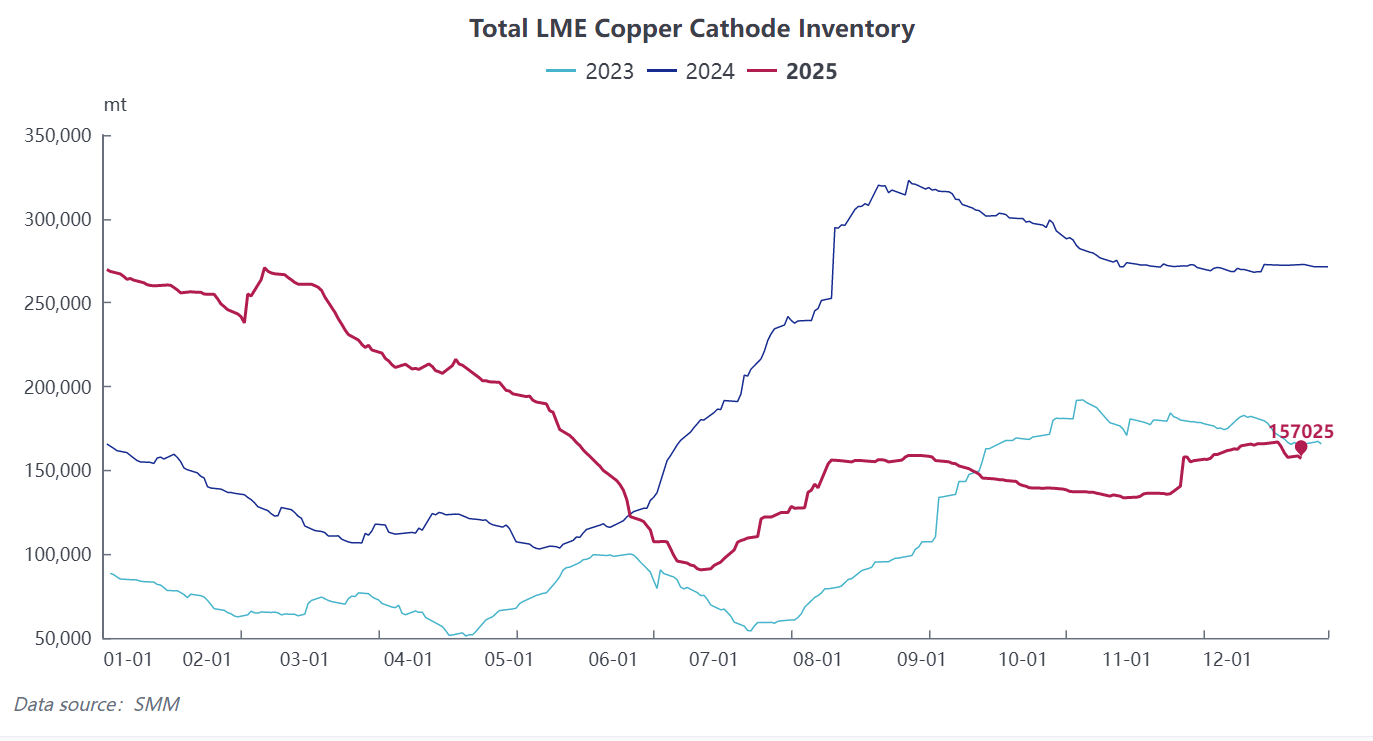

3. Imbalanced inventory distribution: Under the expectation of US tariffs, the COMEX-LME spread remains above $500/mt, leading to a continued concentration of copper cathode in the COMEX market. As of December 24, COMEX inventories rose to a record high of 475,400 short tons, while LME warehouse inventories in Asia gradually declined, exacerbating regional supply tightness and squeeze risks.

3. Imbalanced inventory distribution: Under the expectation of US tariffs, the COMEX-LME spread remains above $500/mt, leading to a continued concentration of copper cathode in the COMEX market. As of December 24, COMEX inventories rose to a record high of 475,400 short tons, while LME warehouse inventories in Asia gradually declined, exacerbating regional supply tightness and squeeze risks.

4. Scrap copper demand growth outpaces supply growth: With copper concentrate TCs at low levels, smelters continue to increase their demand for recycled copper raw materials. Downstream processing enterprises face low-carbon requirements, which will also drive up the utilization rate of copper scrap. This keeps supply and demand for recycled copper raw materials tight, but the impact on the balance of the copper element is limited.

