In 2025, the global chromium market witnessed adjustments in its supply and demand dynamics. Overseas ferrochrome production saw widespread cuts and suspensions, which gradually led to a surplus of chromite ore—the raw material. Meanwhile, China's core position in the global ferrochrome industry was further consolidated.

Output in the stainless steel market, the key downstream sector, maintained an overall steady growth, but its demand for chromium exhibited significant periodic fluctuations. This drove the ferrochrome market to present an "M-shaped" operating pattern characterized by sharp rises and falls.

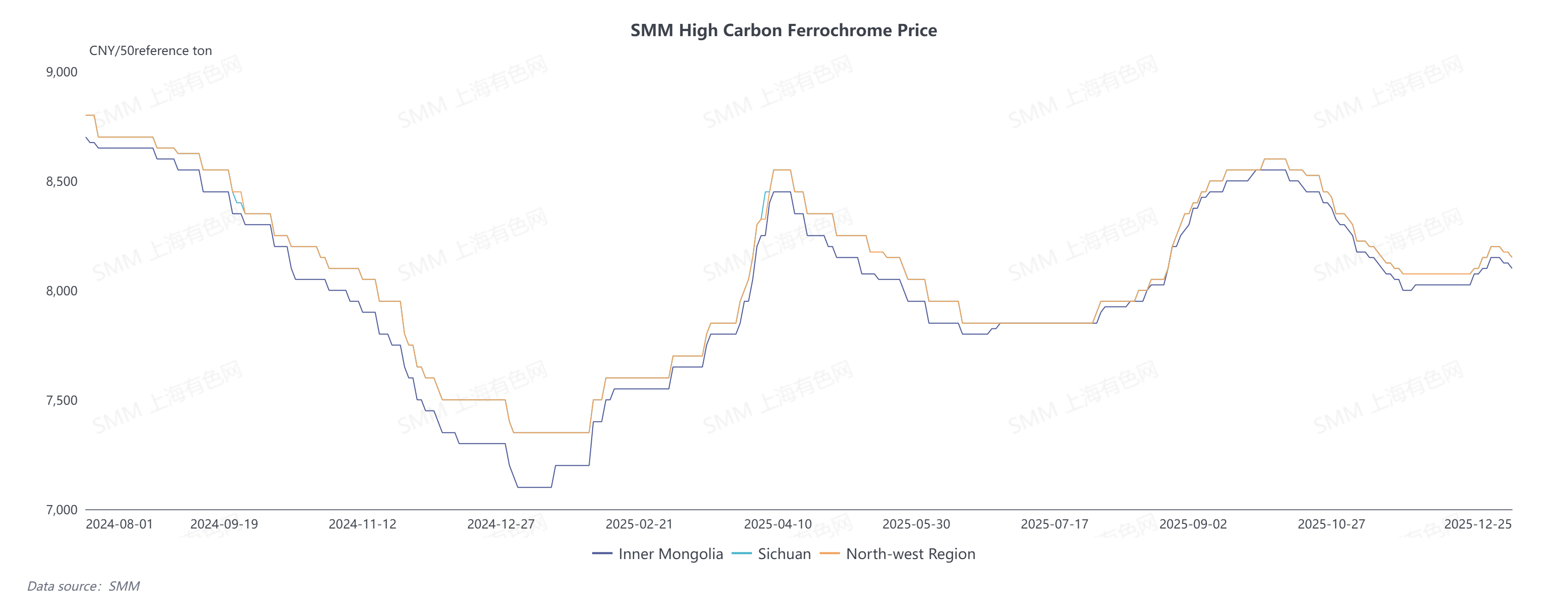

I. Review of High-Carbon Ferrochrome Price Trends

Affected by adjustments in the fundamental supply-demand relationship, the price of high-carbon ferrochrome in China fluctuated sharply in 2025, hitting a peak of 8,600 yuan per 50 basis tons and a trough of 7,100 yuan per 50 basis tons, with a price difference of over 1,500 yuan.

In 2024, severe oversupply suppressed the ferrochrome price at the low level of 7,100 yuan for nearly three months. Later, the market entered the "Golden March and Silver April" consumption peak season: a sharp increase in downstream stainless steel production schedules boosted chromium demand, yet negative cost margins dampened manufacturers’ production enthusiasm. Against the backdrop of tight supply, the ferrochrome price rebounded rapidly to 8,500 yuan per 50 basis tons.

Starting from June 2025, major chromium enterprises overseas, especially in South Africa, announced the suspension of ferrochrome smelting operations, making the reduction of imported ferrochrome the main theme of the chromium market in the second half of the year. To ensure the stability of raw material supply, the steel tender price stabilized in the range of 8,300–8,500 yuan per 50 basis tons.

