SMM December 22 News:

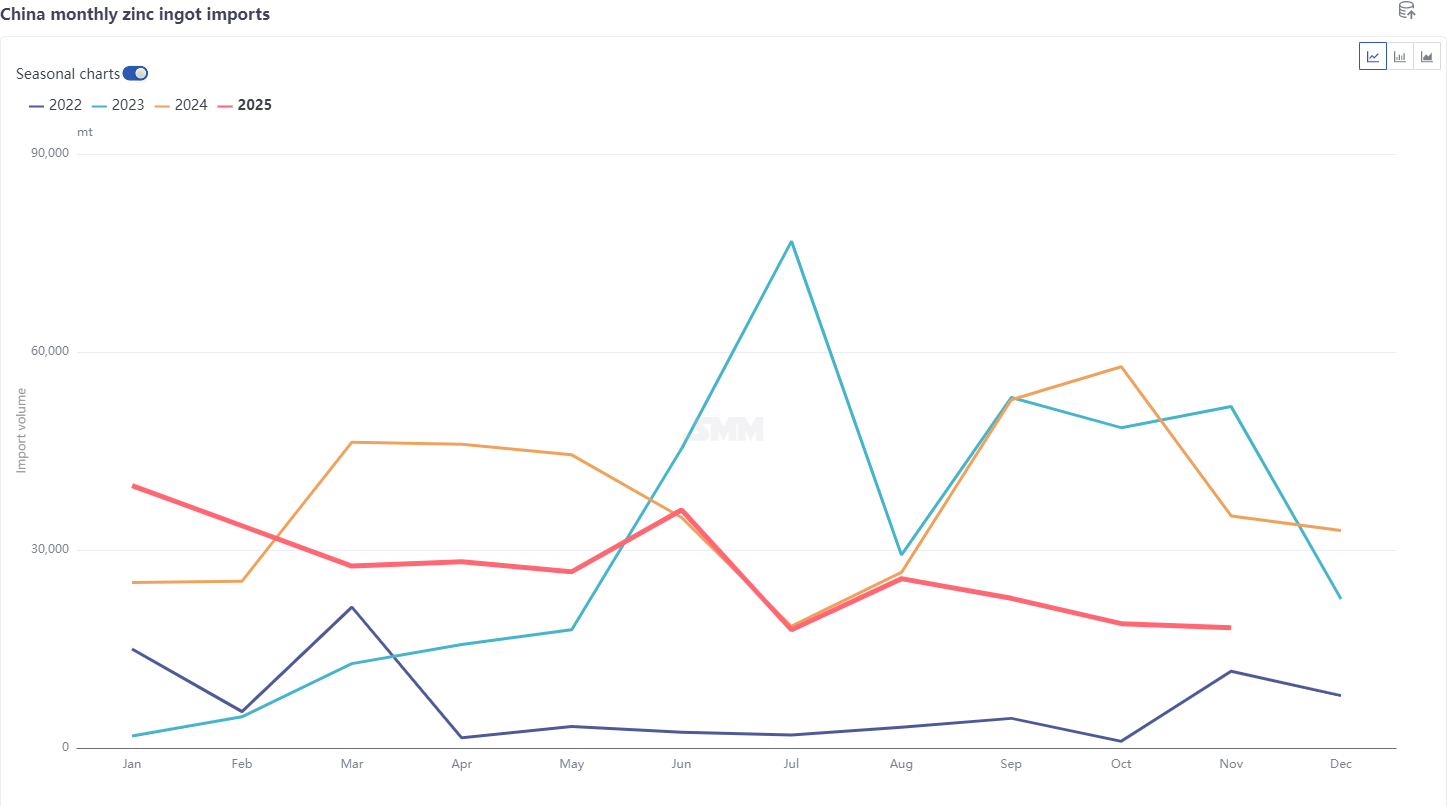

According to the latest customs data, China's refined zinc imports in November 2025 totaled 18,200 mt, down 600 mt or 3.22% MoM, and down 48.15% YoY. Imports from January to November amounted to 295,000 mt, a cumulative decrease of 28.46% YoY. Exports of refined zinc in November were 42,800 mt, resulting in a net export volume of 24,600 mt for the month.

By country, the top three sources of refined zinc imports in November were Kazakhstan (13,700 mt, 75.17%), Iran (3,600 mt, 19.75%), and Australia (400 mt, 2.31%). Imports from Iran increased due to barter trade, while overall imports from other sources declined. Refined zinc exports surged in November, with the top three destinations being Taiwan, China (18,100 mt, 42.37%), Singapore (14,500 mt, 33.87%), and Hong Kong, China (4,500 mt, 10.41%). Overall, the export window opened, with exports primarily shipped to delivery warehouses in Southeast Asia. Additionally, direct flows to downstream users in other Southeast Asian countries also contributed to the increase.