Demand Side: Strong Expectations for New Copper Demand in Emerging Sectors, but Bubble Risks Warrant Attention

Copper demand driven by the energy transition and the AI computing boom is expected to offset the decline from weak demand in the traditional real estate sector, keeping copper consumption growth positive. However, attention should be paid to the actual return on investment in the AI industry, as most AI projects are not yet profitable, and there is a risk of structural decline in the marginal returns on capital expenditure.

Macro Perspective: Monetary Easing Expectations Amplify Financial Premiums

In 2025, amid monetary easing policies in the US, the US dollar index fell by over 9%. Expectations for US Fed interest rate cuts have not yet cooled, highlighting copper’s anti-inflation and financial attributes. Driven by both fundamentals and macro factors, capital inflows have pushed prices higher. Additionally, against the backdrop of a weaker US dollar, ample liquidity, geopolitical risks, and de-dollarization, soaring precious metal prices have also contributed to the rise in copper prices.

"Mines Reap Huge Profits, While Downstream Processors Struggle for Scraps"

Mines, leveraging resource monopolies, capture the majority of price increase benefits, while downstream processing enterprises face multiple pressures—squeezed costs, capital tie-ups, compressed RC/TC, and intense competition—continuously eroding profit margins.

Amid soaring copper prices, semi-finished copper product enterprises are caught in a dilemma: rising raw material costs and difficulty in raising processing fees. This severely impacts their operations, profitability, and even their market competitiveness and long-term strategic direction. Below are the latest developments in the semi-finished copper products industry:

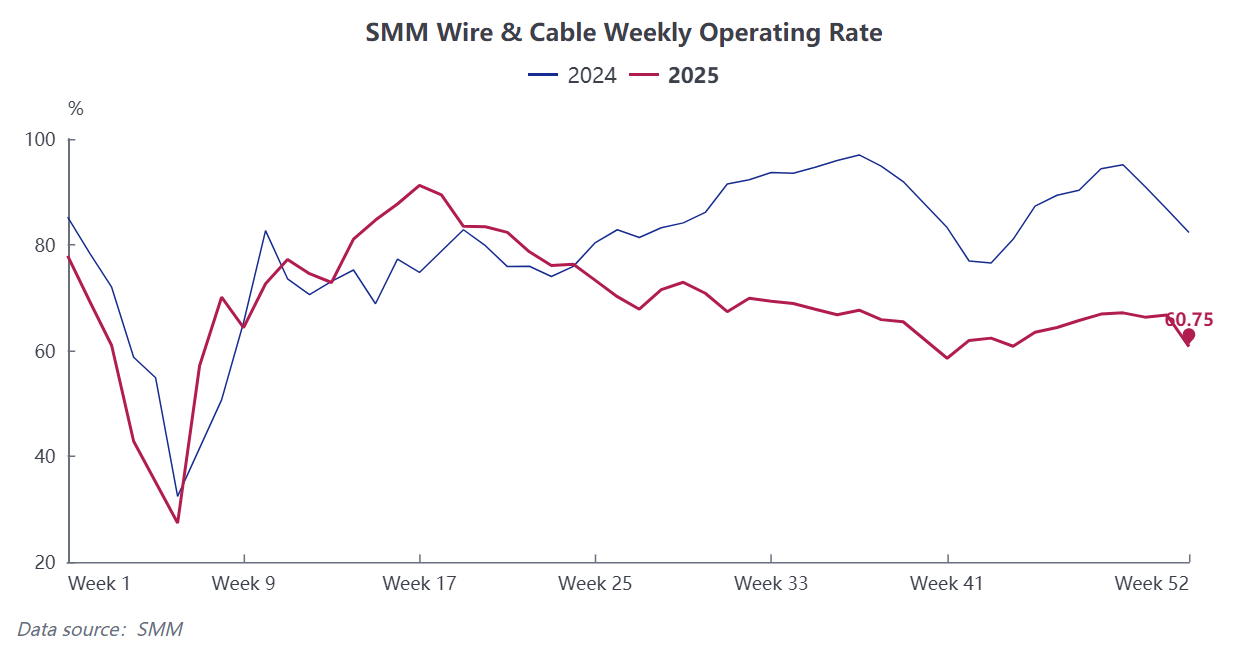

The wire and cable industry faced severe losses at the current copper prices, significantly increasing operational pressure. Most enterprises began production cuts, resulting in an overall bleak performance, with the majority indicating that production workshops would suspend operations during the 2026 New Year holiday. According to SMM data, the weekly operating rate for SMM copper wire and cable enterprises (December 19–25) was 60.75%, down 5.96 percentage points WoW and 21.57 percentage points YoY.

