The Middle East is undergoing a steel industry transformation driven by a confluence of energy transition, economic diversification strategies, and geopolitical dynamics. As one of the world's fastest-growing regions in terms of crude steel production growth, the Middle Eastern market exhibits distinct characteristics: state-led development, divergent strategic paths, and a significant influx of foreign investment.

Part I: In-Depth Analysis of National Strategies and Policy Toolkits

-

Saudi Arabia: High Protection Paired with Strong Incentives to Build a Fully Integrated Steel System for Import Substitution

Within the framework of Vision 2030, Saudi Arabia is systematically promoting import substitution in the steel industry through a parallel approach of high trade protection, strong investment incentives, and localization policies. The goal is to establish a complete, internationally competitive steel industrial chain by 2030.

Through Vision 2030 and the National Industrial Strategy, Saudi Arabia has elevated the steel industry to a national strategic priority. Its core objective is to achieve self-sufficiency in steel and become one of the world's top 15 steel-producing nations by 2030. To this end, the government has implemented a three-pronged policy mix: imposing 10–20% import tariffs and frequently launching anti-dumping investigations on the trade front; offering tax exemptions for up to 20 years and project financing support of up to 75% on the investment front; and, regarding the green transition, setting a 2060 carbon neutrality goal while primarily relying on low-cost energy advantages to maintain competitiveness in the short term. More structurally significant is the IKTVA localization program, which mandates the procurement of a certain proportion of local content in energy and construction projects, creating a relatively stable demand base for domestic steel mills. Driven by this policy mix, Saudi Arabia has become one of the most attractive global destinations for steel investment in recent years.

-

United Arab Emirates (UAE): Leveraging Clean Energy Advantages to Build a Green, High-End Steel Manufacturing Hub for the Global Market

In an open trade and investment environment, the UAE is capitalizing on its nuclear and renewable energy advantages to explicitly position its steel industry as a low-carbon, high-end manufacturing hub targeting international markets.

Guided by the "Operation 300 billion" strategy, the UAE is fully leveraging its clean energy endowment to drive the steel industry toward low-carbon and high-end development. At the policy level, this manifests as a relatively open trade environment (implementing the 5% GCC Common External Tariff), an investment incentive system centered on free zones (including 100% foreign ownership and tax benefits), and a green transition pathway focusing on electric arc furnace (EAF) steelmaking. Notably, Emirates Steel has begun producing internationally certified low-carbon steel, with unit carbon emissions approximately 60% lower than the global average. Against the backdrop of the EU's Carbon Border Adjustment Mechanism (CBAM) being gradually implemented, this advantage is poised to translate into tangible market competitiveness. Overall, the UAE has successfully converted its energy advantages into industrial strengths, gradually forming a complete value chain from clean power to green steel.

-

Iran: An Inward-Looking Steel Development Model Oriented Toward Capacity Expansion Under Sanctions Constraints

Under long-term sanctions, Iran's steel industry has prioritized capacity expansion and import substitution, but the effective release of capacity and structural upgrading remains constrained by energy, equipment, and institutional limitations.

The Seventh Five-Year Development Plan set a target of achieving 55 million tons of crude steel capacity by 2026. By 2024, Iran's nominal crude steel capacity had already reached approximately 58.2 million tons, exceeding the planned target ahead of schedule. However, capacity utilization faces significant bottlenecks: actual crude steel production in 2024 was only about 31 million tons, representing a capacity utilization rate of approximately 53%. Key constraints include restrictions on equipment imports and technology upgrades due to sanctions, energy shortages affecting the stable operation of blast furnaces and EAFs, and insufficient supporting infrastructure, which lowers overall production efficiency. On the policy front, Iran reinforces import substitution through strict import licensing and foreign exchange controls. Although foreign investment is officially encouraged, financial settlement and equipment procurement obstacles are significant. Concurrently, environmental pressures are mounting, but meeting emission reduction targets faces practical challenges due to aging blast furnace equipment.

-

Other Regional Countries: Embedding into the Regional Division of Labor Through Specialization

Countries like Qatar, Oman, and Bahrain play complementary, rather than dominant, roles in the Middle Eastern steel industry through specialization and regional collaboration.

