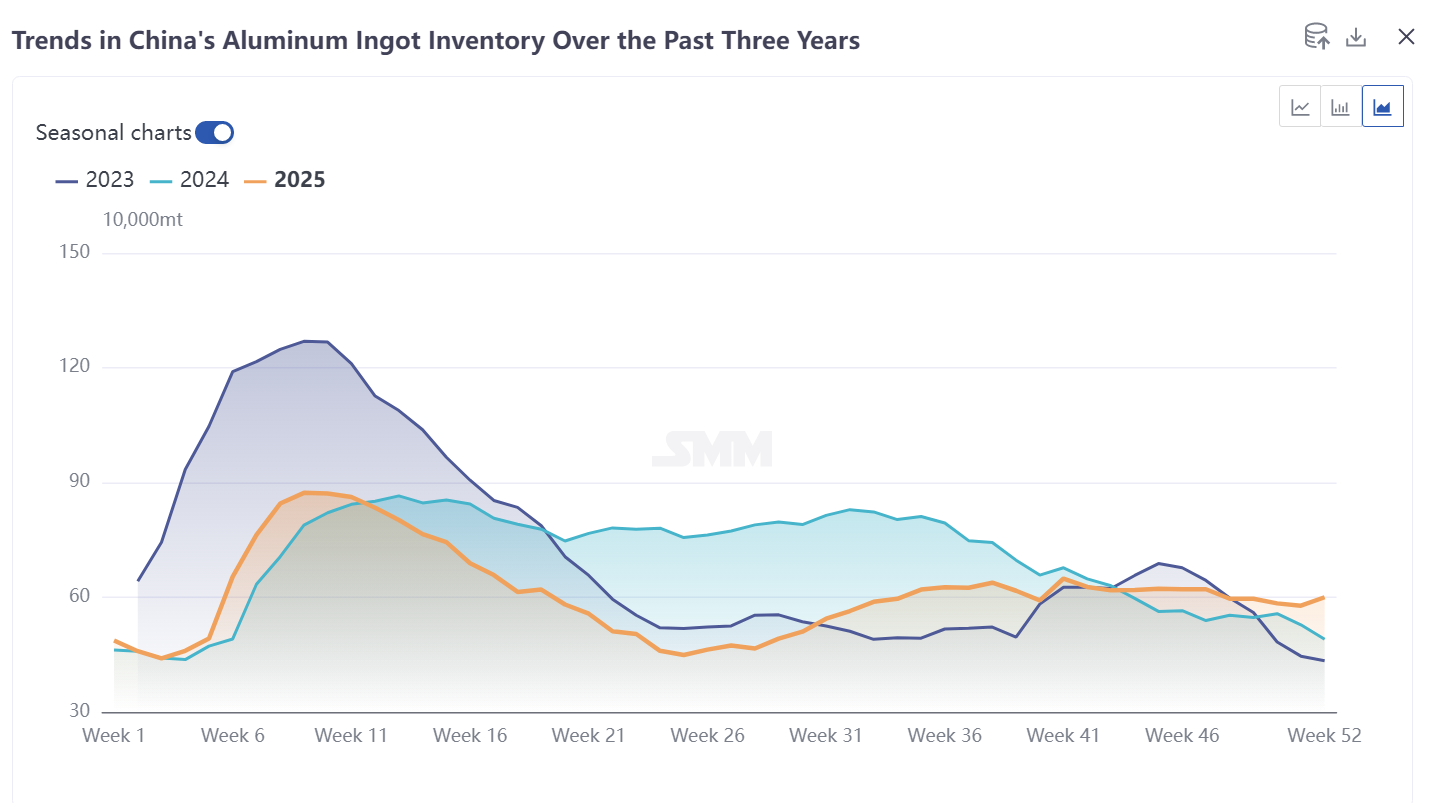

Recently, the domestic aluminum ingot market inventory structure has undergone a phased adjustment. The previously troubling backlog of shipments from Xinjiang has been gradually resolved, leading to a rebound in supply chain circulation efficiency. However, at the same time, inventory buildup pressure has emerged in some storage areas, compounded by regional market differences and weak downstream demand. As a result, domestic aluminum ingot inventory is characterized by "overall circulation improvement with localized pressure becoming prominent." This article provides an in-depth analysis of the current domestic aluminum ingot inventory situation based on the latest shipment, in-transit, and storage area feedback data, and offers predictions for future trends.

I. Core Current Situation: Shipping Backlogs Fully Eased, Concentrated Arrivals Trigger Phased Inventory Buildup

The Xinjiang shipping issues that previously constrained the circulation of aluminum ingots have been fundamentally resolved. Multiple sources confirm that the backlog situation for aluminum ingots in Xinjiang has significantly improved, and the shipping segment of the supply chain has returned to normal. Feedback from the logistics side indicates that aluminum ingot shipments via dedicated railway lines operated by a certain logistics company are now smoothly exiting warehouses, with no backlog at the stations. The planned arrival targets for this week are expected to be successfully met, marking the resolution of the core bottleneck that previously hindered circulation.

