According to SMM, on the evening of December 19, 2025, Antofagasta and smelters under the China CSPT group finalized the 2026 copper concentrate long-term contract TC/RC at USD 0/mt and 0 cents/lb, marking a historical low. By comparison, the 2025 copper concentrate benchmark TC/RC was set at USD 21.25/mt and 2.125 cents/lb.

Compared with the end of 2024, during this year’s CESCO week, Chinese smelters accelerated the pricing rhythm for 2026 domestic copper cathode long-term contracts. It is reported that first-round offers for major copper cathode brands circulating in East China are mostly above RMB 180/mt. This article provides a brief summary of current long-term contract quotations across different regions.

Overall, spot premiums in 2025 have improved notably compared with 2024. However, in East China, uneven brand liquidity, wide inter-brand price spreads, and the scarcity of imported COMEX-registered brands have resulted in a highly fragmented fixed-price long-term contract market. Coupled with copper prices repeatedly hitting record highs, most downstream consumers remain pessimistic about signing 2026 copper cathode long-term contracts. Although expectations have risen from late-2024 levels and there is some anticipation of potential supply tightness in 2026, high copper prices and elevated premiums continue to deter downstream buyers, and the proportion of fixed-price long-term contracts is expected to decline further.

Based on SMM’s active market discussions this week, first-round fixed long-term contract offers in Eastern China are mainly quoted at RMB 200–260/mt on exw Shanghai warehouse basis, while ex-work plant prices from large smelters in East and Central China are quoted at RMB 180–200/mt. Adjustments may be made depending on delivery terms, pricing mechanisms, transportation distance, and contracted volumes.

In South China, exw warehouse prices are quoted at around RMB 260/mt, compared with approximately RMB 120/mt in 2025.

In Southwest China, first-round ddp offers are around RMB 160/mt, versus RMB 110/mt in 2025.

In northern regions, quotations vary significantly. Offers in North China have yet to commence, while Henan and Shandong are heard at around RMB 60–70/mt, and Northwest China at approximately RMB 140–160/mt on ex-work basis

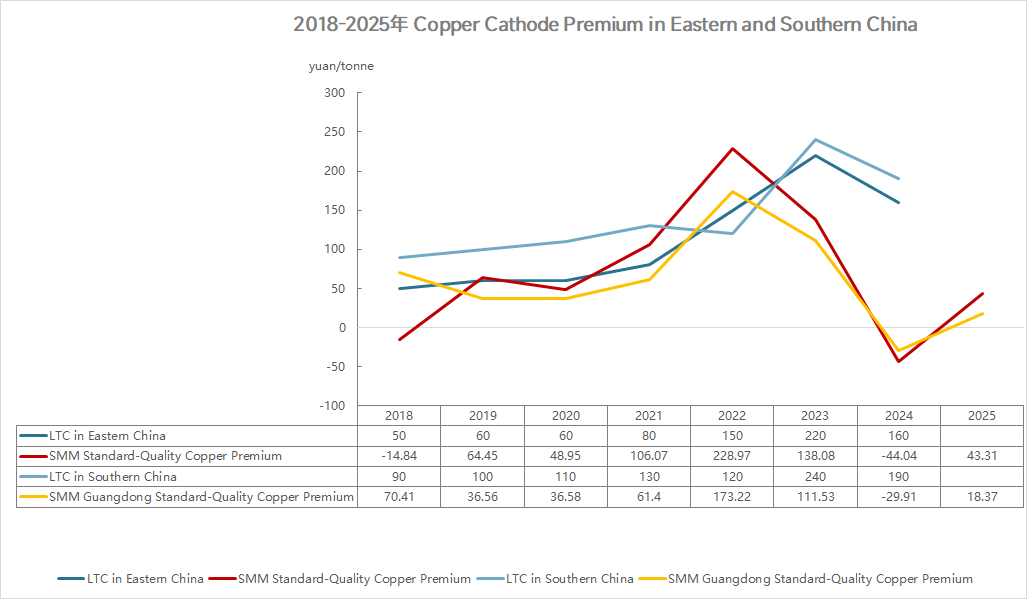

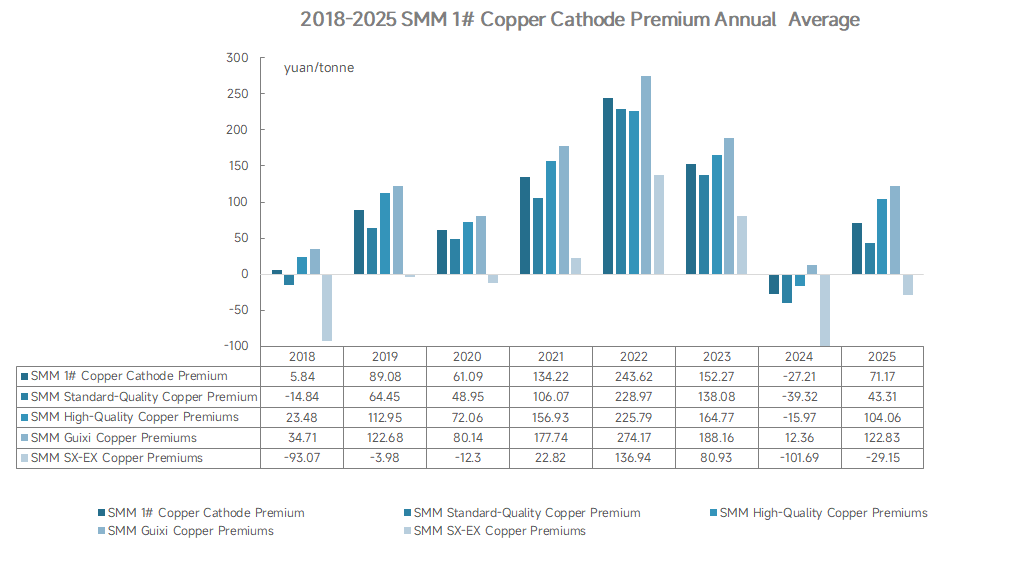

Note: 2025 average prices are calculated up to December 26, 2025.

Following the completion of the first-round quotations, producers are expected to actively negotiate with downstream buyers. SMM will continue to monitor market developments closely.