However, in October, domestic ferrochrome manufacturers ramped up production actively as profits were secured, leading to a steady growth in output, which effectively offset the supply gap caused by reduced imports. Meanwhile, downstream stainless steel sector was mired in weak demand and cautious purchasing amid the off-season, pushing the retail ferrochrome price into a downward trajectory and falling back to 8,000 yuan per 50 basis tons.

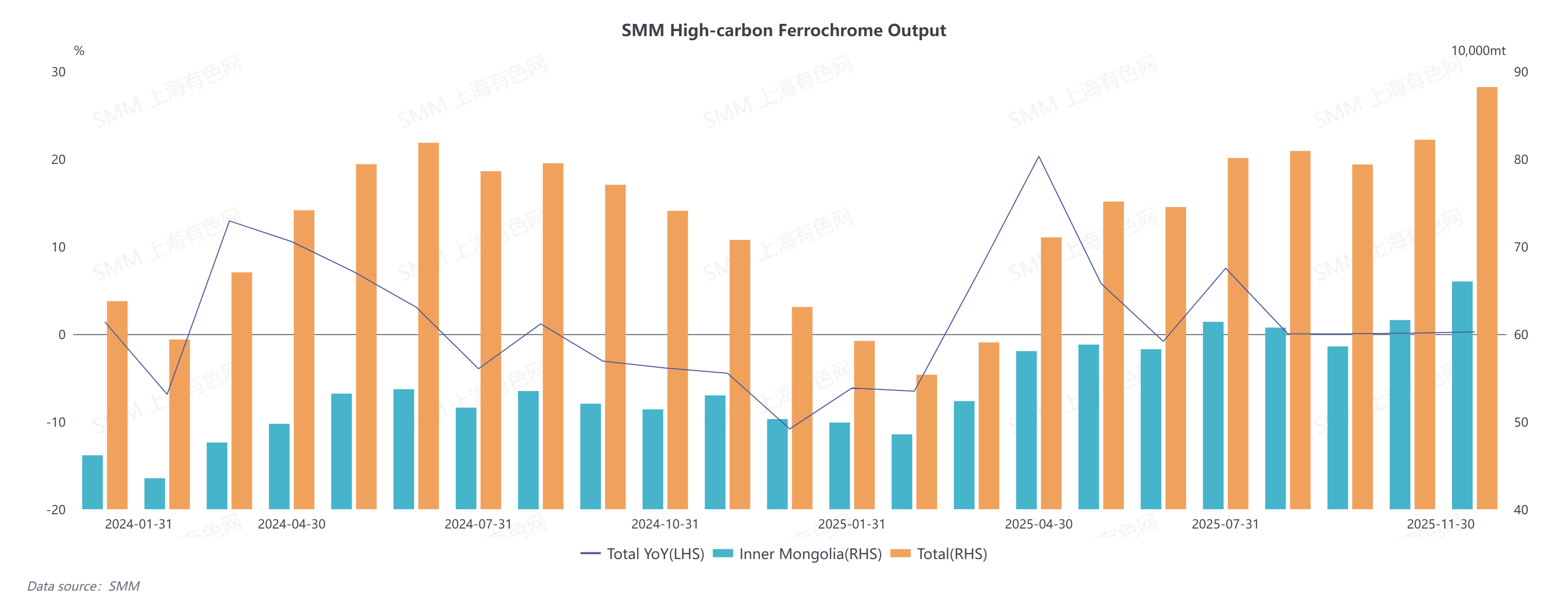

II. Review of Ferrochrome Supply Dynamics

In 2025, China’s high-carbon ferrochrome output demonstrated a stepwise growth trend, with an overall year-on-year increase of approximately 2.76%, and exceeded the historical peak to approach 900,000 tons in November.

In the first half of 2025, combined effects of negative cost margins and the market conditions of 2024 dampened the production enthusiasm of ferrochrome manufacturers, keeping the output at a low level. Entering the second half of the year, the production cuts and suspensions of overseas ferrochrome curbed the total volume of imported ferrochrome. Meanwhile, the downstream stainless steel output remained high, providing solid support for domestic ferrochrome demand. Favorable steel tender prices expanded the profit margins of ferrochrome manufacturers, driving a steady growth in output.

At the same time, unique geographical advantages propelled Inner Mongolia’s output share to rise from 70% to 78%, making it the primary driver of production growth. The low electricity tariff averaging 0.41 yuan/kWh effectively reduced the power consumption of ferrochrome production in Inner Mongolia, and the development of new technologies such as source-grid-load-storage integration will further amplify this advantage. In addition, its proximity to Tianjin Port—the major distribution hub for chromite ore—has significantly lowered the logistics costs in Inner Mongolia, with the average freight rate standing at around 80 yuan/ton. Furthermore, Inner Mongolia has designated the ferroalloy industry as a pillar sector and provided policy support, fueling the steady development of the local ferrochrome industry.

