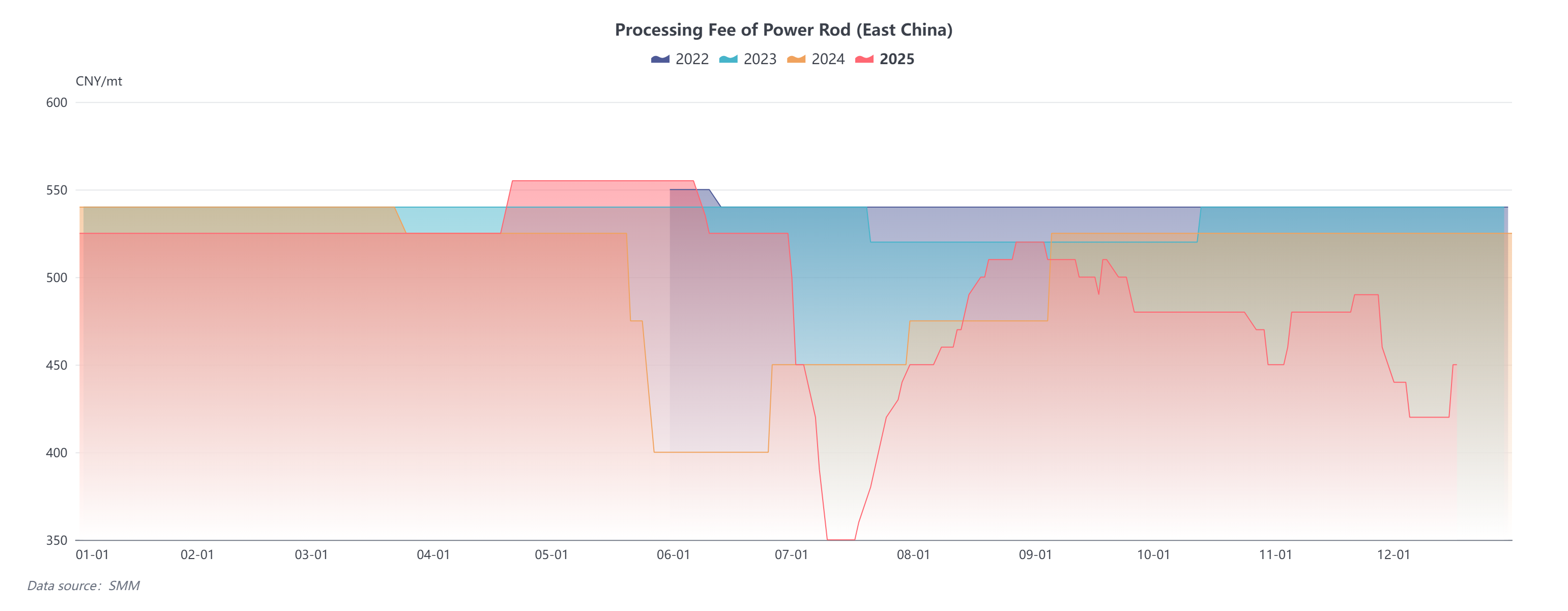

Amid the dual pressures of capacity expansion and weak demand in the copper cathode rod industry, the oversupply situation has become increasingly prominent, with industry competition intensifying and significant divergence in market processing fees. According to SMM, the average processing fee for 8mm power rods in east China in December 2025 was 430 yuan/mt, while traders' processing fee quotations even turned negative, with the price spread between copper cathode rod producers and traders widening to 500-600 yuan/mt at one point. This extreme price difference not only reflects the supply-demand imbalance in the industry but also highlights the fundamental differences in profit models between copper cathode rod producers and traders. The following analysis will explore the causes of the processing fee spread, break down the core profit logic of traders, and outline the future competitive direction of the industry.

