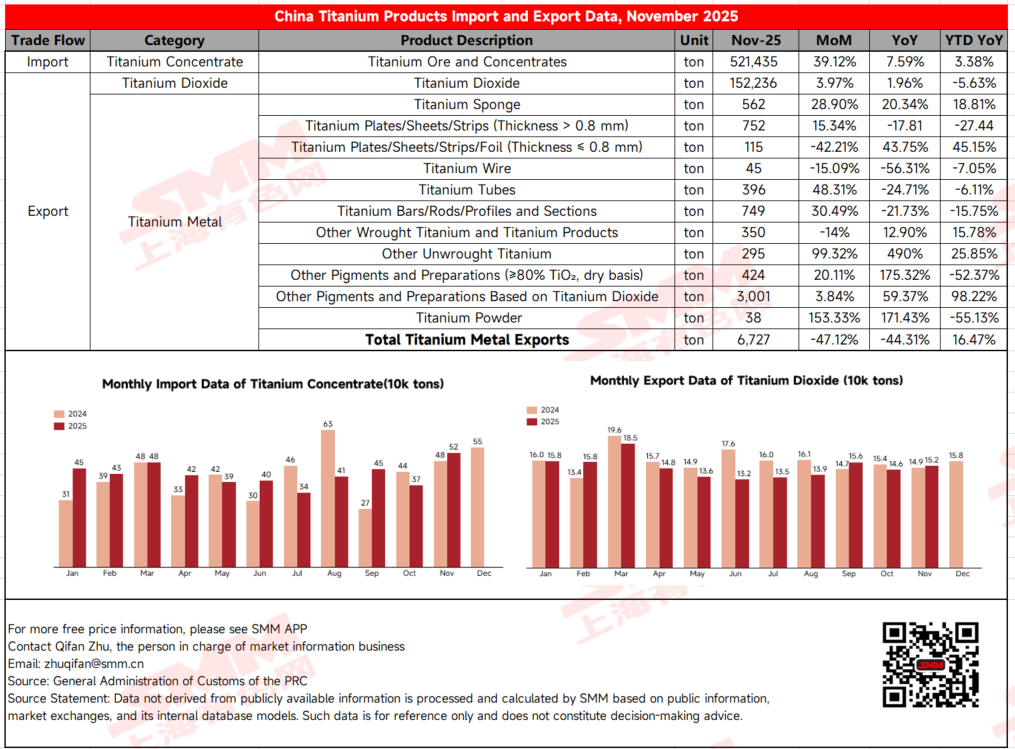

In November 2025, China's titanium concentrate imports reached 521,400 tons, up 39.12% month-on-month and 7.59% year-on-year. Regarding exports, titanium dioxide exports for the month were 152,200 tons, a month-on-month increase of 3.97% and a year-on-year rise of 1.96%. Meanwhile, total exports of titanium metal products amounted to 6,727 tons, a sharp month-on-month decline of 47.12% and a year-on-year decrease of 44.31%. Overall, the imported ore market and titanium dioxide foreign trade showed active performance with a significant recovery trend. However, titanium material exports weakened noticeably, and overall orders in the fourth quarter were generally subdued.

Titanium Concentrate: Import Volume Increases, Prices Remain Stable; Downstream Demand Continues to Pressure the Market

The titanium concentrate market has shown a downward trend overall since November, with imported ore prices remaining weak and stable. Among them, the ex-factory price for Mozambique titanium concentrate (TiO₂≥46%) was reported at 1,700–1,800 yuan/ton, while the ex-factory price for Nigerian titanium concentrate (TiO₂≥50%) was reported at 1,850–1,900 yuan/ton.

Import ore volume increased significantly by 39.12% month-on-month this month, reaching 541,400 tons, indicating a notable increase in supply. At the same time, imported ore prices have gradually approached the level of domestic ore, prompting downstream enterprises to consider switching to imported ore for stockpiling. Furthermore, due to the significant increase in sulfuric acid costs in sulfuric acid process titanium dioxide production, titanium dioxide companies are also inclined to push down procurement prices for titanium ore, further pressuring the market. From the demand side, the operating rate of the titanium dioxide industry remained high this month, with demand growing steadily in sync.

Looking ahead to next year, the imported titanium ore market is expected to remain stable and achieve slight growth, gradually becoming a strong competitor to domestic ore. As downstream industries continue to expand production, demand for imported titanium ore is expected to increase further.

Titanium Dioxide: Export Volume and Prices Rise Together; Strong Overseas Demand Fails to Mask Structural Profit Pressure

In November 2025, titanium dioxide exports amounted to 152,200 tons, an increase of 3.97% month-on-month and 1.96% year-on-year. Cumulative exports from January to November decreased by 5.63% year-on-year. The significant improvement in exports in November was mainly supported by Christmas stocking demand in the foreign trade market, with good order performance. Additionally, orders signed in October were concentrated for delivery in November, driving the overall shipment volume up. Exports in December are expected to remain high. On one hand, Indian agent orders have increased significantly since mid-December after India lifted its anti-dumping duties on Chinese products. On the other hand, most orders are being delivered before Christmas, coupled with some new foreign trade orders driven by the coatings exhibition at the end of November.

Despite strong export demand, market competition pressure continues to intensify: Sulfuric acid process titanium dioxide continues to suffer losses due to cost inversion. As the mainstream process, Chinese brands compete to lower prices in the international market, putting significant pressure on transaction prices. Chloride process products in the export market mainly compete with mid-to-high-end European and American brands, but the international market generally positions them as mid-to-low-end, leaving limited room for price increases. Furthermore, since October, with capacity release and lower chlorine costs, the price gap between chloride process and sulfuric acid process products has further narrowed, forming a competitive landscape where both are on par. Therefore, even though the export market overall recovered in the fourth quarter, the industry still faces significant profit and competitive pressure.

Titanium Metal: Exports Under Significant Pressure in the Second Half of the Year; Policies and Overseas Competition Lead to Weak Demand

In November 2025, the total export volume of titanium metal raw material products was 6,727 tons, a month-on-month decrease of 47.12% and a year-on-year decline of 44.31%. Cumulative exports from January to November increased by 16.47% year-on-year. Among them, sponge titanium exports were 562 tons, a month-on-month increase of 28.9%.

The titanium metal market performed weakly overall in the second half of the year, mainly affected by export control policies, which structurally suppressed export volume. At the same time, overseas market competition intensified, with ongoing supply from regions such as Kazakhstan and Japan consistently pressuring domestic exports, leaving Chinese products in a relatively weak position in the international market share. Demand in the civilian sector was also relatively sluggish, with no significant new demand highlights emerging in the industry.

Looking back at the first half of the year, the market was mainly supported by demand from the aerospace sector, coupled with opportunities such as international conferences driving concentrated order releases, which contributed to an overall recovery trend in exports. However, after entering the second half of the year, the export market failed to sustain its growth momentum, maintaining a weak pattern overall.

![[SMM Analysis]Global Tungsten Stays Hot Over Chinese New Year: Europe Tight, India Scrap Gains](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)

![[SMM Analysis] Logistics Slowdown Causes Disruption in Goods Flow, Stainless Steel Social Inventory Rises Temporarily](https://imgqn.smm.cn/usercenter/tjmLW20251217171722.jpeg)