The wire and cable industry faced severe losses at the current copper prices, significantly increasing operational pressure. Most enterprises began production cuts, resulting in an overall bleak performance, with the majority indicating that production workshops would suspend operations during the 2026 New Year holiday. According to SMM data, the weekly operating rate for SMM copper wire and cable enterprises (December 19–25) was 60.75%, down 5.96 percentage points WoW and 21.57 percentage points YoY.

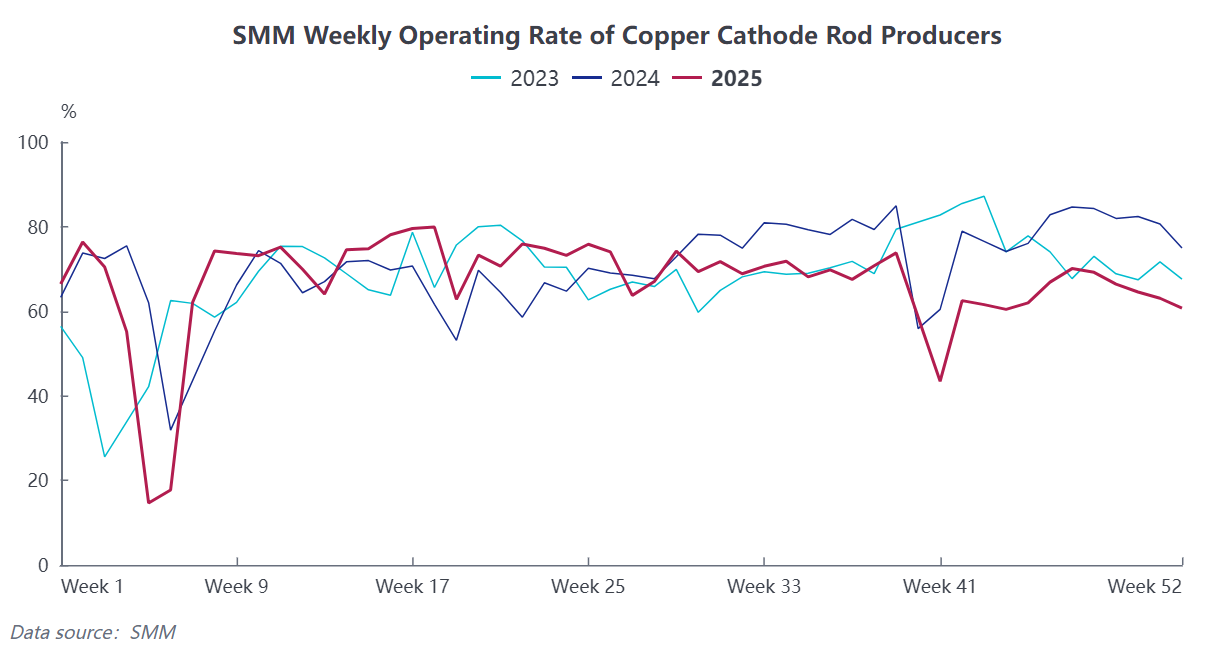

Copper Rod Industry: With copper prices remaining high, new orders have declined and finished product inventories are high, leading multiple enterprises to continue reducing or halting production. According to SMM data, the operating rate of major domestic copper cathode rod enterprises (December 19-25) was 60.73%, down 2.34 percentage points WoW and 14.19 percentage points YoY. The surge in copper prices has led to a sharp increase in capital occupation for processing enterprises, causing liquidity strain. The imbalance in cost transmission has also resulted in a collapse of gross margins, accelerating industry reshuffle and phasing out outdated capacity.

Processing enterprises can use the SMM #1 copper cathode spot price as an anchor, combined with "back-to-back" purchase and sales price locking, which is one of the core operations to lock in processing fees and reduce the risk of copper price fluctuations. "Unified price benchmark + matching performance terms + closed-loop risk management" will support the long-term development of enterprises.