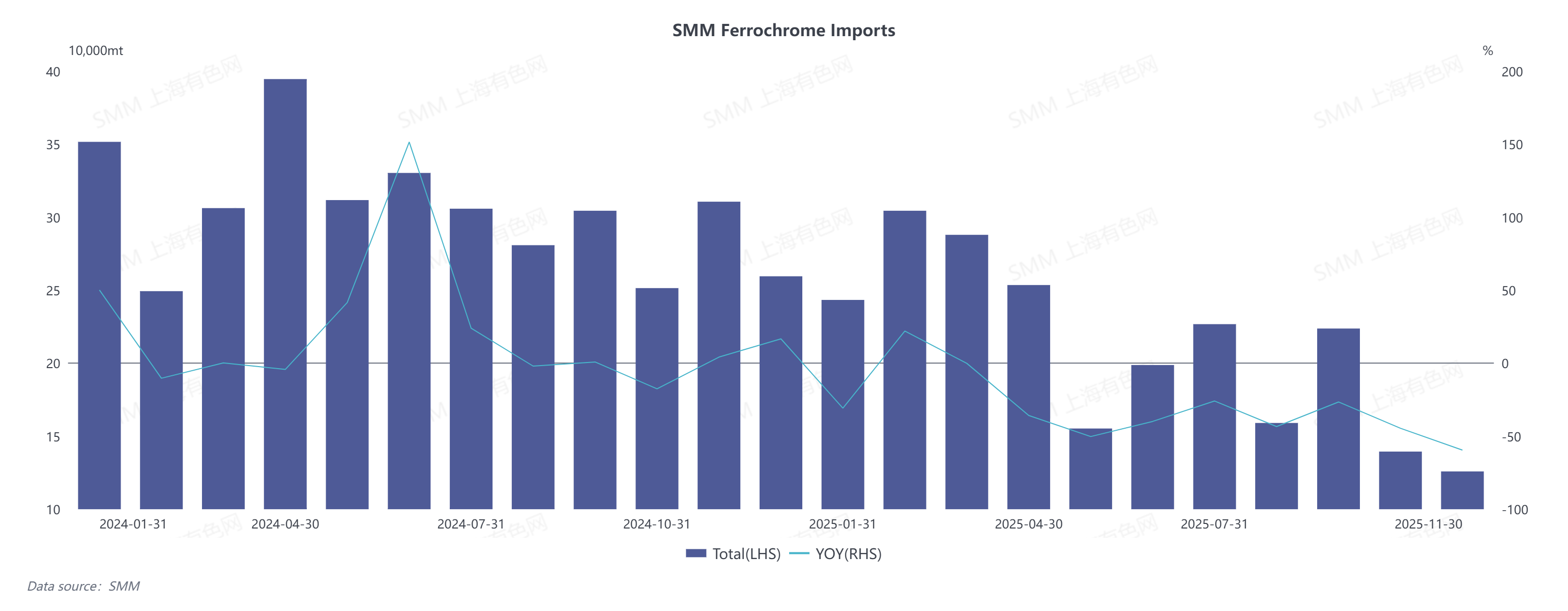

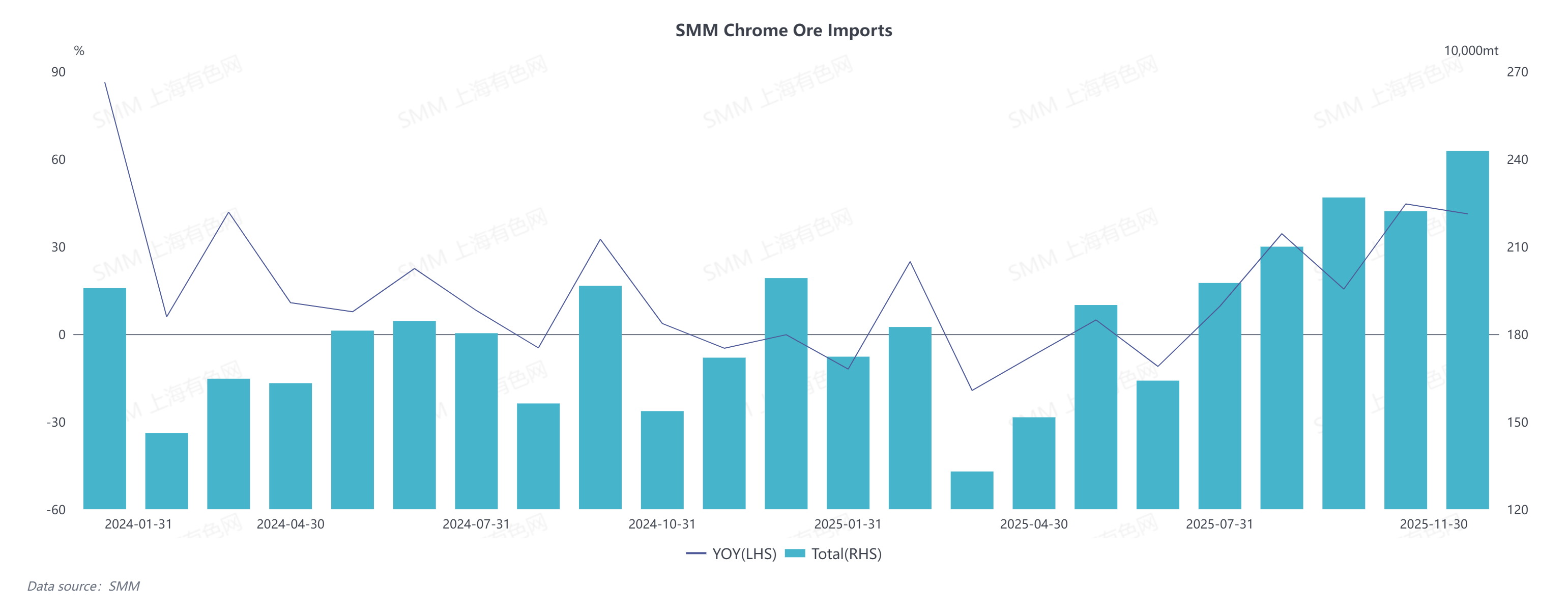

On the import front, constrained by inherent power supply issues and the competitive pressure from the expansion of China’s ferrochrome production capacity, major South African chromium enterprises including Glencore and Samancor announced the phased suspension of their ferrochrome smelting operations starting from May 2025. This directly resulted in a substantial decline in China’s ferrochrome imports.

In the January–November period of 2025, the total import volume of high-carbon ferrochrome reached 2.3187 million tons, a year-on-year decrease of 31.76%. Specifically, imports of high-carbon ferrochrome from South Africa accumulated to 955,100 tons, down 43.13% year on year; while imports from Kazakhstan totaled 941,900 tons, registering an 18.36% year-on-year decline.

III. Review of Ferrochrome Demand-Side Dynamics

In 2025, the stainless steel market—the core downstream sector of ferrochrome—saw steady output growth, with its demand for chromium rising by 5.39% year on year and exhibiting distinct periodic fluctuations.

The market started off at a low level in Q1 due to the Spring Festival holiday, but production schedules surged during the "Golden March" consumption peak. Volatile raw material supply drove up stainless steel prices, and improved profit margins boosted steelmakers’ production enthusiasm. In Q2, however, stainless steel futures and spot prices slumped sharply amid disruptions from U.S. tariff policies. Coupled with the arrival of the traditional off-season, steel mills faced the risk of losses, leading to a slowdown in output growth and weaker demand for chromium.

The market gradually entered the "Golden September" peak season in Q3, when steel mill output rebounded and inventory-building activities picked up, pushing up procurement demand for ferrochrome. In Q4, the "Silver October" period underperformed; hampered by sluggish end-user demand in the year-end off-season, stainless steel prices declined, and news of production cuts by steel mills emerged frequently, resulting in diminished support for ferrochrome demand.

