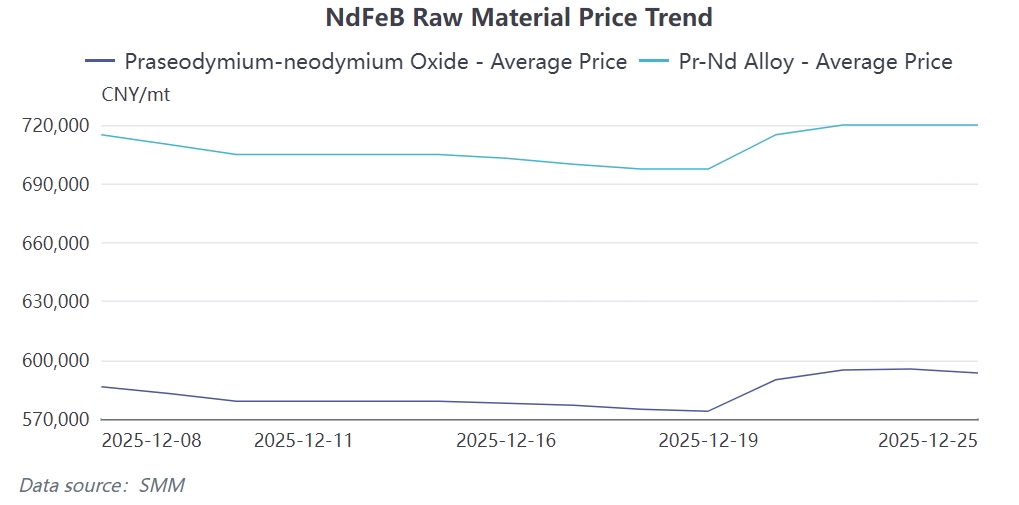

Recently, NdFeB raw material prices for Pr-Nd oxide and Pr-Nd alloy experienced a rapid surge before entering a phase of fluctuation at highs. As of December 25, Pr-Nd oxide settled at 593,500 yuan/mt, up 19,500 yuan WoW; Pr-Nd alloy settled at 720,000 yuan/mt, up 22,500 yuan WoW. Despite the significant short-term increase in raw material prices, NdFeB product prices did not follow suit, with some magnetic material enterprises instead reducing prices for sales. This divergence stems primarily from the fact that the current raw material price increase was not driven by supply-demand fundamentals but was dominated by policy expectations and market sentiment. On one hand, the undersupply pattern of rare earth raw materials throughout 2025 is already established, pushing prices to continue strengthening; on the other hand, actual end-use demand remains weak due to the broader environment, leading to a failure in the price transmission mechanism.

From an annual perspective, the supply-demand dynamics and pace within the rare earth magnetic material industry chain in 2025 differed significantly from previous years. At the beginning of the year, due to export controls and fluctuations in China-U.S. trade relations, magnetic material enterprises frequently adjusted their production plans. In April, export restrictions tightened abruptly, causing market transactions to cool sharply. Demand remained sluggish in May. With the replenishment of short-term orders, shipments rebounded slightly from June to July. A temporary peak was reached in August. The China-U.S. Kuala Lumpur talks in October and the renewed export license policy in November triggered panic stockpiling among end-users, which pulled forward demand expected for the end of 2025. After entering December, end-user purchase willingness weakened significantly due to saturated stockpiles from earlier periods and unclear strategic directions for the new fiscal year. Coupled with a slowdown in overseas holiday order growth, new orders for magnetic material enterprises continued to shrink, leading to sluggish business activity at year-end.

The underlying cause of the current market predicament lies in insufficient support from the demand side. Although rare earth prices remain high due to supply control, the actual consumption growth in downstream sectors such as new energy and wind power has slowed down, exacerbating cost pressures for end-users. Meanwhile, amid the economic downturn, customers have become more cautious about new product development and stockpiling plans, widely adopting low-inventory strategies to avoid inventory devaluation risks caused by price fluctuations. This contradiction of "high raw material costs and weak demand transmission" became particularly evident in December, leaving magnetic material enterprises struggling to raise prices despite facing cost pressures, resulting in continuously narrowing profit margins.

Comprehensively, the year-end rare earth market's "price increase and volume contraction" pattern reflects the interplay between policy-driven factors and weak fundamentals. Short-term panic stockpiling is unlikely to reverse the weakness in demand, while rigid constraints on the supply side will continue to support prices fluctuating at highs. It is anticipated that the restoration of profitability across the industry chain will require a substantial recovery in end-use demand and a rebalancing of supply and demand. At this stage, rare earth permanent magnet manufacturers and downstream end-users are placing greater emphasis on liquidity and the timing of stockpiling.