I. Core Causes of the Widening Processing Fee Spread in the Copper Cathode Rod Market

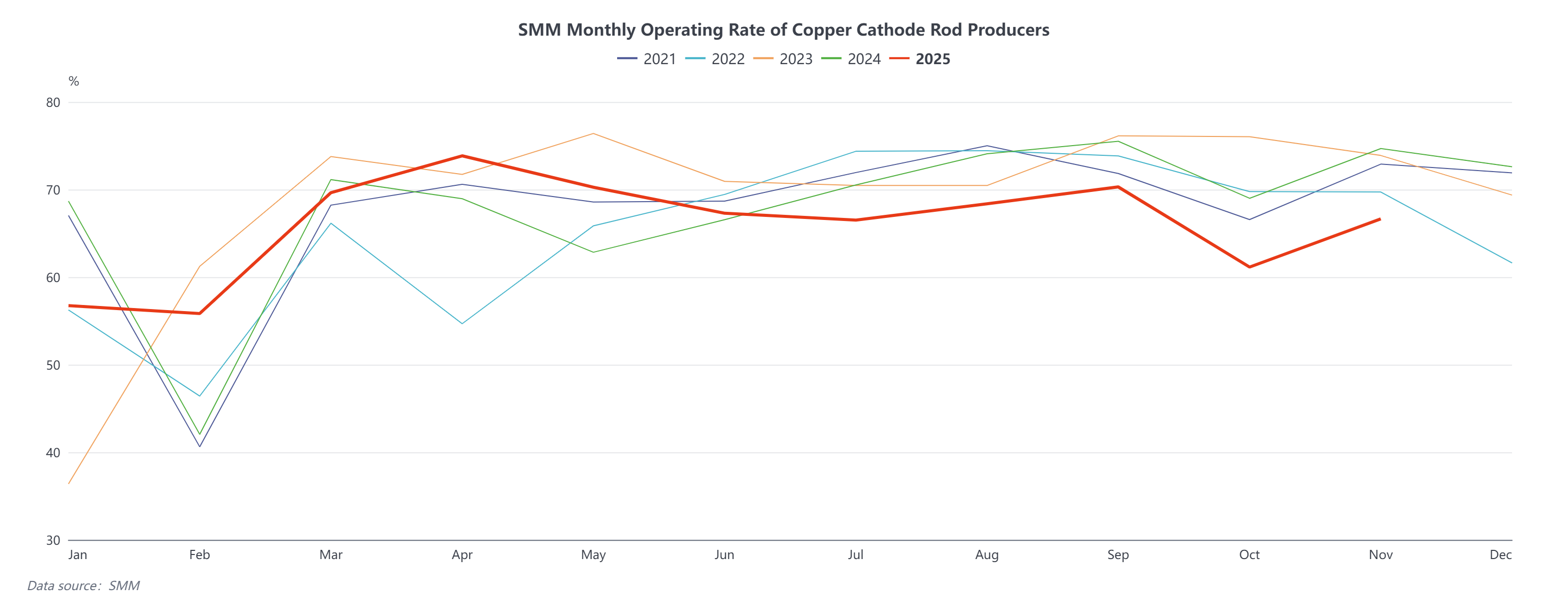

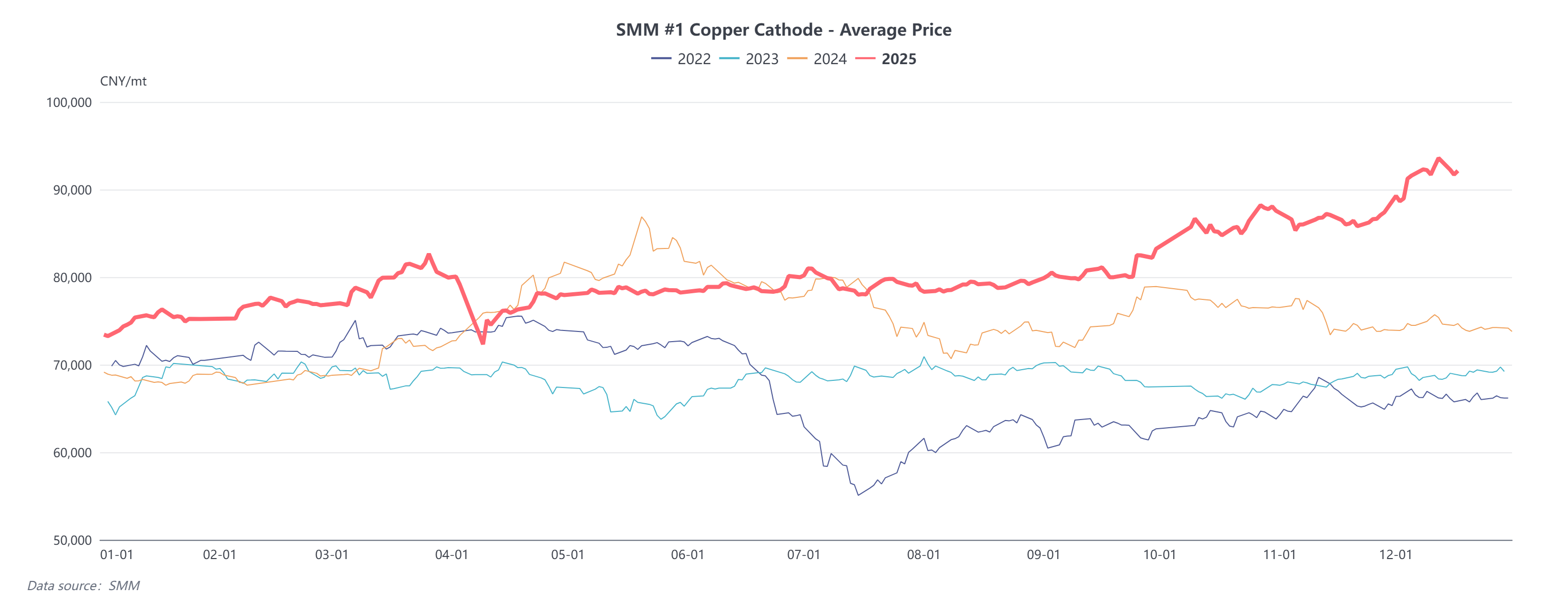

In recent years, copper cathode rod capacity has continued to expand, while downstream demand from the construction sector has been weak due to the property market downturn, and demand growth in the power industry slowed in H2. Overall demand growth has lagged behind the pace of capacity expansion, leading to a decline in capacity utilization. The operating rate for copper cathode rods in November was only 66.65%, up 5.49 percentage points MoM but down 8.03 percentage points YoY.The operating rate for December is expected to decrease by 1.58 percentage points MoM to 65.07%, down 7.53 percentage points YoY. To compete for limited market share, enterprises have engaged in fierce involution in processing fees. Additionally, copper prices remained above 90,000 yuan/mt in December, causing a sharp increase in downstream procurement costs. Demand from wire and cable enterprises was further suppressed, while their sensitivity to processing fees increased significantly, leading to notable "low processing fee order grabbing" in the copper cathode rod industry.

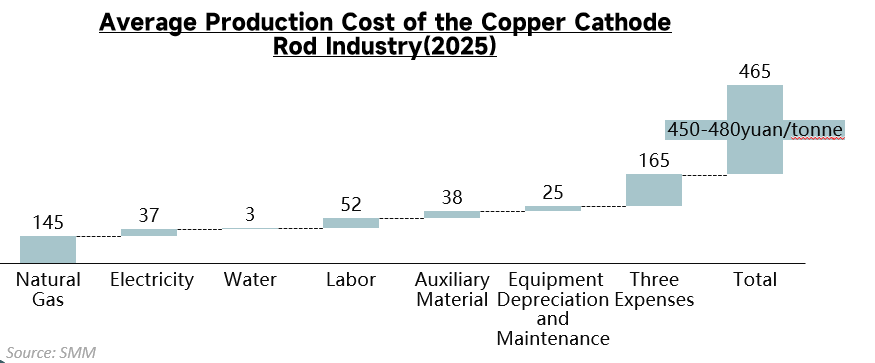

However, copper cathode rod producers need to cover fixed production costs such as equipment depreciation, labour, and energy consumption. Most enterprises still require processing fees to cover fixed costs to ensure basic profitability. In contrast, traders' costs are mainly concentrated in spot procurement capital occupation, logistics and storage, and financial instrument fees. With faster capital turnover and the ability to further reduce costs through economies of scale, traders have a cost structure that allows for significantly lower processing fees than rod producers. Traders quoting "negative processing fees" are not operating at a loss but offset the loss through a diversified profit system.

II. Core Profit Logic Behind "Negative RC/TC"

First, traders can capitalize on copper price fluctuations by buying low and selling high. They stockpile when copper prices are low and actively sell when futures prices exceed spot prices; conversely, they hold inventory awaiting price increases. After copper prices break through highs, even with negative RC/TC, they can realize gains from the price spread through subsequent copper price increases. Second, to hedge against the risk of price pullbacks, they purchase put options while selling; if prices pull back, option gains can offset some spot losses; if prices continue to rise, they retain profit potential.

