SMM December 19 News:

Key Points: This week, the solid-state battery sector showed vibrant activity with dense signals of industrialisation. Marked by Wanbang's 200 mt lithium sulphide production line about to start operations, upstream core electrolyte materials have entered a critical phase of mass production validation. Meanwhile, the oxide route, through QuantumScape and Ilika's customer breakthroughs and prototype deliveries, has demonstrated strong commercial momentum. On the downstream application side, from Dongfeng and FAW's strategic settlements to the real vehicle delivery of MG4 semi-solid state models, the industry chain is accelerating its move from "laboratory" to "production line," indicating that 2026 may become a year of differentiation in technology routes and market structures.

This week (December 12-18, 2025), industry dynamics show that solid-state batteries have moved beyond the long-term concept incubation stage and are entering a pre-industrialisation tipping point, driven by dual engines of "material mass production validation" and "vehicle application anchoring." The core industry conflict is shifting from "whether samples can be produced" to "whether stable, economical, and automotive-compliant large-scale production can be achieved." Upstream raw material prices maintained a slight downward trend, with key materials such as lithium sulphide, LATP, and LPSC all seeing price pullbacks, while shipments remained stable. Current demand mainly focuses on downstream validation and small-batch battery sample applications.

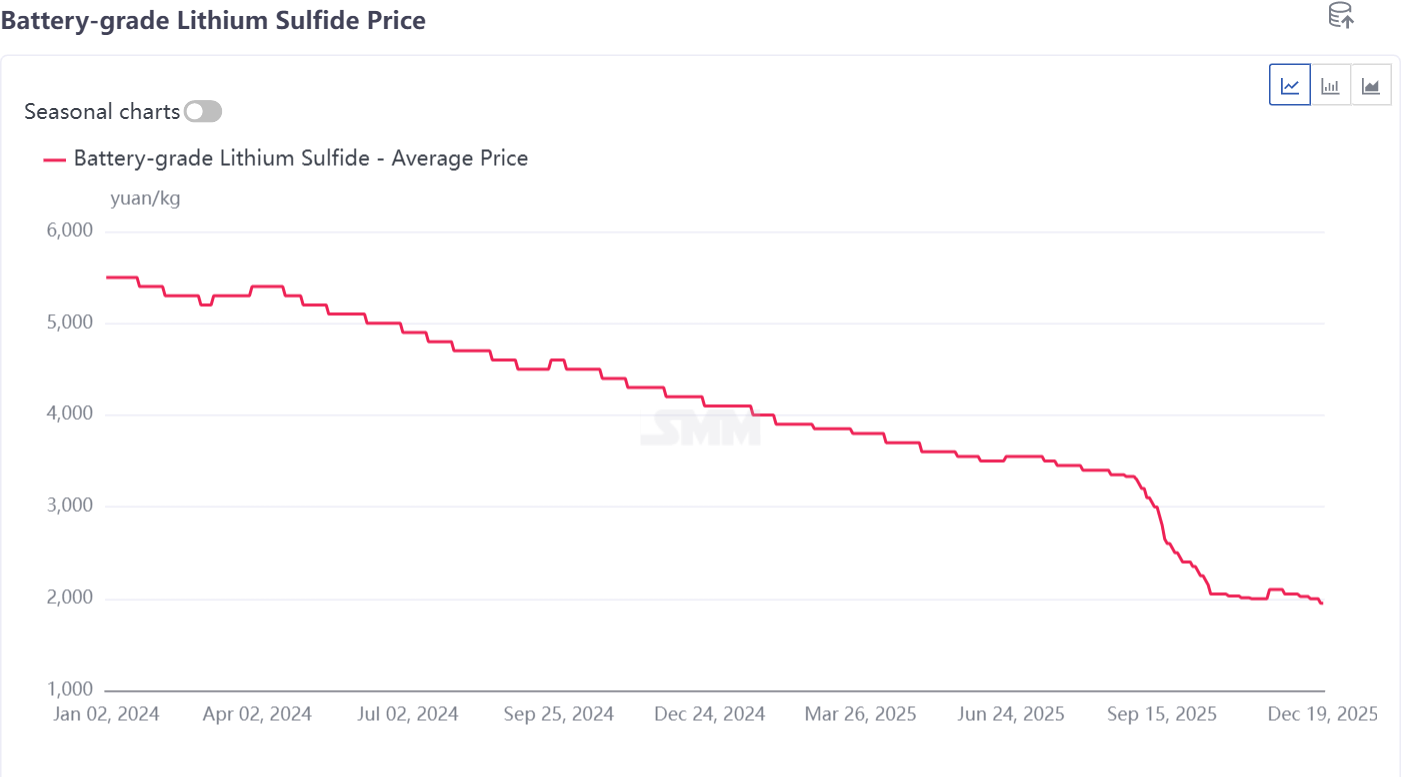

This week, lithium sulphide prices showed a steady decline, with high operating rates among lithium sulphide enterprises, and shipments were primarily in small orders, averaging 1,950 yuan/kg.