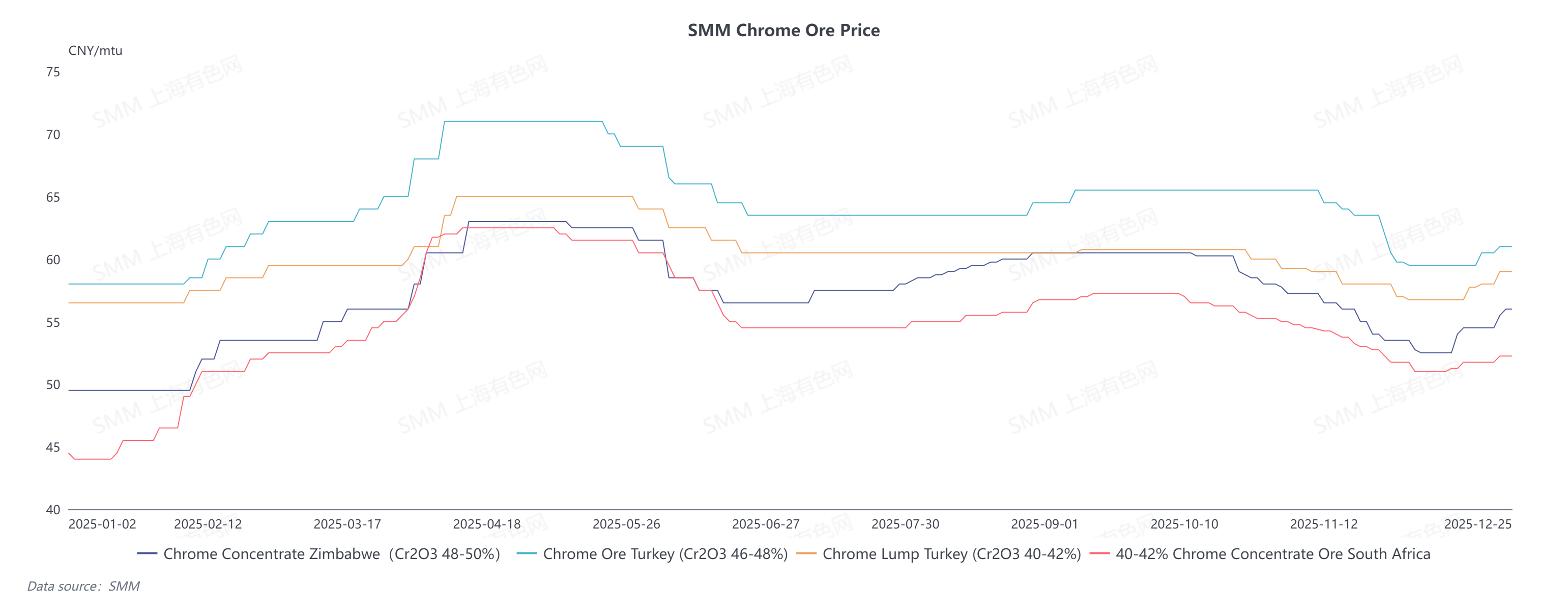

IV. Review of Chromite Ore Price Trends

On the raw material front, chromite ore prices in 2025 followed a trend of sharp rise and gradual decline in the first half of the year, and gradual stabilization in the second half.Starting from March, chromite ore futures took the lead in bottoming out and rebounding. Coupled with the concentrated release of buying interest after the Spring Festival, prices surged by approximately 50 US dollars in a short period, and spot prices followed the upward movement accordingly. Later, during the May–July consumption off-season, the underperformance of the stainless steel market and bearish expectations drove a preliminary drop in futures prices. Meanwhile, weakening ferrochrome prices dampened demand for chromite ore, leaving traders struggling to offload inventories and dragging spot prices lower.

In the second half of the year, production cuts and suspensions of ferrochrome in South Africa directly boosted chromite ore export volumes, which in turn led to repeated record highs in China’s chromite ore imports. The oversupply issue capped the upside potential of prices. According to SMM data, China’s current chromite ore port inventory is approaching 4 million tons, significantly increasing the pressure on traders to sell cargoes. Combined with the slight pullback in ferrochrome output and the lack of demand support for ore, chromite ore prices still face downside risks.

On the import front, China's total chromite ore imports reached 20.922 million tons in the January–November period of 2025, a year-on-year increase of 10.46%. Specifically, imports from South Africa accumulated to 17.3298 million tons, up 12.58% year on year; imports from Turkey totaled 734,100 tons, down 25.46% year on year; and imports from Zimbabwe hit 1.6497 million tons, registering a year-on-year surge of 46.29%.

In terms of import structure, South African chromite ore still dominated, accounting for nearly 83% of total imports. Benefiting from increased mining output in Zimbabwe, its import volume rose, with its proportion climbing to 8%. In contrast, Turkish chromite ore saw its import share narrow to 3.4% due to transportation restrictions caused by geopolitical factors and other elements.