Qatar Steel primarily serves large domestic infrastructure and energy projects; Oman, leveraging its port and logistics advantages, has attracted foreign companies like India's Jindal Group to establish export-oriented steel capacity; Bahrain's United Steel Company has developed into a major long product exporter in the Gulf region. While the scale of the steel industry in these countries is relatively limited, they maintain a degree of competitiveness within the Middle Eastern steel industry system through clear niche market positioning and regional synergy.

Part II: Deep Dive into Mainstream Enterprise Landscape and New Capacity Additions

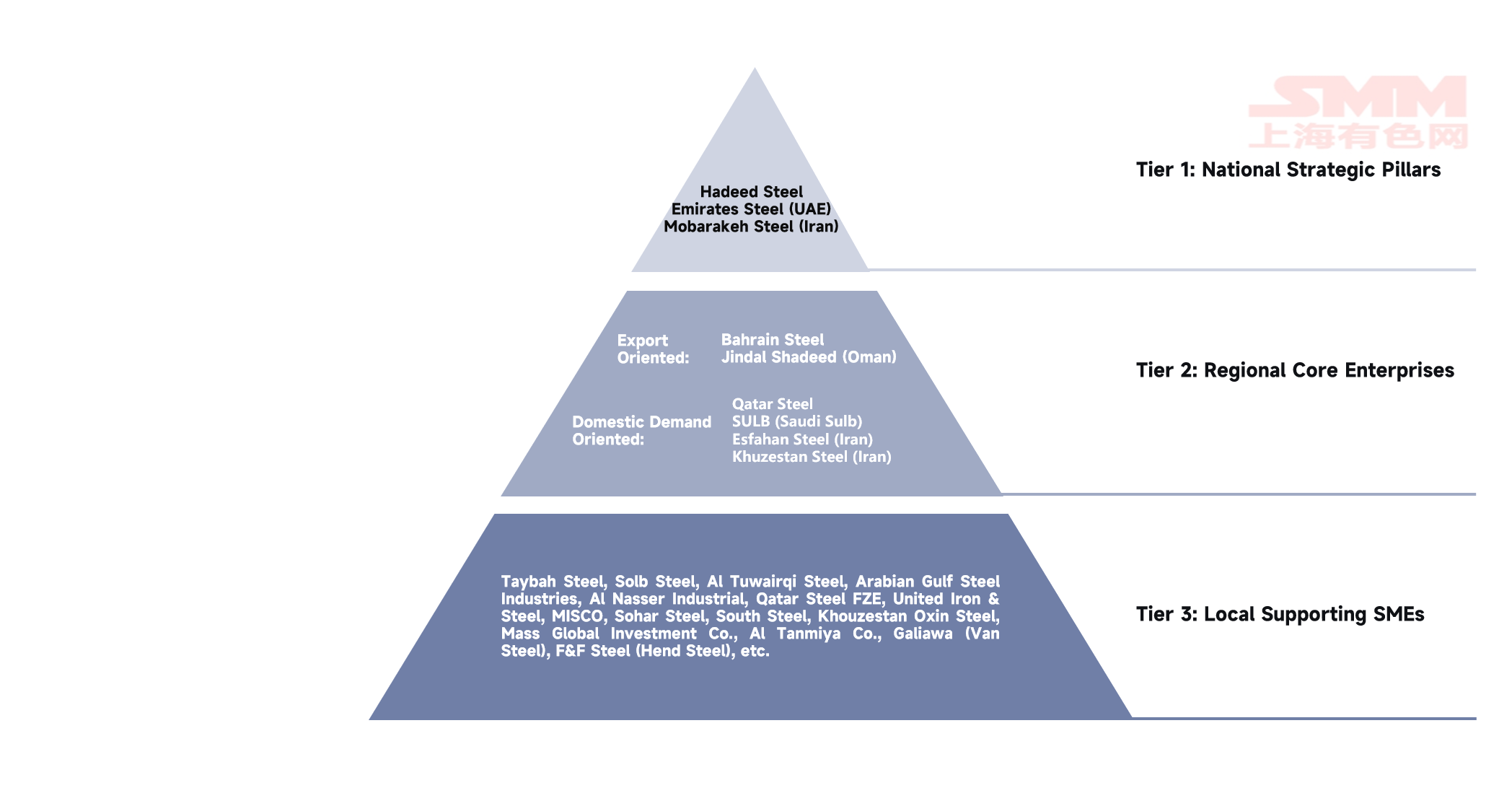

Mainstream Competitive Landscape: Trio of Nations Dominate, with Clear Tiers

Data Sources: SMM, WSA.

