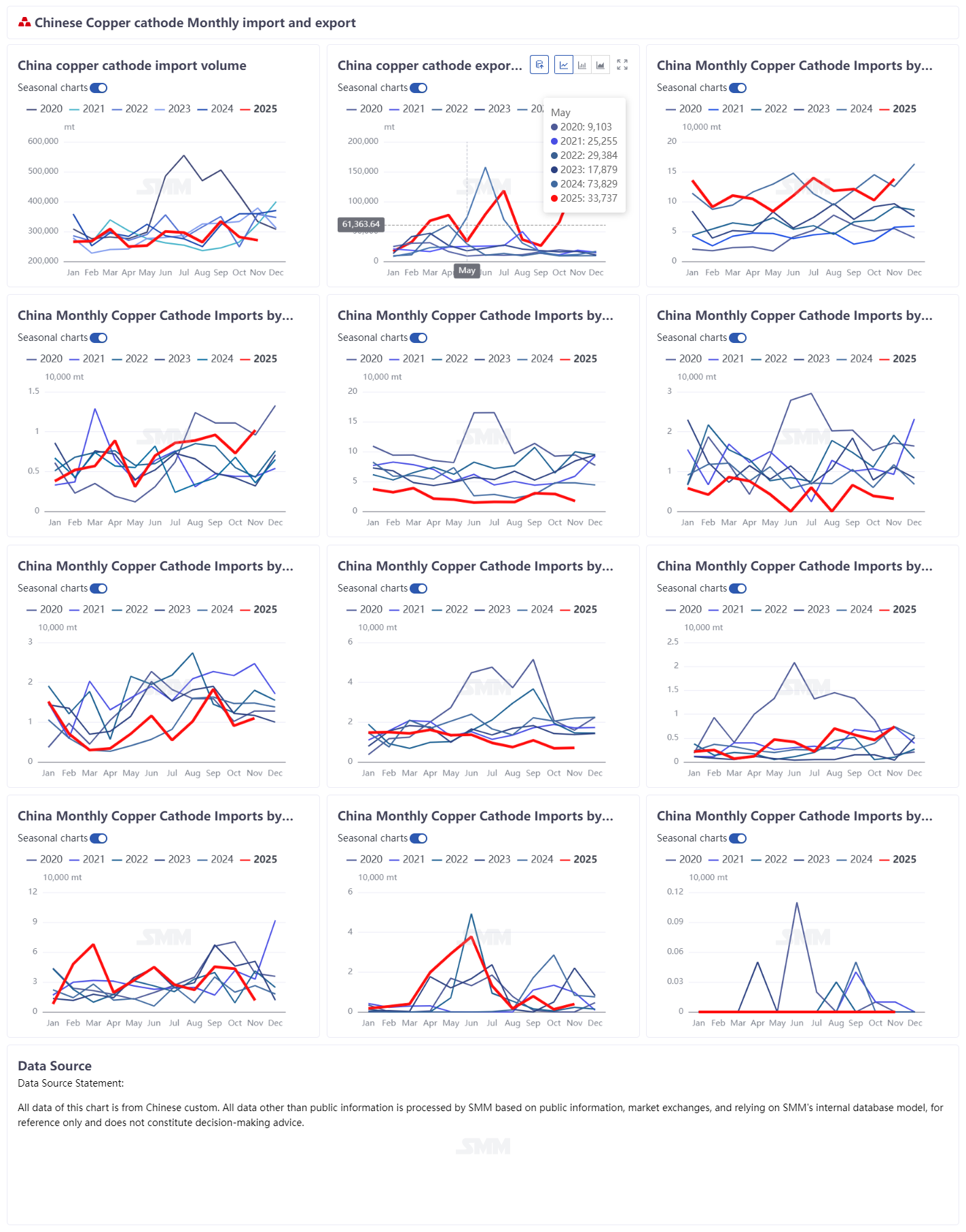

According to customs data, China’s refined copper imports totaled 271,100 tons in November 2025, down 3.90% month-on-month and 24.67% year-on-year. In the same period, exports surged to 143,000 tons, marking a 116.83% MoM increase and a remarkable 1128.09% YoY growth.

In November, refined copper imports remained at a low level, though supply from Africa showed some recovery compared to the previous month. The Democratic Republic of Congo (DRC) remained China’s largest source, with monthly imports reaching 138,200 tons, accounting for 51% of the total—up 34.77% MoM and 10.29% YoY. However, imports from other major producers such as Russia, Kazakhstan, Zambia, and Chile declined overall. This reflects China’s growing dependency on African-origin copper, with a rising concentration of import sources. Notably, non-LME-registered brands now account for over 70% of total imports, indicating that the current narrow brand mix—especially wet-process copper and non-registered brands—is likely to persist through year-end.

On the export front, China’s refined copper exports exhibited strong counter-cyclical momentum in November, exceeding 140,000 tons—second only to the June 2024 record of 157,700 tons. The surge was driven partly by the widening LME-COMEX spread, which incentivized traders to re-export bonded CME-registered warrants and November-arrival cargos. Another key driver was the significant expansion of the export window, prompting smelters to release substantial volumes to the international market. Notably, China’s copper exports showed greater destination diversification: in addition to traditional delivery destinations, market share in Europe, the Middle East, and Southeast Asia also expanded.

Looking ahead, China’s refined copper is beginning to displace other suppliers in non-US regions. In early December, export activity is expected to remain relatively high as the window remains open. However, with the LME-COMEX arbitrage window narrowing recently, re-export arbitrage will likely decline. The sharp drop in net imports in November suggests that China’s apparent copper consumption has fallen short of market expectations since then. Seasonal demand weakness is expected to persist through year-end, and although December’s net imports may show a slight MoM improvement, they will likely remain significantly lower on a YoY basis.