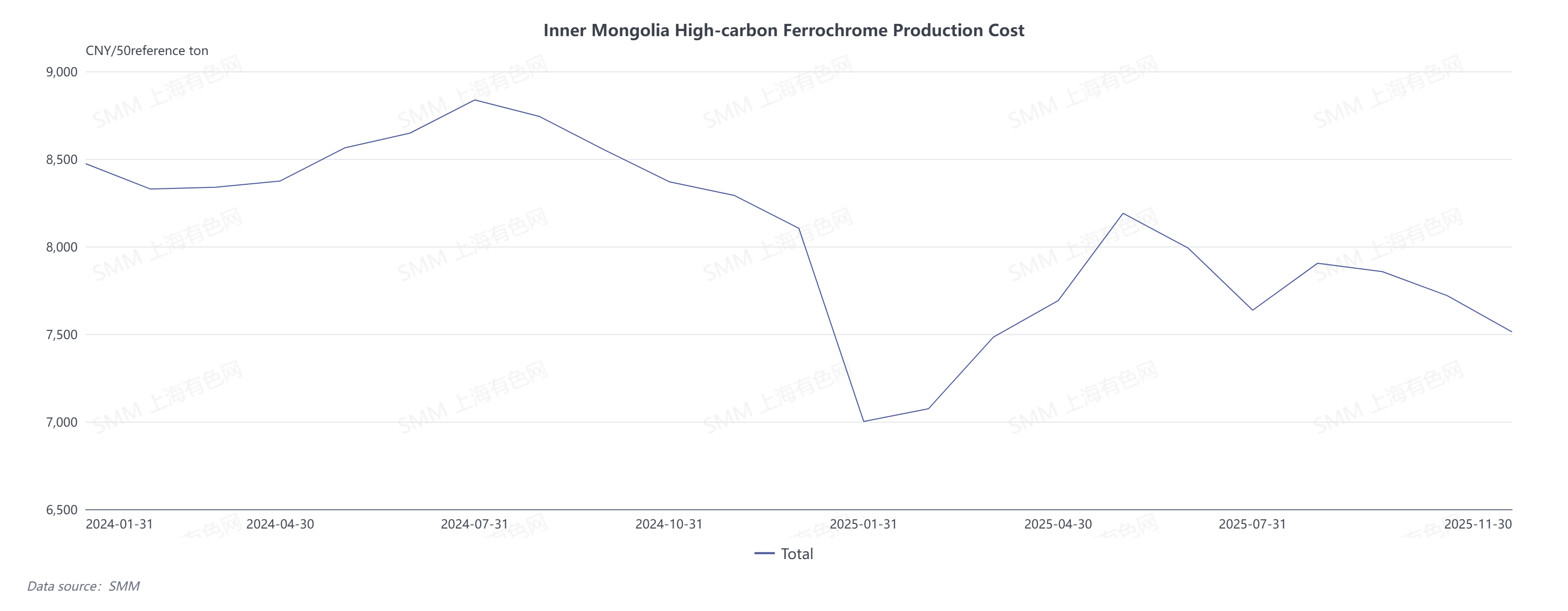

V. Review of Ferrochrome Cost Variations

In 2025, the production cost of high-carbon ferrochrome in China exhibited distinct characteristics of initial rise followed by stabilization and regional differentiation, with a notable correlation to price fluctuations of chromite ore—the primary raw material—and a fluctuation range of 100 yuan per 50 basis tons.

From a regional perspective, Inner Mongolia leveraged its multi-dimensional advantages in policies, geography, and transportation to keep ferrochrome production costs low, allowing local manufacturers to maintain a certain profit margin for most of the year. In contrast, southern regions such as Sichuan managed to control production costs from June to October by taking advantage of preferential electricity tariffs during the wet season.

In terms of different periods:

- From January to April, the rebound of chromite ore prices after a decline drove up the spot smelting cost of ferrochrome.

- From May to June, the concentrated arrival of chromite ore shipments at ports triggered a price correction. Combined with successive reductions in coke prices, the production cost of ferrochrome moved downward.

- From July to September, the market gradually entered the consumption peak season. Optimistic expectations pushed chromite ore prices higher; meanwhile, navigation restrictions at Tianjin Port led to increased freight costs, and consecutive hikes in coke prices further drove up ferrochrome production costs.

- From October to December, year-end consumption off-season dampened market expectations. Severe oversupply of chromite ore led to price declines, dragging down raw material costs accordingly. However, most southern regions entered the dry season, and the upward adjustment of electricity tariffs resulted in a moderate increase in ferrochrome production costs.