Data Sources: SMM, WSA.

From a technological pathway perspective, the resource endowment of the Middle East—"scarce in coking coal, abundant in natural gas"—dictates its steel industry's reliance on the "Natural Gas-based Direct Reduced Iron (DRI) + Electric Arc Furnace (EAF)" route, accounting for approximately 95% of production. Only Iran retains some Blast Furnace-Basic Oxygen Furnace (BF-BOF) capacity due to its coking coal resources and historical reasons. Capacity distribution is highly concentrated, with Saudi Arabia, Iran, and the UAE accounting for over 80% of the region's total capacity, showing clear tier differentiation.

Data Sources: SMM, WSA, GEM.

Data Sources: SMM, WSA, GEM.

The first tier consists of national champion enterprises: Saudi Iron and Steel Company (HADEED, part of SABIC, now under PIF), Emirates Steel (part of ADQ), and Iran's Mobarakeh Steel. These three steelmakers have a combined capacity exceeding 24 million tons, dominating the regional landscape. Saudi Iron and Steel Company (HADEED), as Saudi Arabia's first fully integrated steel producer, is accelerating consolidation after its acquisition by the Public Investment Fund (PIF) in 2024, with plans to invest in expanding high-end flat products (e.g., automotive sheets). Its crude steel capacity in 2024 is approximately 6.2 million tons, covering certain categories of long and flat products. Emirates Steel focuses on green transformation, with its low-carbon steel boasting emissions 60% below the global average (internationally certified), and a capacity of about 3.6 million tons in 2024. Iran's Mobarakeh Steel is the Middle East's largest single-site steel plant with 14.1 million tons of capacity, specializing in flat products, maintaining high-capacity utilization despite sanctions. Iran's Esfahan Steel is one of the few regional companies still using the BF-BOF route, with 3.6 million tons of capacity focused on construction materials, serving southern infrastructure projects using domestic coking coal. Iran's Khuzestan Steel also possesses 3.6 million tons of EAF capacity, providing steel support for the southern energy and petrochemical base.

The second tier comprises regional specialist’s dominant in niche markets. Oman's Jindal Shadeed Iron & Steel, controlled by India's Jindal Group, has 2.4 million tons of EAF capacity producing billets, rebar, and hot-rolled products. Leveraging the logistical advantages of Sohar Port, it exports significantly to South Asia and Africa. Qatar Steel, with 2.57 million tons of capacity, fully serves domestic mega-projects. Bahrain's United Steel Company holds over 40% market share in the Gulf region for long products with 1.1 million tons of capacity, serving as a core player in regional long product trade. Saudi Arabia's Al Ittefaq Steel focuses on long products with 3.6 million tons of capacity, deeply integrated with domestic construction and the IKTVA program.

The third tier consists of numerous small and medium-sized EAF mills distributed in Iraq, Kuwait, Saudi Arabia, the UAE, etc. They mainly produce basic long products like rebar and wire rod, serving local construction markets. Representative enterprises include Iraq's Mass Global Investment Co. (1.25 million tons), Oman's MISCO (1.2 million tons), Kuwait Steel Company (1.2 million tons), Saudi Arabia's Al Tuwairqi Steel (1.63 million tons), etc. These companies have weaker bargaining power and are susceptible to fluctuations in raw material prices and demand.

