I. Macro Environment Analysis in 2025

The global nickel market operated in a complex and volatile macro environment in 2025. The implementation of US tariff policies significantly disrupted global trade flows, while a slowdown in manufacturing growth put widespread pressure on the nonferrous metals market. The US Fed's monetary policy path was fraught with twists and turns, and repeated shifts in expectations for interest rate cuts impacted market sentiment. Domestically, China implemented proactive fiscal policies and moderately accommodative monetary policies, attempting to hedge some trade friction risks by strengthening domestic demand and exploring new export channels. The "anti-involution" policy was introduced in July. Looking at the overall performance of commodities, the nonferrous metals sector showed significant internal divergence, but nickel, constrained by its own supply-demand imbalance, performed noticeably weaker than other industrial products.

II. Nickel Market Price Review in 2025

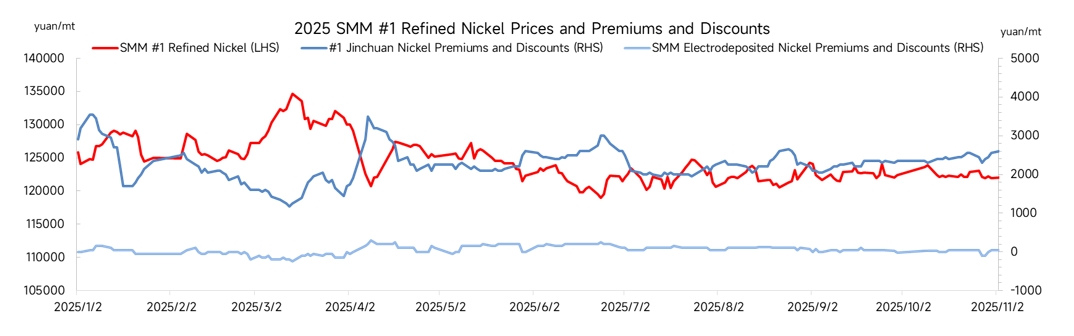

Nickel prices, both domestic and overseas, generally fluctuated downward throughout 2025, with the price center shifting significantly lower. LME nickel prices fell from an opening of $15,365/mt at the start of the year to a low of $13,865/mt. The most-traded SHFE nickel contract dropped from 124,500 yuan/mt to a low of 111,700 yuan/mt, hitting a nearly five-year low. In late December, news that Indonesia, the world's largest nickel producer, planned to significantly cut its RKAB nickel ore quota for 2026 sparked strong expectations of supply-side production cuts, vigorously stimulating bullish sentiment. Nickel prices surged strongly, with LME nickel rising to around $16,000/mt, climbing from the year's low to the H2 high within five trading days.

2025 Q1: Spot prices stabilized at 128,000 yuan/mt, while Jinchuan nickel premiums pulled back from 3,500 yuan to 1,500 yuan. Demand side, post-holiday work resumption was slow with sluggish procurement; supply side, seasonal inventory accumulation suppressed nickel prices and premiums.

2025 Q2: Affected by Sino-US tariff policies, nickel prices fell sharply from 130,000 yuan before rebounding to 125,000 yuan. Jinchuan nickel premiums rebounded to the beginning-of-year level of 3,500 yuan, and electrodeposited nickel premiums also rose.

2025 Q3: Nickel prices moved sideways within the 120,000-125,000 yuan range. Cost support coupled with off-season demand meant the market lacked a one-way driver; electrodeposited nickel capacity was released, and global inventories continued to accumulate. Jinchuan nickel premiums fluctuated rangebound between 2,000-2,500 yuan, while electrodeposited nickel maintained a discount.

2025 Q4: Nickel prices broke below the previous range. Year-end capital repatriation by enterprises led to weaker demand; due to year-end production cuts and tight spot availability, Jinchuan nickel premiums surged significantly from 2,000 yuan to a yearly high of 7,000 yuan, resulting in a notable divergence between premiums and discounts.

III. Expansion Wave Dominated by China and Indonesia

In 2025, domestic refined nickel production in China continues to grow at a high rate, with an expected annual output of 390,000 mt, up 15% YoY; the annual refined nickel production in Indonesia is expected to reach 80,000 mt. The increase mainly comes from electrodeposited nickel produced using MHP (Mixed Hydroxide Precipitate) as raw material through the HPAL (High-Pressure Acid Leaching) process, as MHP can accommodate lower-grade nickel ore, has a higher cobalt extraction rate, and can generate additional revenue through cobalt recovery. In terms of profitability, as of November, the profit margin for producing electrodeposited nickel through the integrated MHP process reached 9%, significantly higher than the -3% for the high-grade nickel matte process. Meanwhile, the planned capacity for MHP in Indonesia will be gradually released from 2026-2027, supporting further growth in refined nickel production with increased supply of intermediate products.