Notably, following the alleviation of shipping backlogs, previously delayed goods have arrived at warehouses in a concentrated manner, leading to a phased inventory buildup. Data shows that from last weekend to the first two days of this week, the inventory buildup trend was particularly pronounced in key domestic aluminum ingot storage areas. While this phenomenon is partly due to renewed environmental protection-related production cuts downstream on the demand side, the primary reason remains the phased outcome of the concentrated release of goods after the improvement in backlog issues last week. From the perspective of subsequent support from the circulation side, there is currently no significant backlog at railway stations, with only routine station cargo volumes maintained. Coupled with stable in-transit volume data showing no significant increase, this indicates that the current concentrated shipping phase has concluded. Subsequently, the pace of aluminum ingot shipments and arrival volumes are expected to gradually return to normalized levels.

Specifically, regarding in-transit volume data, the overall trend recently showed an "initial rise followed by stabilization": in early December, the backlog situation was more severe, with a noticeable decrease in aluminum ingot rail in-transit volumes, and significant declines in in-transit volumes to Wuxi and Gongyi, two major consumption areas. By mid-December, in-transit volumes to both areas climbed simultaneously, reflecting the trend of concentrated shipments of previously backlogged goods. As of this week, although in-transit volumes to both areas have retreated from the earlier highs, they remain at relatively high levels overall, which also brings some pressure for subsequent inventory digestion in storage areas.

II. Regional Differentiation: Prominent Inventory Buildup Pressure in Central China, East China Taking on Increased Inflow