Second, against the backdrop of increasingly involutionary RC/TC, futures tools are traders' core profit strategy. When accepting spot orders, traders establish hedging positions in the futures market against spot market exposure. Whether copper prices rise or fall, they can offset spot and futures gains and losses, ultimately ensuring basic profits through the spot-futures price spread. For copper rod plants, only large enterprises can engage in hedging and the aforementioned low-price stockpiling, while small and medium-sized enterprises, constrained by cost pressure, seldom use futures tools for profit. Meanwhile, traders can simultaneously conduct arbitrage to lock in profits. For example, under the current SHFE copper contango structure, if they anticipate the price spread will narrow, they can execute positive arbitrage; conversely, they can profit from reverse arbitrage.

Finally, aggregating scattered demand to achieve economies of scale wins. According to SMM, downstream enterprises primarily cooperate with traders through "spot order purchases." Traders can attract a large volume of scattered orders with "low RC/TC," achieving concentrated scale benefits to dilute logistics and transportation costs and expand profit margins.

III. Nature of Industry Competition and Future Development Direction

Overall, the reasons for the current market pressure on RC/TC and widening price spreads are weak consumption demand on one hand, and the disparity in profit models between copper cathode rod manufacturers and traders on the other. In reality, the essence of competition in the current copper cathode rod industry, whether for manufacturers or traders, has gradually evolved from superficial contention over "RC/TC levels" to a deeper contest of "superiority of profit models".

For traders, it is essential to further leverage financial instruments and capital efficiency to break away from reliance on RC/TC. For manufacturers, the key to breaking the deadlock lies in leveraging production-side advantages, such as optimizing production equipment through technological innovation to reduce costs, and creating high-value-added, high-end products to tap into the high-end market. At the same time, they should also utilize financial instruments to unlock profit opportunities in the futures market. Looking ahead, the traditional profit model of relying on RC/TC in the copper cathode rod industry is no longer sustainable. Only by escaping the involution of RC/TC and building diversified, high-barrier profit models can companies gain the initiative in the current oversupplied market.