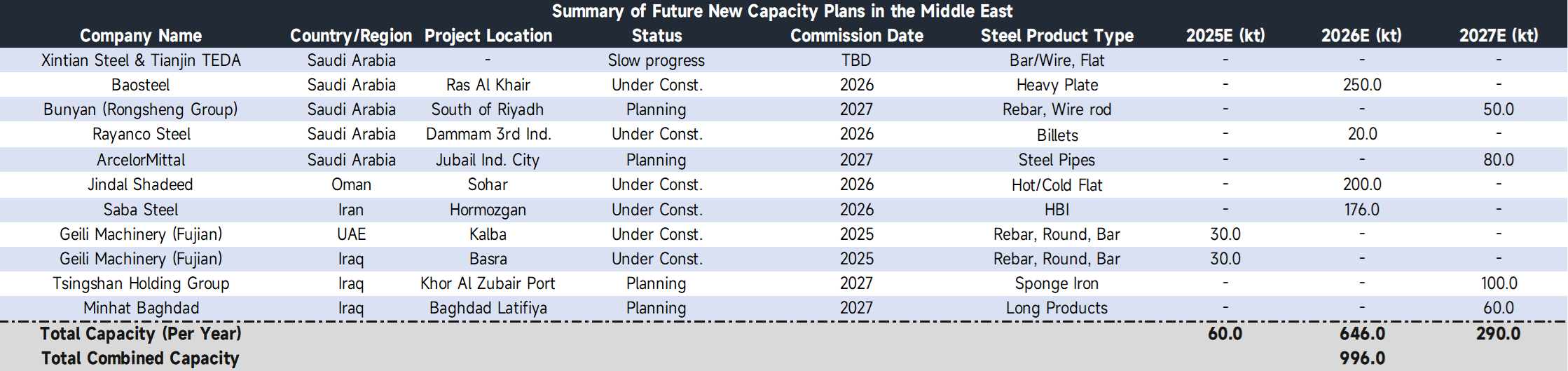

Perspective on New Capacity Additions: Significant Scale Expansion and Structural Upgrading

The next three years mark a concentrated period for new capacity commissioning in the Middle East, with planned additions totaling approximately 10 million tons, all based on the "Natural Gas-based DRI + EAF" route. 2026 is the peak year for commissioning, with Saudi Arabia contributing over half of the new capacity.

Data Source: SMM, GEM.

Data Source: SMM, GEM.

As the main force in expansion, Saudi Arabia is advancing both high-end and large-scale projects. China Baowu's Heavy Plate project (2.5 million tons) is progressing smoothly and expected to commence operation in 2026, filling the regional gap for high-end heavy plates. Benefiting from the Jubail Industrial City's supporting infrastructure and policy support, it has high certainty of realization. The New Tianjin Steel Group's 2.5 million tons integrated steel project is progressing slowly due to factors like local content requirements and labor policies. ArcelorMittal's 800,000 tons seamless pipe project is in the planning stage, aiming to enhance industrial supporting capabilities. Overall, Saudi Arabia's new capacity additions possess the highest certainty of realization within the region in terms of policy clarity and demand underpinning. However, local content requirements will be a core constraint for foreign-invested projects.

Oman focuses on export-oriented expansion. Jindal Shadeed's 2 million tons Hot Rolled/Cold Rolled flat products project is proceeding smoothly, slated for 2026 commissioning, aiming to expand into global markets leveraging port advantages. Iran's expansion reflects more of a strengthening on the raw material side. The Sabzevar Steel 1.76 million tons Hot Briquetted Iron (HBI) project is under construction, but equipment import delays due to sanctions have caused schedule slippage. Iraq focuses on supporting domestic infrastructure. The Geely Machinery 300,000 tons rebar project is expected in 2025, and Tsingshan Holding's 1 million tons DRI project is planned for 2027. However, both countries face operational risks such as unstable power supply, weak infrastructure, and political volatility, introducing uncertainty into project advancement. It is important to note that against the backdrop of a regional average capacity utilization rate of only about 50%, the actual commissioning schedule and operational ramp-up rates of these new projects remain subject to significant uncertainty.

Part III: Supply-Demand and Trade Patterns in the Middle East

In 2024, the Middle East's total crude steel production reached 54.1 million tons, but its capacity utilization rate was only 50%, reflecting significant structural disparities within the region. Iran's crude steel production in 2024 stood at 31.4 million tons, with exports of approximately 10.8 million tons. Iran has established significant cost competitiveness in long products, making it a key steel supplier within the Middle East and to surrounding markets.

This contrasts sharply with the Gulf Cooperation Council (GCC) countries. Despite hosting massive construction demand, their domestic production falls short. Saudi Arabia's crude steel production in 2024 was only 9.6 million tons, and the UAE's was about 3.7 million tons. The huge supply-demand gap forces them to rely heavily on international markets. In 2024, the UAE was a net importer of approximately 8.6 million tons, and Saudi Arabia about 4.6 million tons. GCC countries primarily depend on imports to fuel their ambitious infrastructure and industrialization projects. Unwilling to remain pure buyers long-term, they are pursuing "import substitution" strategies—especially Saudi Arabia, which aims to transform itself into an exporter.