VI. Supply-Demand Balance Analysis of the Chromium Market

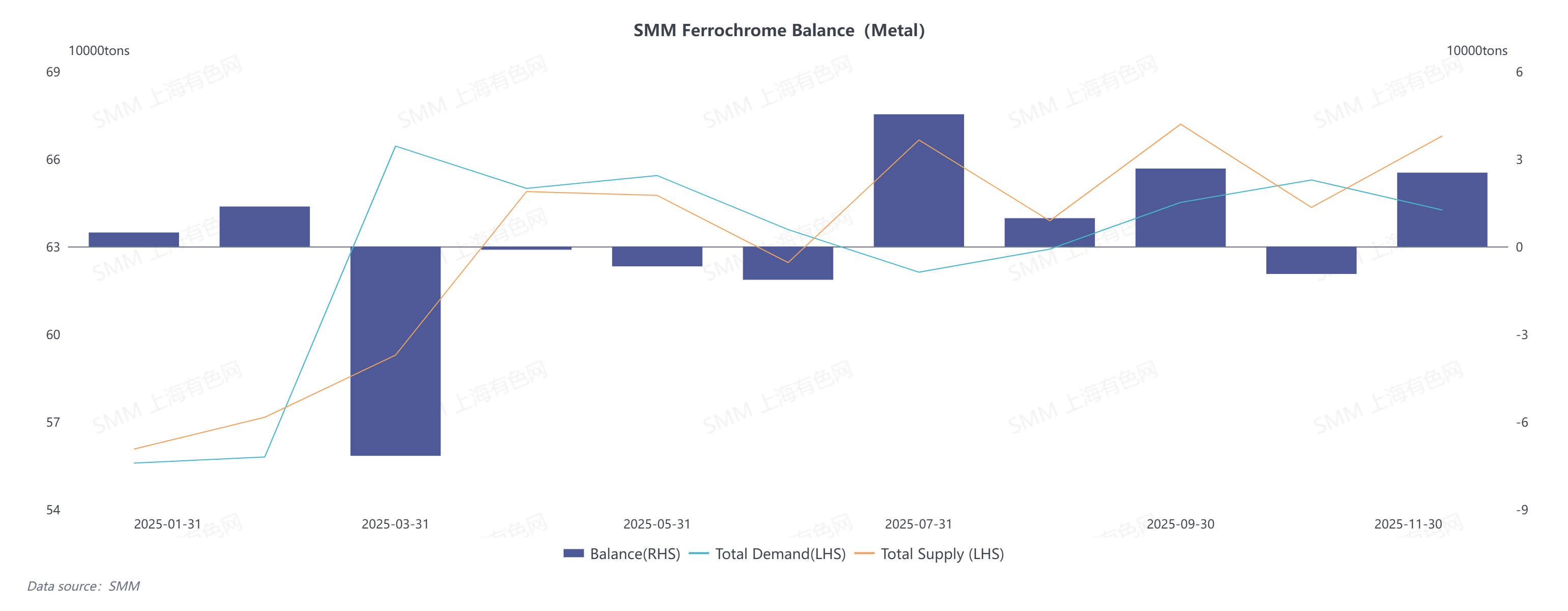

(I) Supply-Demand Balance of Ferrochrome in China

Against the backdrop of booming supply and demand, China’s ferrochrome market maintained an overall tight balance in 2025. Supply was notably tight in the first half of the year; after the supply gap was filled in the second half, the market tilted toward looseness, with an expected slight surplus of 47,700 metal tons.

From January to June, lingering overhang from the severe oversupply in 2024 and negative cost margins dampened the production enthusiasm of ferrochrome manufacturers, keeping output at a low level and resulting in insufficient supply. On the demand side, stainless steel mills completed maintenance and significantly ramped up production schedules, driving up procurement demand for ferrochrome raw materials. The prominent supply shortage pushed ferrochrome prices upward.

From July to December, reduced imports of ferrochrome vacated part of the domestic supply market. With stainless steel output remaining at a relatively high level, domestic ferrochrome demand received strong support. Ferrochrome manufacturers ramped up production actively, with output climbing steadily and multiple new production capacities coming online. In November, ferrochrome output hit a record high, easing market supply and resolving the shortage issue, thus maintaining a tight balance operation.