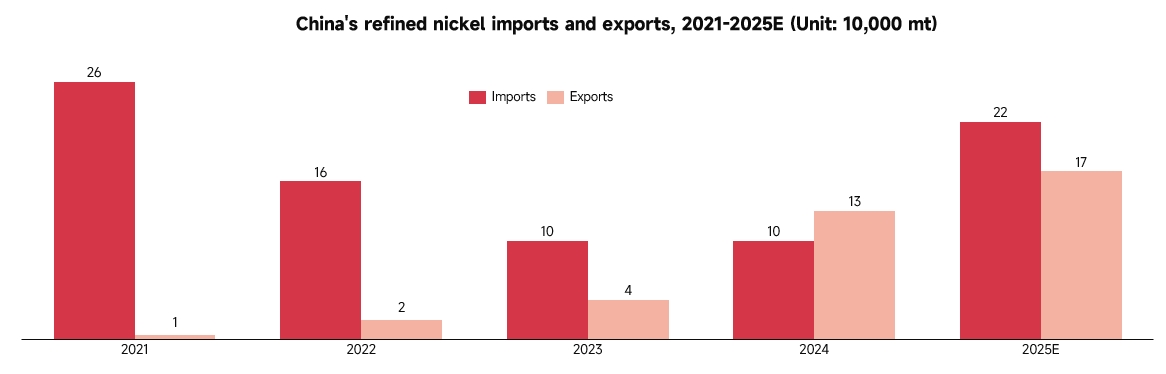

In 2025, the net export position of refined nickel in China is further strengthened. On the import side, due to the explosive growth in domestic electrodeposited nickel capacity, which largely covers domestic demand, the inversion of prices between the domestic and overseas markets becomes the norm. Traditional import brands such as Russian nickel and Nikkelverk nickel are being replaced by domestically produced electrodeposited nickel, with imports of refined nickel declining from 260,000 mt in 2021 to 100,000 mt in 2024, a cumulative decrease of 62%. However, imports are expected to rebound in 2025, reaching 220,000 mt, up 120% YoY. On the export side, the surplus of domestic refined nickel intensifies in 2025, and enterprises must alleviate pressure through exports. Given the strong cost advantages of electrodeposited nickel, it is price-competitive when exported to Southeast Asia and Europe. Domestic brands like Huayou and GEM have successively obtained LME delivery qualifications, leading to a gradual increase in export volumes, with 2025 exports projected to reach 170,000 mt, representing a compound annual growth rate of 141%.

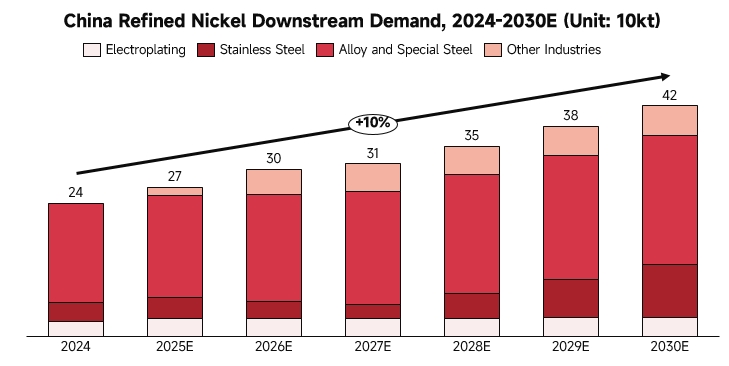

IV. Weak Traditional Demand, Emerging Drivers Yet to Gain Traction

Stainless Steel: Demand has peaked, and its share is shrinking. Currently, stainless steel mills are extensively using nickel pig iron as a substitute for refined nickel, resulting in sluggish actual consumption growth of refined nickel in the stainless steel sector.

Alloy Special Steels: This segment shows the most certain and robust growth, serving as the primary driver of overall demand. The underlying logic is the rapid rise in demand for high-purity nickel driven by the upgrade of China's high-end manufacturing (aerospace, military, wind/PV mounting brackets, high-end tool steels, nickel-based superalloys, etc.).

Electroplating: The annual demand for refined nickel in the domestic electroplating sector is relatively stable, including some high-end electroplating (such as coatings for NEV parts, 5G/consumer electronics connectors), with future demand levels stabilizing around 30,000 mt, constituting a rigid demand that is difficult to replace.

V. Global Inventory Continues to Accumulate

LME Inventory: Surges from 160,000 mt on December 31, 2024, to 250,000 mt on December 22, 2025, an increase of 59%.

SHFE Inventory: As of December 26, inventory stands at 45,000 mt, an increase of about 10,000 mt from the beginning of the year, a 31% increase.

SMM Refined Nickel Social Inventory: By mid-December, the domestic social inventory of refined nickel is 59,000 mt, up 41% YoY.

VI. 2026 Nickel Market Outlook

Looking ahead to 2026, the oversupply situation in the nickel market is expected to continue, with a projected global primary nickel surplus of 120,000 mt. In terms of supply, the continuous release of low-cost MHP capacity in Indonesia will support high levels of refined nickel supply. On the demand side, the main growth points still depend on the stainless steel and new energy sectors: real estate policy support may bring marginal improvements, but substantial recovery in the real estate market will take time, making significant growth in stainless steel demand unlikely. Short-term demand for nickel in ternary batteries is unlikely to see a substantial increase, and the commercial application of solid-state batteries will still require a considerable amount of time, thus failing to provide a significant boost to nickel demand in 2026.

Based on the fundamentals of supply and demand, the center of nickel prices in 2026 may shift further downward. If Indonesia substantially tightens nickel ore supply, LME nickel prices may temporarily break through $16,000/mt, but the medium and long-term oversupply situation is unlikely to change, and the high inventory pressure may take a longer time to digest.

![[SMM Analysis] Explaining Indonesia's Centralized State-run Management of Resource Exports and Future Possibilities](https://imgqn.smm.cn/usercenter/GmHLU20251217171733.jpg)

![[SMM Analysis] Can Indonesia import sulfuric acid as a substitute after the sulfur restriction?](https://imgqn.smm.cn/production/admin/votes/imagesDzORb20240320114304.png)

![[SMM Analysis] After Sulphur Restrictions, Can Indonesia Import Sulphuric Acid as a Replace?

Wait, let me reconsider the translation.

[SMM Analysis] After Sulphur Restrictions, Can Indonesia Import Sulphuric Acid to Replace It?](https://imgqn.smm.cn/usercenter/fzwTi20251217171733.jpg)