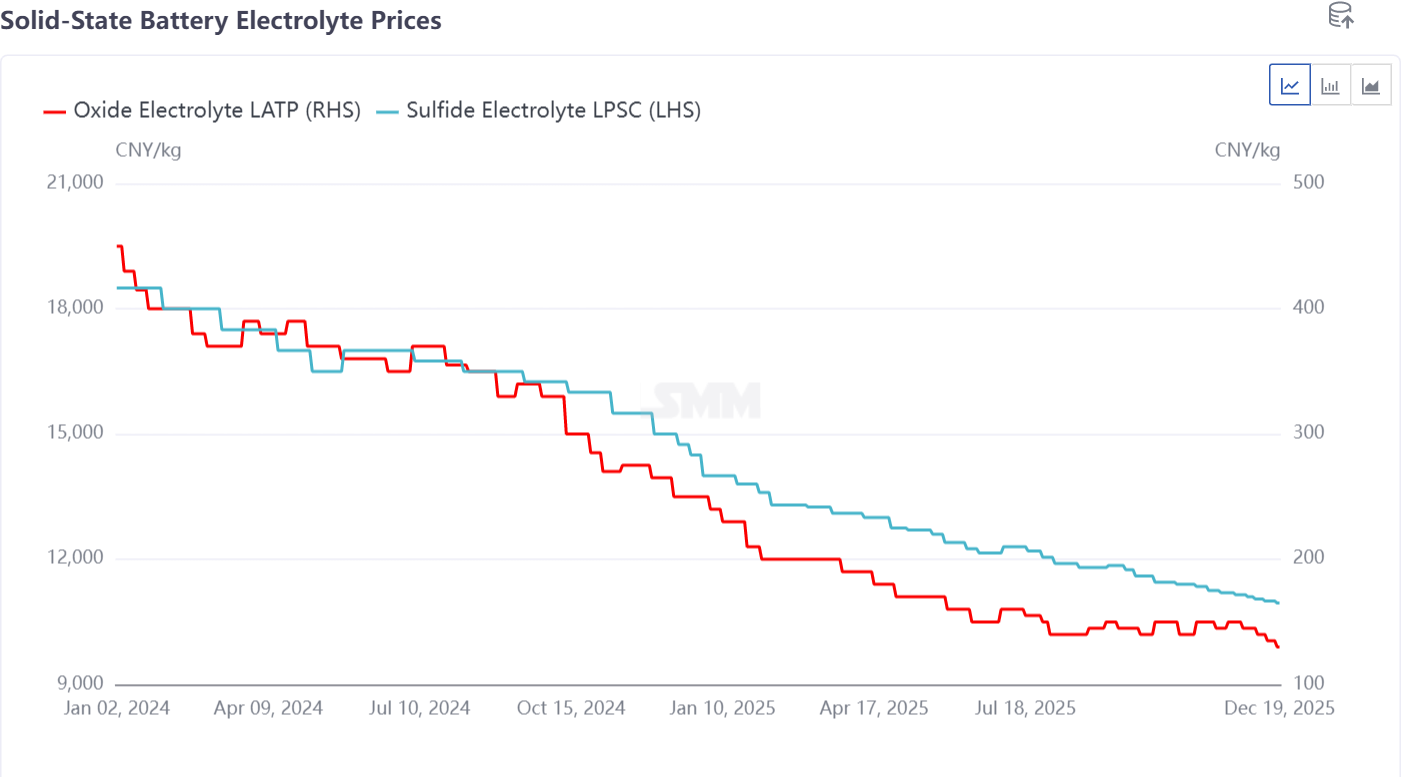

In terms of electrolytes, the price of sulphide electrolyte LPSC was 10,950 yuan/kg, while the oxide electrolyte was 130 yuan/kg, both showing varying degrees of decline.

I. Upstream Materials: Mass Production Capability Becomes the Core Competitive Factor, Sulphide and Oxide Routes Diverge

The most symbolic event this week was the substantial breakthrough at the front end of the industry chain, moving from "gram-level R&D" to "ton-level engineering," which is the fundamental prerequisite for cost reduction and volume expansion.

1. Sulphide Route: Domestic Industry Chain Closure Accelerates, but Cost and Consistency Challenges Enter Practical Testing

Key Breakthrough: Sichuan Wanbang's 200 mt/year battery-grade lithium sulphide demonstration line is about to start production. As the most critical and cost-intensive precursor for sulphide electrolytes, the scale-up supply of lithium sulphide is the "bottleneck" for the entire chain. This move suggests that the biggest cost reduction barrier for all-solid-state batteries using the sulphide route may be initially overcome.

Industry Significance: This is not an isolated event but resonates with the pilot layouts of Chengxin Lithium (Suining base), Wanrun Co., Ltd., Jinhé Industry, and others. They collectively point to a trend where companies with lithium and sulfur resource advantages are attempting to build a vertical integration advantage from ore to materials, establishing a long-term cost moat. However, Ganfeng LiEnergy (already producing 300 mt of electrolytes) has set a very high barrier for competitors with its first-mover advantage and progress in customer validation. In 2026, the actual production cost of lithium sulphide, product batch consistency, and certification feedback from downstream electrolyte enterprises will be the primary indicators for assessing the commercialisation progress of this route.

