SMM News, December 17:

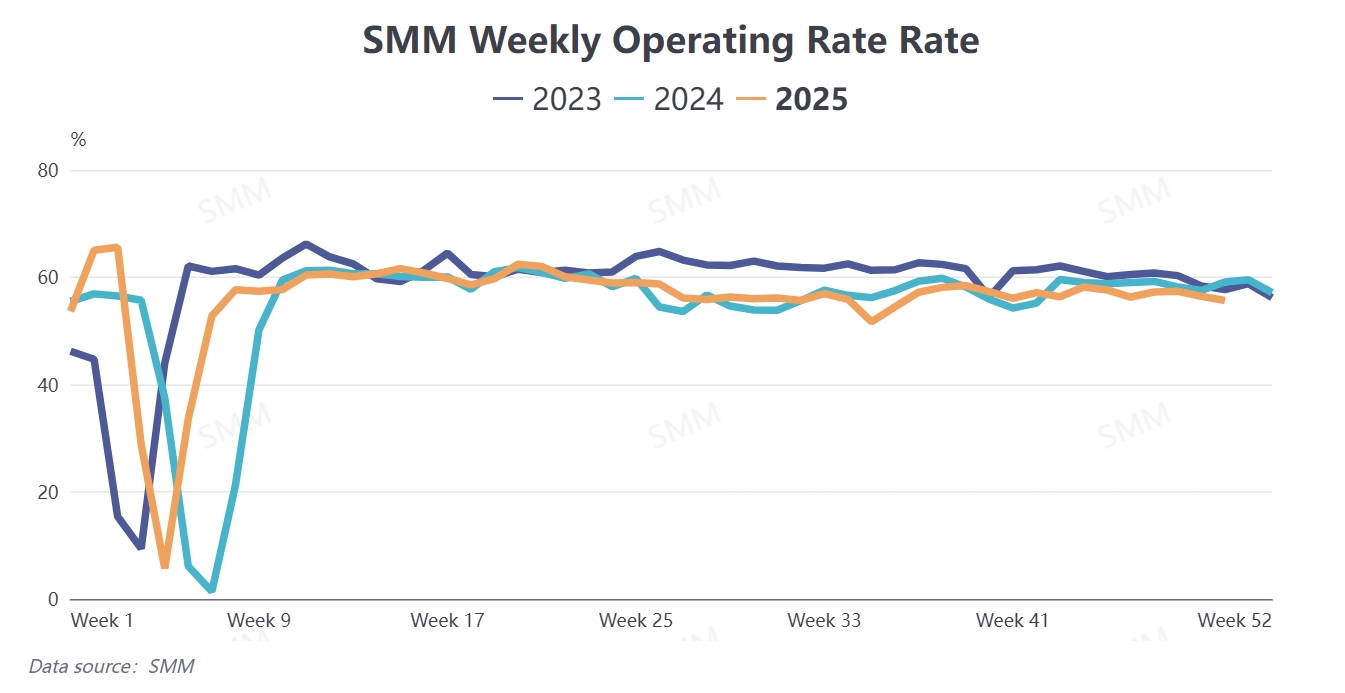

According to SMM communications and research, China's zinc oxide operating rate recorded 48.34% in November, up 0.18 percentage points MoM, but down 0.14 percentage points YoY. After entering December, based on the weekly operating rate, the zinc oxide operating rate has also continued to weaken. What are the reasons behind this? How will the zinc oxide market develop going forward?

Based on recent market feedback and information obtained by SMM, the recent decline in zinc oxide operating rates is primarily attributed to two factors.

Firstly, some enterprises in the north are still affected by environmental protection inspections, leading to production halts.

Secondly, terminal demand has weakened. Recent market feedback indicates that orders for both semi-steel and all-steel tires have softened, with a noticeable inventory buildup at end-user tire factories. Meanwhile, the ceramic market is also facing production cuts or suspensions at ceramic plants, coupled with continuously weakening demand.

From the perspective of the rubber-grade zinc oxide market, which accounts for over half of downstream consumption, the short-term market is experiencing weak demand. In the long term, however, demand from end-user tire factories for rubber-grade zinc oxide presents both opportunities and challenges.

So, where do these opportunities and challenges come from?