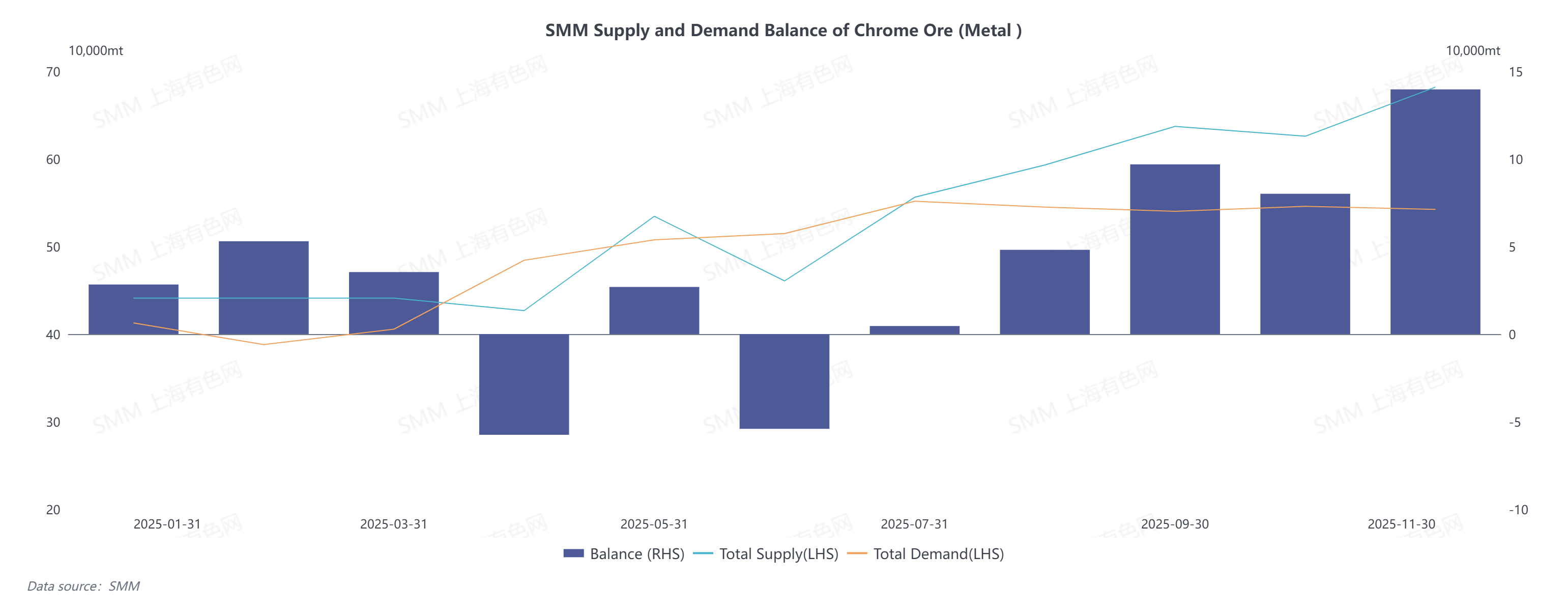

(II) Supply-Demand Balance of Chromite Ore in China

In 2025, the problem of chromite ore oversupply became increasingly pronounced, keeping the ore prices under pressure.

In the first half of the year, the oversupply of chromite ore was mainly attributed to the sluggish output of ferrochrome on the demand side. On one hand, the lingering impact of ferrochrome oversupply in 2024 dragged its prices down to a historical low in recent years, which dampened the production enthusiasm of ferrochrome manufacturers, resulting in limited overall output and consequently weak demand for chromite ore. On the other hand, after chromite ore prices rebounded from an excessively low level, overseas mines grew more willing to ship cargoes, with the global chromite ore shipment volume stabilizing at 2.3 million tons and supply increasing accordingly.

In the second half of the year, the oversupply of chromite ore was primarily driven by continuously rising imports that repeatedly hit record highs. The suspension of ferrochrome operations in South Africa led to the diversion of surplus chromite ore to the export market, directly pushing up China’s chromite ore imports by 25% year on year. On the demand side, domestic ferrochrome manufacturers expanded production actively boosted by attractive profit margins, generating a demand of approximately 2.19 million metal tons for chromite ore—a year-on-year increase of 5.7% that remained relatively modest. As a result, the oversupply trend of chromite ore persisted.

(III) Global Ferrochrome Supply-Demand Balance

In 2025, the global ferrochrome market saw a distinct state of supply shortage. On the supply side, the global center of ferrochrome production accelerated its eastward shift, and China’s position as the world’s largest ferrochrome producer became increasingly prominent, with its share of global output rising to 43%. However, affected by high power costs, South Africa basically suspended its ferrochrome smelting operations throughout the year, leading to a sharp contraction in output and a notable supply gap.

On the demand side, the stainless steel markets in China and Indonesia remained in a phase of active expansion, with output maintaining steady growth, thus providing rigid demand support for ferrochrome raw materials. Nevertheless, attention should be paid to two potential factors: first, the possible slowdown in the expansion rate of the stainless steel market in the future, amid the decline in demand from traditional industries and the ongoing development of emerging sectors; second, the increasing proportion of recycled raw materials used due to the accumulation of scrap metal in the early stage. These factors have dragged down the growth rate of direct demand for ferrochrome from 4.9% to 2.1%.

From the perspective of the chromite ore sector, short-term oversupply of global chromite ore is inevitable, but driven by the continuous growth of new production capacity, the chromite ore market is expected to gradually return to a balanced state. On one hand, current chromite ore prices are at a relatively high historical level, with substantial mining profits, thus sustaining a high annual output of 400 million tons. However, there are no significant new mines under development globally, and supply growth mainly relies on the expanded output of traditional mines in South Africa, Kazakhstan, India and other countries, meaning the supply growth rate will slow down in the subsequent period. On the demand side, ferrochrome production capacity in China, Zimbabwe, Indonesia and other countries is growing steadily, and South Africa is also promoting the recovery of its ferrochrome industry by actively addressing power supply challenges. This underpins a sound growth outlook for chromite ore demand, and the oversupply issue will be gradually alleviated.

![Silicon Metal Price Center Remained in the Doldrums [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/CrEsY20251217171716.jpg)

![Silicone Product Prices Rebounded and Rose, While Overall Market Transactions Remained Sluggish [SMM Silicone Weekly Review]](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)