Introduction

Recent news from Bloomberg, citing sources within the Indonesia Nickel Miners Association (APNI), indicate that Indonesia could be steering toward a major turn in the global nickel supply chain. The government is reportedly weighing a plan to slash the approved nickel ore production quota, known as RKAB, for 2026 to around 250 million tons, which would represent a drop of roughly 34% compared to 2025 levels. If finalized, the move would signal a notable shift in policy from the world’s top nickel producer, with the clear intent of tightening supply and supporting nickel prices, which have remained under pressure. Whether such a reduction is practically feasible, however, remains an open question.

As background, based on SMM’s discussions with the Ministry of Energy and Mineral Resources (ESDM), the government has indeed begun tightening nickel ore “supply” controls in response to persistent market oversupply. SMM’s internal data shows that Indonesia’s actual nickel ore production in 2025 is estimated at approximately 265 million tons, well below the approved RKAB quota of about 326 million tons. This gap highlights that not all approved quotas are ultimately realized in the market.

In parallel, the government is increasingly focused on preserving and extending the life of Indonesia’s nickel resources. According to ESDM, the average nickel ore grade in 2024 stood at around 1.66%. However, within just one year, the average saprolite grade has declined to approximately 1.57%, a near 0.1 percentage point drop, which is significant for the industry. This rapid deterioration in ore quality reflects accelerated mining of higher-grade resources. If supply is left unchecked and exploration fails to keep pace with demand growth, Indonesia’s economically viable nickel ore reserves could be depleted at a much faster rate.

From this perspective, the volume of nickel ore actually released to the market is already more constrained than headline RKAB figures suggest. In the government’s defense, the 2026 quota regime is expected to be accompanied by stricter approval requirements, including the obligation to fully pay reclamation guarantees, as well as tighter scrutiny of miners’ production records, exploration performance, and operational capability. These measures are intended to improve discipline and ensure sustainable mining practices.

From SMM’s standpoint, forecasting Indonesia’s 2026 nickel ore quota should be approached from two key angles:

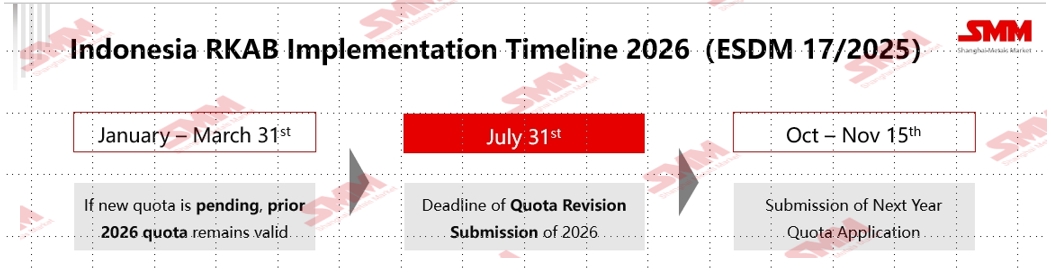

I. There are “Two” RKAB Application Process of 2026

Although the previous three-year RKAB framework has been reverted to an annual system under ESDM Regulation No. 17/2025, the quota application and adjustment process for 2026 is still ongoing. Under Article 11 and Article 12 of the regulation, miners are allowed to apply for quota revisions or additional allocations up until 31 July 2026, subject to specific conditions. Therefore, it remains premature to conclude that total approved quotas will be strictly capped at 250 million tons. Well-established, large-scale miners with strong compliance records may still seek higher quotas to support additional sales or operational expansion.

II. Rising Smelter Demand in 2026

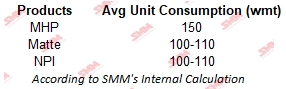

Nickel ore demand is expected to increase further in 2026 as new smelting capacity comes online, particularly in the hydrometallurgical segment. The government’s push for low-emission, higher value-added downstream development has encouraged investment in HPAL projects producing MHP. While Indonesia still has fewer HPAL facilities compared with RKEF-based pyrometallurgical operations, hydrometallurgy capacity will expands steadily.

Importantly, lower average ore grades mean higher ore consumption per unit of nickel output. Producing one ton of MHP requires substantially more ore when feed grades decline. According to SMM’s forecasts, Indonesia could see more than 200,000 tons of additional nickel metal output in 2026, which would translate into a significant increase in nickel ore demand. This estimate does not yet fully account for additional capacity from Nickel Matte, NPI, and FeNi projects that are either under construction or in planning stages.

To put this into perspective, SMM’s internal data shows that Indonesia’s nickel ore demand in 2025 could reach around 280 million wmt. Even after factoring in production cuts, maintenance shutdowns, or delays at some smelters, the commissioning of new projects in 2026 is likely to push ore demand above 2025 levels.

III. SMM's Conclusion

While Indonesia’s aim to reduce nickel ore supply is clear, which is driven by price and resource sustainability goals, a blanket reduction of the 2026 RKAB quota to 250 million tons may prove difficult to sustain in practice. Several factors could push the final approved quota higher, including rising downstream demand, declining ore grades, and the RKAB system's own mid-year revision mechanism. SMM estimates Indonesia's approved nickel ore RKAB for 2026 is likely to remain above 250 million tons, unless policy enforcement becomes significantly more stringent than in previous years.

![[SMM Stainless Steel Flash] April 2, 2026: Stainless Steel Market Highlights](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)

![[SMM Analysis] Nickel Salt Prices Edge Down Amid Weak Downstream Demand and Rising Raw Material Costs](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)