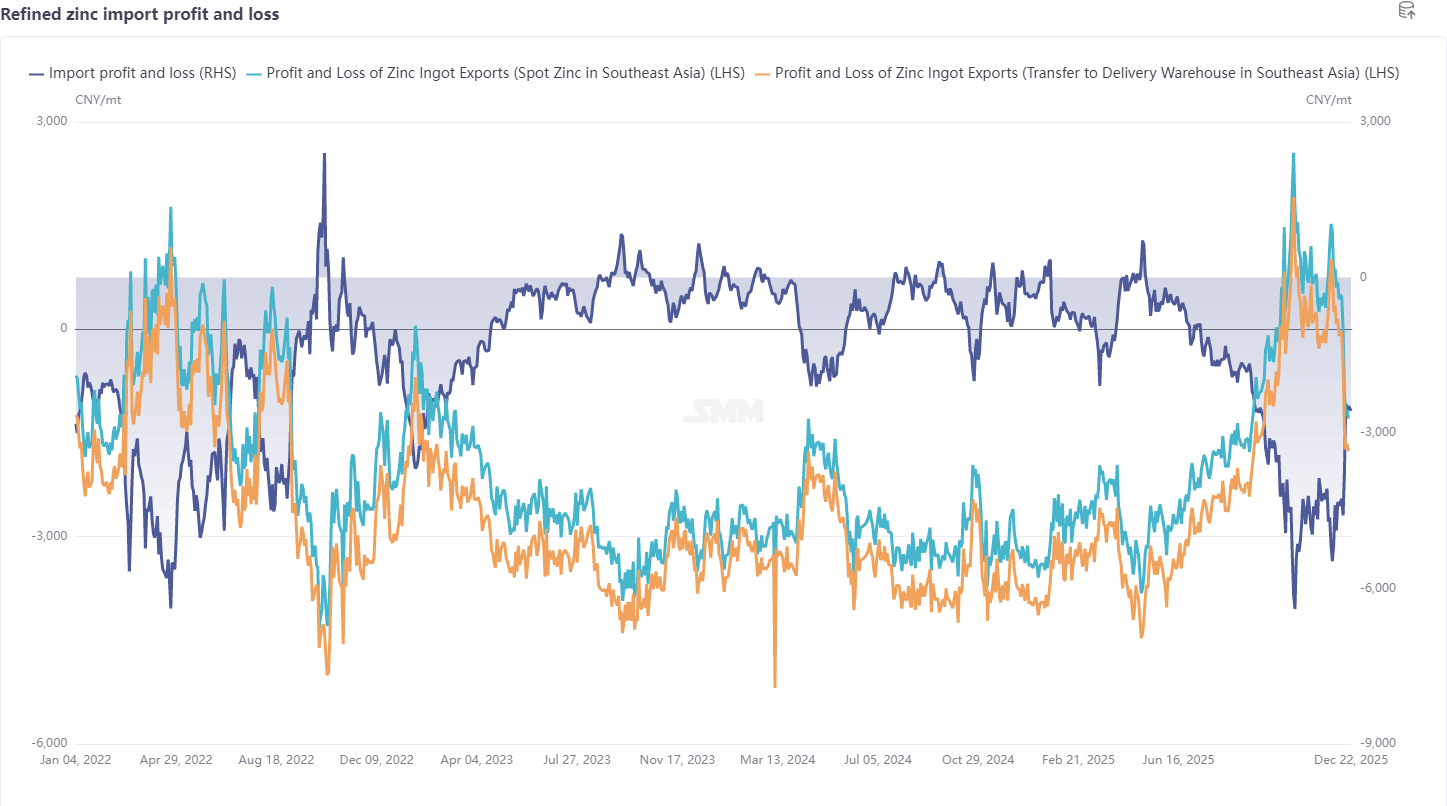

Entering December, the US Fed cut interest rates by 25 basis points as expected, but the latest employment and inflation data reduced the urgency for further rate cuts; the Bank of Japan raised interest rates by 25 basis points to 0.75%, bringing rates to their highest level in nearly 30 years. Domestically, the Central Economic Work Conference was held in December, calling for accelerated arrangements for the implementation of the 15th Five-Year Plan to ensure a good start and solid progress. On the fundamentals side, as domestic export volumes were gradually realized, coupled with the release of invisible inventory through deliveries, LME inventory increased significantly to around 100kt, and the large LME Cash-3M backwardation structure ended, with structural risks subsiding; domestic zinc concentrate TCs continued to decline to around 1,500 yuan/mt in metal content, and amid tight raw material supply, smelters increased production cuts and maintenance, leading to continuously declining production. Zinc ingot inventory continued to decrease. With the domestic market outperforming the overseas market, the SHFE/LME zinc price ratio corrected. Although imports of refined zinc remained at a loss of around 2,000 yuan/mt, the export window completely closed. In December, refined zinc imports are expected to remain at the volume under long-term contracts, while export volumes are projected to decrease to 10,000–20,000 mt.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.