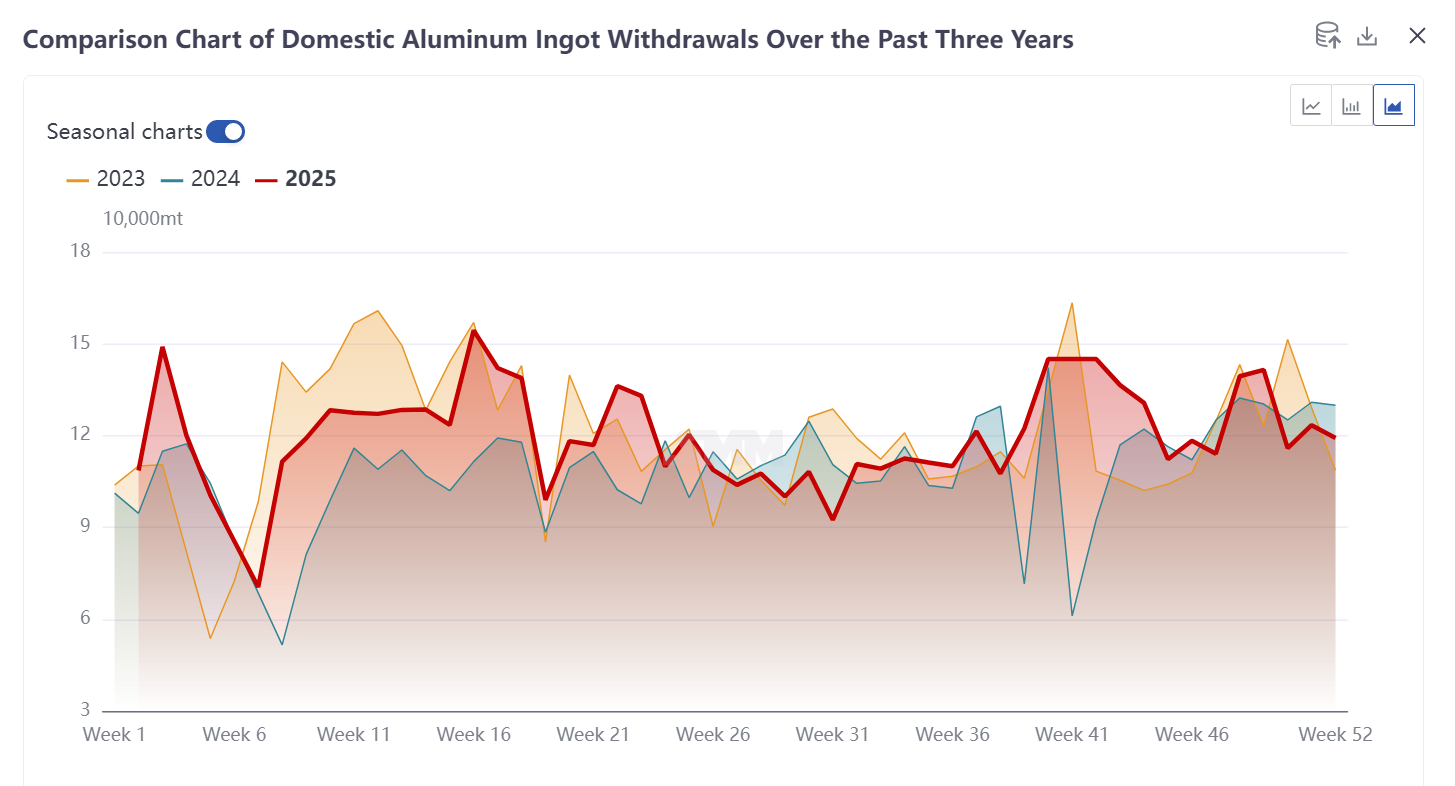

The core contradiction in the current domestic aluminum ingot inventory centers on regional differentiation, with the two major core warehouse areas of Gongyi and Wuxi exhibiting a pattern of "uneven pressure." Among them, the Gongyi warehouse area is currently facing relatively significant inventory buildup pressure, driven by two core factors: On one hand, the enthusiasm for downstream cargo pick-up remains persistently low, with leading local aluminum processing enterprises implementing production cuts due to the impact of environmental protection-related controls, directly leading to a decline in the digestion capacity on the demand side for aluminum ingots, a slowdown in inventory turnover efficiency, a marked weakening in warehouse withdrawals, and concerns among some warehouses about the risk of overstocking; on the other hand, the cumulative effect of previous concentrated arrivals has further exacerbated short-term inventory pressure.

In stark contrast to the Gongyi warehouse area, the Wuxi warehouse area, leveraging its regional price spread advantage, is poised to become the core destination for subsequent aluminum ingot shipments. Currently, aluminum ingots in the Gongyi market are trading at a significant discount, and from a cost-benefit perspective, aluminum plants' subsequent shipment flows will significantly tilt towards the Wuxi market, with the volume of aluminum ingots expected to gradually increase in the Wuxi warehouse area. This flow adjustment will not only alleviate the inventory buildup pressure in the Gongyi warehouse area but also reshape the regional distribution pattern of domestic aluminum ingot inventory, leading to notable changes in the price spreads among mainstream domestic aluminum ingot consumption areas by year-end. The subsequent inventory in the Wuxi warehouse area may exhibit a mild growth trend, but thanks to its regional demand foundation and circulation efficiency advantages, the inventory digestion pressure will remain relatively manageable.

III. Cost Drivers: Highway Transport Supplement Withdraws, Logistics Costs Return to Rational Levels

From a logistics cost perspective, the supplementary transport channels temporarily activated earlier due to shipping backlogs have gradually withdrawn from the market. Among these, an aluminum group previously temporarily utilized highway transport for aluminum ingots to alleviate shipping pressure. Currently, with railway shipments returning to normal, the highway transport channel has officially ceased operation. The core reason is that highway transport costs are significantly higher than railway transport; given smooth railway shipments, highway transport lacks economic advantage. This change further confirms that aluminum ingot shipments and logistics links in north-west China have returned to normal, and supply chain costs will gradually revert to rational levels.

IV. Subsequent Outlook: Inventories Gradually Stabilize, Focus on Demand Recovery Pace

Overall, domestic aluminum ingot inventories have passed the earlier volatile phase of "backlog-concentrated release" and are expected to gradually enter a stable operating range. In the short term, the Gongyi area still needs to digest inventory pressure from previous concentrated arrivals, while the Wuxi area will absorb some of the increased shipments, leading to a gradual optimization of regional inventory structures. Medium and long-term, as the effect of concentrated shipments subsides, subsequent arrivals are expected to stabilize, and inventory trends will primarily depend on the pace of year-end rigid demand pick-ups and pre-holiday stockpiling by downstream users. If environmental protection-related controls are marginally relaxed, production resumptions by processing enterprises in Gongyi could lead to a rebound in cargo pick-up demand, effectively alleviating local inventory pressure. If demand remains persistently weak, domestic aluminum ingot inventories may continue to fluctuate at highs. For market participants, it is advisable to closely monitor two key indicators: first, daily and weekly inventory change data for the major warehouse districts in Gongyi and Wuxi to track the progress of regional inventory buildup pressure relief; second, operating rates and cargo pick-up data from downstream processing enterprises to gauge the shifting pace of demand. Subsequently, as regional inventory disparities become clearer, regional aluminum ingot price spreads may undergo further adjustments, presenting periodic opportunities for trading segments.

In summary, entering late December, disruptions on the aluminum ingot supply side have eased, but short-term supply pressure has increased. Demand side, warehouse withdrawals in Gongyi have weakened significantly due to environmental protection-related controls, and demand stability is difficult to maintain under the suppression of high aluminum prices. SMM expects the domestic aluminum ingot inventory trend in late December to still show a slight increase within a stable range, operating around 580,000-650,000 mt, with a high probability that month-end inventory will be above 600,000 mt, which is expected to exert some negative feedback on the performance of aluminum futures and spot markets towards year-end.

![Aluminum Producers' Operating Rates Rebound to 61.9%; High Prices Challenge "Golden March" Peak Season [SMM Survey]](https://imgqn.smm.cn/usercenter/tXCfs20251217171653.jpg)

![ADC12 Prices Rose Again This Week[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)