2. Oxide Route: Overseas Leaders Achieve Key Customer Ties, Leading in Engineering and Reliability Validation

Milestone: US-based QuantumScape (QS) announced a joint development agreement (JDA) with a top ten global automaker. This goes far beyond typical sample testing, indicating that its oxide solid-state lithium metal battery has gained strategic recognition from a top-tier customer in key performance areas, entering a deeper phase of co-development.

Industrialisation: UK-based Ilika shipped 10Ah Goliath prototype cells to automotive customers and completed 50Ah P2 cell samples, marking continuous and solid progress in scale-up capabilities for its oxide route. The overseas oxide path is steadily advancing along a clear commercialisation path of "prototype development → customer joint validation → capacity ramp-up," temporarily leading in engineering maturity and acquisition of high-end customers.

II. Midstream Sector: Manufacturing and Supply Chain, Specialized Division of Labor Initiated, New Demand for Equipment and Auxiliary Materials Under "Solid-State Definition"

Another indicator of industry maturity is the activation of specialized supply chains. Multiple events this week indicated that a new value chain is forming to meet the specific demands of solid-state batteries.

Specialized Equipment: Ouke Technology announced the completion of validation for its solid-state battery equipment, signifying that traditional lithium battery equipment systems have begun customized adaptations for unique solid-state processes (such as electrolyte layer preparation and high-pressure compaction). This is an indispensable step toward mass production.

Key Auxiliary Materials: Zhonglun New Materials launched BOPA film specifically for solid-state batteries, Yongtai Technology promoted lithium replenishing agents compatible with solid-state systems, and Jiangfan Guizhi raised funds to advance high-end silicon carbon anodes. These cases collectively indicate that solid-state batteries are not merely a simple upgrade to existing liquid lithium battery systems but are driving a comprehensive overhaul of the material system—from adhesives and conductive agents to packaging materials. Enterprises that can proactively define and meet these new demands will secure a core position in the future supply chain.

III. Downstream Applications: Automakers' Strategic Paths Diverge, Dual-Track System of "Semi-Solid Transition" and "All-Solid-State High-End" Established

The strategic choices of automakers have provided clear demand traction and a implementation timetable for this round of industrialization, and the path forward has become clear.

Semi-Solid (Solid-Liquid Hybrid) as a "Definitive Transition Solution" has been successfully commercialized: The delivery of the SAIC MG4 Semi-Solid Anxin Edition, particularly its claimed excellent low-temperature performance, has tangibly demonstrated to the market the immediate value of hybrid electrolyte technology in enhancing safety and alleviating low-temperature anxiety. This offers a clear technical option for the mid-to-high-end EV market from 2024 to 2026.

All-Solid-State Batteries Anchor "High-End Flagship and Performance Revolution": Plans from FAW Hongqi (to be equipped in 2027) and Bugatti (in collaboration with Rimac, targeting 2030) clearly define the initial positioning of all-solid-state batteries—not for ordinary economy models, but as the "technical crown" defining the next generation of luxury and ultra-high-performance car models. This determines their high initial cost tolerance but also imposes extremely stringent requirements for energy density, power density, and absolute safety. IV. Accelerated Collaboration: Capital and R&D Models, Deepening Integration of Industry and Finance, Joint R&D Becoming the Mainstream Paradigm

This week, from Jiangfan Guizhi completing nearly 100 million yuan in Pre-A round financing to Sunwoda establishing joint laboratories with Shenzhen Institute of Technology and Jinhe Industrial with Anhui University, two major industry trends are reflected: 1) Capital markets continue to increase their focus on technology unicorns in the solid-state battery segment; 2) Faced with extremely high technical complexity, the deeply integrated R&D model of "enterprise-led, university-collaborated, and capital-boosted" has become the most effective paradigm for breaking through core material and process bottlenecks.

V. Policy Promotion: National Subsidies + Solid-State Battery Evaluation

This week, progress on solid-state batteries from national teams emerged, with products submitted by various companies meeting expectations. A major power that manually calculated to build an atomic bomb in difficult times, with its determination in carbon emissions reduction, combined with strong technological iteration capabilities in the industrialisation of traditional lithium batteries for new energy, is bound to ride the waves in solid-state batteries as well.

SMM believes that the industry is currently entering a critical verification period of "separating the genuine from the fake," and 2026 may be a key year for the solid-state battery industry to solidify its foundation and find a way forward. Particularly in the "separating the genuine from the fake" aspects of raw materials, materials, and process links, it is a critical verification year. National subsidies may continue to increase, lower entry barriers for enterprises, optimise the competition system, and establish a multi-route, multi-level horse racing mechanism, with each participating team forming deep bonds, sharing information, and working together to achieve breakthroughs.

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!

![Breaking the Hormz Strait Curse for Sulfur Self-Rescue: Hubei Yihua Signs 1,000kt Phosphogypsum-to-Sulphuric Acid Project [SMM Analysis]](https://imgqn.smm.cn/usercenter/zWZVI20251217171730.jpg)