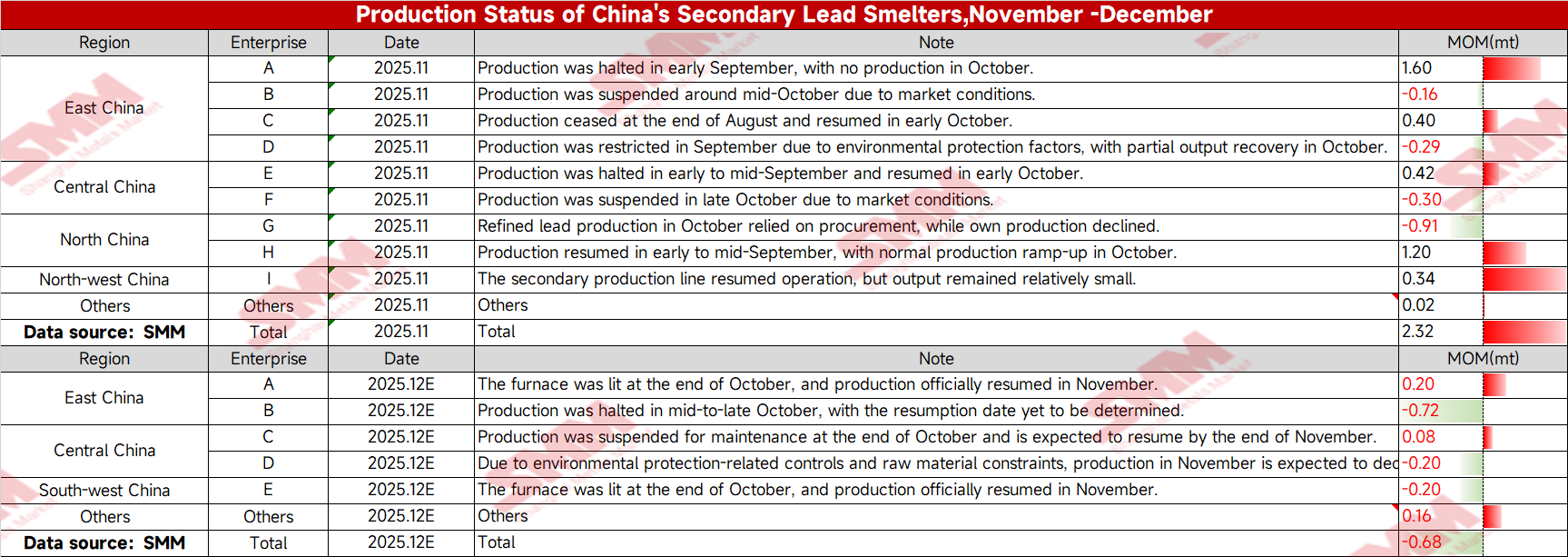

Several new secondary lead projects were commissioned in 2025. From January to November, cumulative production of secondary crude lead reached 3.609 million mt, up 4% YoY. However, losses in secondary refined lead smelting dampened production enthusiasm, with some smelters opting to sell crude lead directly. Cumulative secondary refined lead production from January to November 2025 was 2.886 million mt, down 1.4% YoY. In November 2025, multiple smelters resumed production, leading to a significant increase in secondary lead output to 373,000 mt, up 7.78% MoM and 16.83% YoY. Secondary refined lead production reached 296,000 mt, up 8.5% MoM and 10.13% YoY. The chart below details the production schedules of secondary lead smelters for November-December.

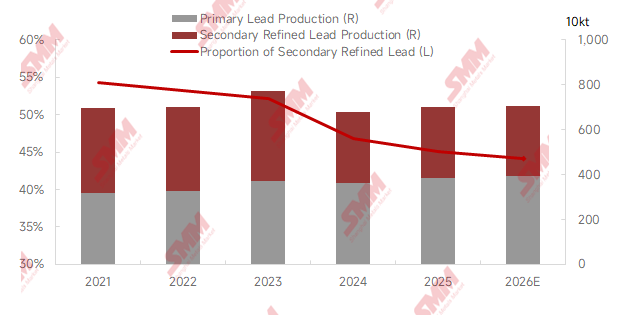

Looking ahead to 2026, secondary refined lead production is expected to decline by 1.5% YoY. The secondary lead sector faces severe overcapacity, and supply-demand imbalances in raw materials are causing operational losses, forcing secondary lead smelters to transform.

Data Source Statement: The data is processed by SMM based on publicly available information, market exchanges, and internal database models, and is for reference only.

SMM expects more secondary lead smelters to transition to an integrated raw material smelting model in 2026, combining lead concentrates, waste lead-acid batteries, and other lead-containing scrap to maximize by-product revenue. Equipment upgrades and commissioning will then impact normal production. Additionally, some companies plan to add electrolysis lines, converting crude lead output into primary lead rather than secondary refined lead. Furthermore, supply-side structural reforms advocate for capacity optimization. Amid policy and industry trends, some secondary lead capacity is expected to be phased out, with total capacity projected to fall below 8.5 million mt by 2030.