Currently, the high-end steel market in the Middle East remains heavily dependent on imports from China, Japan, and South Korea, which dominate with their technological and supply chain advantages. Long product trade circulates more within the GCC. If Saudi Arabia's capacity plans materialize, its long products could first substitute for some imports from Turkey and the CIS within the region. However, achieving large-scale net exports and expanding into African and South Asian markets will still face severe challenges, including demand absorption, logistics costs, and intense international competition.

Regarding product structure evolution, construction-related long products currently dominate the Middle East, accounting for about 65%. However, with the development of high-end industries like automotive manufacturing under Saudi Arabia's Vision 2030 and aerospace in the UAE, the share of flat product consumption is expected to rise steadily. The localization of high value-added products like automotive sheets and special heavy plates has become a core objective for industrial upgrading in these countries, offering clear long-term market entry points for companies with technological advantages, although the import substitution process will likely be more protracted than anticipated.

Part IV: Future Challenges and Strategic Opportunities

-

Major Challenges Ahead

The Middle Eastern steel industry faces multiple challenges in the future: First, risks of overcapacity and structural mismatch. With approximately 10 million tons of new capacity planned in the next three years and a peak in commissioning expected in 2026, demand growth is limited. Given the region's already insufficient capacity utilization rate, if high-end capacity fails to materialize as planned, low-price competition could intensify. Second, technological and operational bottlenecks, including shortages of skilled talent for high-end flat product production, equipment upgrade constraints due to sanctions in Iran, and operational risks like power supply, infrastructure, and political volatility in Iraq and other countries. Third, green transition pressures. Saudi Arabia and Iran still rely on traditional processes, transitioning to low-carbon steelmaking requires massive investment, and mechanisms like the EU's CBAM could increase export costs for high-carbon steel from the region. Fourth, trade versus localization contradictions. GCC countries promote "import substitution," but high-end products will remain import-dependent in the short term. Foreign-invested projects must meet local content requirements, making it challenging to balance costs and compliance.

-

Structural Opportunities and Strategic Roles

However, challenges breed structural opportunities. For China, the Middle East is demonstrating multiple advantages as a future core engine for exports and industrial cooperation. On the demand side, it benefits from long-term, certainty-driven growth fueled by national-level strategies, transitioning from basic infrastructure to high-end manufacturing. Geopolitically and in trade, the Middle East, with its superior location, advanced logistics, and open policies, is gradually replacing Turkey and emerging as a new trade and logistics hub connecting Asia, Africa, and Europe. Crucially, downstream processing and manufacturing clusters—represented by steel pipes, metal structures, and automotive components—are rapidly forming in the Middle East. Leveraging local low-cost energy and incentive policies, a significant agglomeration effect is taking shape. This five-dimensional combination of "stable demand, hub status, open environment, manufacturing base, and cost advantage" positions the Middle East not only as a crucial export destination for Chinese products but also as a strategic springboard for Chinese enterprises to engage in capacity cooperation, establish regional manufacturing centers, and radiate into broader global markets.

-

Medium- to Long-Term Outlook

Looking ahead, three major trends are expected in the Middle Eastern steel industry: (I) The consolidation of a dual-center structure of "Saudi Arabia dominating scale + UAE leading in green high-end." Saudi Arabia will control the basic steel market with its capacity and industrial chain advantages, while the UAE will become a high-end steel hub with its low-carbon technology. (II) Accelerated product structure upgrading. With the expansion of Saudi Arabia's automotive manufacturing and the UAE's aerospace industries, the share of flat product consumption will gradually increase. Import substitution for high-end products like automotive sheets and special heavy plates becomes a core direction, offering long-term opportunities for technologically advantaged companies. (III) Deep transformation of trade and industrial roles. Saudi Arabia is poised to shift from a "net importer" to a more balanced trade position, with long products gradually substituting for extra-regional imports and seeking export opportunities. Foreign enterprises will evolve from mere exporters to deep collaborators participating in local high-end capacity building and downstream industry cluster development. Overall, the Middle Eastern steel industry is gradually transitioning from "scale expansion" to "quality upgrading and value chain integration," poised to play an increasingly important participant role in the global steel industry's low-carbon transition and structural reshaping.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)