SMM, December 22:

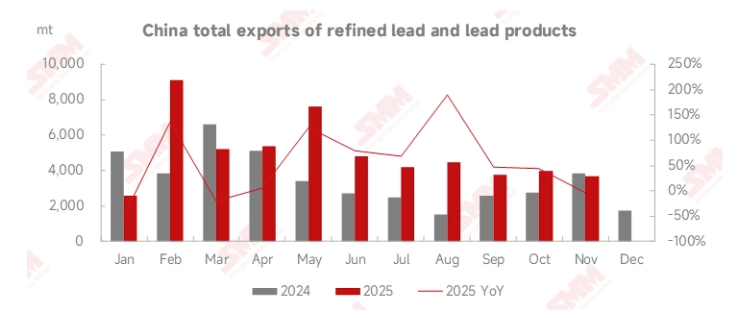

According to customs data, China's refined lead exports totaled 1,148 mt in November 2025, down 45.31% MoM and decreasing 45.6% YoY. From January to November, combined exports of refined lead and lead materials reached 54,832 mt, up 37.16% cumulatively YoY.

On the import side, China imported 8,656 mt of refined lead and 17,301 mt of lead alloy in November. From January to November, combined imports of refined lead and lead materials amounted to 166,226 mt, down 19.46% cumulatively YoY.

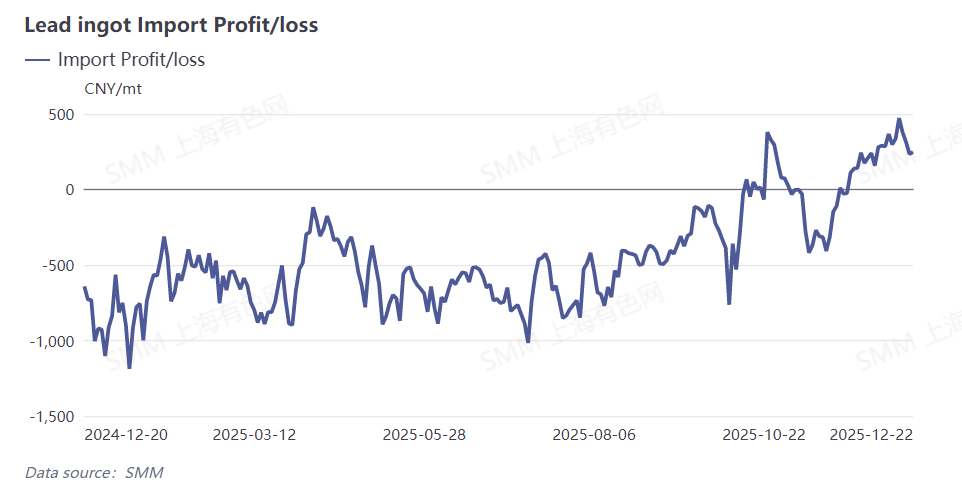

In early November, technically-driven funds pushed lead prices higher, with SHFE lead hitting a nearly 7-month high, boosting LME lead to a peak of $2,097/mt. In mid-to-late November, LME lead inventories surged sharply, overseas lead consumption underperformed compared to the domestic market, and macro sentiment turned bearish, causing LME lead to fluctuate downward.

Meanwhile, SHFE lead also returned to fundamentals, gradually falling below the 17,000 yuan/mt mark and hitting a low of 16,825 yuan/mt. During this period, the import profit margin for lead ingots turned from negative to positive, leading to inflows of crude lead from overseas into China. However, the lead ingots arriving in ports in November were mainly from previously concluded orders.

In December, domestic lead ingot supply tightened temporarily due to production cuts and halts at some smelters. However, downstream lead-acid battery producers showed weak procurement demand, which did not lead to a significant strengthening of lead prices. As a result, the enthusiasm for importing lead ingots remained low. Considering year-end factors, downstream battery producers are expected to take holidays during China's New Year's Day holiday, with limited demand for raw material restocking, leaving limited upside room for domestic lead prices. Additionally, some overseas countries are taking holidays for Christmas or New Year's Day celebrations on January 1, leading to tightened logistics and a decline in international trade activity. In summary, SMM expects combined imports of refined lead and lead materials in December to be lower than in November.