I. Copper Price Trends and Motor Cost Structure

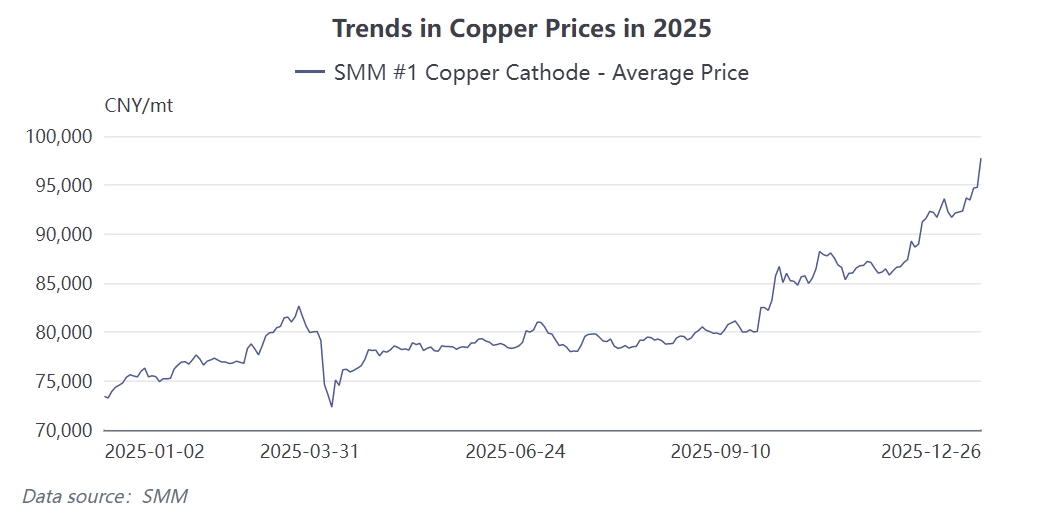

Recent copper prices have shown a sustained upward trend, becoming a direct source of pressure for motor producers. According to market data, the SMM #1 copper cathode price has reached 97,740 yuan/mt, with a single-day increase of 3.14%. This rapid short-term rise has directly impacted the raw material cost structure of motor production. Copper is widely used in motors—from NEV traction motors to small and medium-sized industrial motors, all rely on copper semis. As a downstream product of copper, enamelled wire derives over 95% of its cost from copper semis. This means that any fluctuation in copper prices is almost entirely passed on to the cost of enamelled wire, thereby affecting the total cost of the motor.

The amount of copper used varies significantly across different types of motors. Taking NEVs as an example, the copper usage per traction motor is approximately 15–20 kg, while the total copper usage per vehicle reaches 60–80 kg. Although the unit consumption for micro motors is relatively small, their vast quantity still results in a considerable total copper demand.

II. Motor Producers' Response Strategies

Facing cost pressure, motor producers have adopted differentiated market strategies. The price adjustment range for standard motor products is relatively uniform, generally between 10% and 20%. These products are highly standardized with high price transparency, making cost transfer relatively straightforward. For customized motors, however, producers adopt more cautious pricing strategies. Customized motors are typically designed according to customer drawings, and there is often closer collaboration between the producer and the customer, sometimes even establishing joint ventures to deepen ties. Under this cooperation model, motor enterprises are more inclined to maintain stable customer relationships by sacrificing some design profits. Some companies have also adopted a "same-day quotation" strategy to respond more flexibly to fluctuations in raw material prices. Although this real-time quotation model increases transaction complexity, it better reflects current cost conditions and avoids losses caused by price lag.

III. Differences in the Impact of Copper Price Volatility Compared to Other Raw Materials

Compared to the rise in rare earth prices, the transmission mechanism of copper price increases is more direct and intense. The impact of rising rare earth prices can, to some extent, be shared and buffered by magnetic material manufacturers, whereas the transmission of copper price hikes is more volatile and harder to predict. Copper price fluctuations are influenced by multiple factors, including macroeconomic policies, fundamentals, futures markets, future expectations, and even changes in the international financial landscape. This multi-factor-driven nature makes predicting copper prices exceptionally difficult, leading to greater uncertainty for motor enterprises. In contrast, although rare earth permanent magnets are also a significant component of motor costs, accounting for 30%–45% of raw material expenses, their price volatility can be partially cushioned through long-term cooperation with magnetic material manufacturers and technical adjustments. For instance, cost pressures can be alleviated by optimizing magnet design or adopting alternative materials.

IV. Industry Chain Collaboration and Future Development Paths

Motor enterprises are situated in the midstream of the industry chain. On one hand, they face an end-use market that continuously pushes for lower prices and an unfavorable international economic environment. On the other hand, they must cope with persistently rising copper prices and the persistently high costs of rare earth permanent magnets. This dual pressure makes motor enterprises the "sandwich biscuits" of the industry chain, urgently needing to break through the predicament through technological innovation and supply chain optimization. Material innovation is an important way to address cost pressure. For example, the popularization of hairpin motor technology has achieved cost optimization by increasing the slot fill ratio. Reducing material usage without compromising performance, or finding more economical alternative materials, has become a widely focused direction in the industry. Supply chain collaboration is also crucial. Motor manufacturers, magnetic material suppliers, and copper semis suppliers need to establish closer cooperative relationships to jointly address cost fluctuations. Some enterprises enhance supply chain resilience and reduce market volatility risks through vertical integration or long-term strategic partnerships. At the same time, establishing flexible pricing mechanisms is also an important means to balance the interests of all parties. For instance, some motor manufacturers adopt price linkage clauses, allowing product prices to partially reflect changes in raw material costs, thereby achieving risk sharing.

In the future, motor enterprises will place greater emphasis on diversifying their supply chain layouts, offsetting some cost pressures through technological upgrades and process optimization. Innovative solutions such as flat-wire motors and magnetic material reduction technologies will be accelerated for widespread adoption. Meanwhile, vertical integration and long-term strategic partnerships will become key choices for enterprises to stabilize their supply chains. In response to price fluctuations, establishing flexible pricing mechanisms and inventory management models will also become core competencies for enterprises. Ultimately, those enterprises that can strike a balance between cost control and technological innovation will gain a first-mover advantage in this industry transformation.

![Market Risk Appetite Weakened, the Most-Traded BC Copper Contract Closed Down 0.84% [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/grvgR20251217171710.jpg)