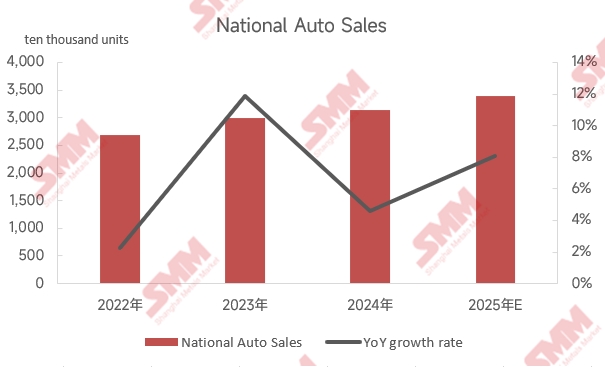

First, from the opportunity perspective, the consumption of rubber-grade zinc oxide is heavily concentrated in the tire sector. China's auto sales have shown remarkable performance over the past three years, increasing from 30.04 million units in 2023 to 31.43 million units in 2024, up 4.63% YoY. Domestic auto sales are projected to reach 33.97 million units in 2025, with an estimated YoY growth of around 8.08%. Although some regions phased out or adjusted the "trade-in" subsidies ahead of schedule by the end of 2025, the automotive market is still expected to present certain opportunities in 2026. In September this year, China released the "Automotive Industry Growth Stabilization Work Plan (2025–2026)," which explicitly states that the industry will maintain stable and positive development trends in 2026. Additionally, the plan outlines detailed measures such as the NEV promotion campaign in rural areas and pilot projects to improve charging and battery swapping infrastructure in county-level regions. These initiatives are expected to continue supporting the auto market, which will directly impact the overall production and sales of tires in China.

Challenges primarily stemmed from the subsequent export of China's tires.

Two investigations related to the European Union impacted the domestic tire market in 2025.

On May 21, 2025, the European Commission initiated an anti-dumping investigation into new pneumatic rubber tires for cars and light trucks originating from China, in response to complaints from the EU tire industry that Chinese dumping practices were harming their interests. On November 6, 2025, the European Commission announced that, following an application submitted by the Coalition Against Unfair Tyre Imports on September 22, 2025, it had launched a countervailing duty investigation into new pneumatic rubber tires for cars and light trucks originating from China.

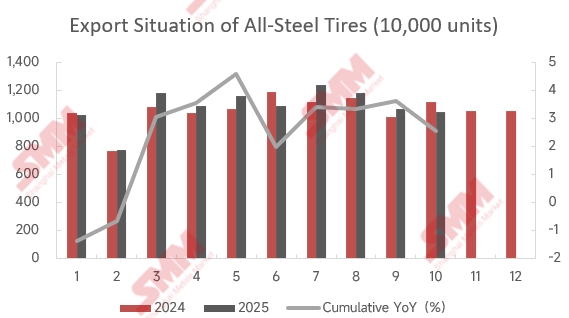

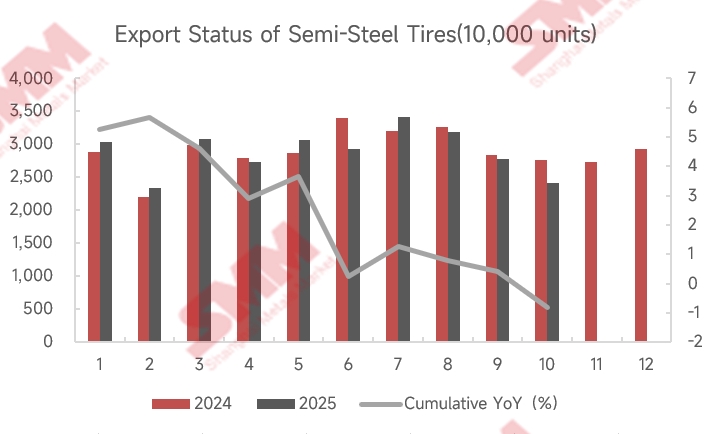

From the perspective of this year's exports of truck and bus radial (TBR) tires and passenger car radial (PCR) tires, as of October, China's cumulative exports of TBR tires reached 108.26 million units, while cumulative exports of PCR tires reached 289.79 million units, with YoY growth rates of 2.56% and -0.82%, respectively. PCR tire exports showed some weakness compared to the previous year.

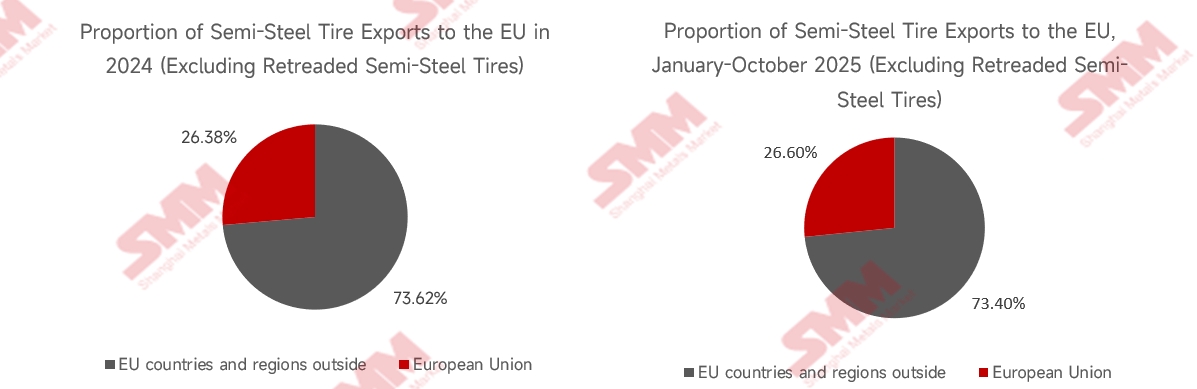

According to customs data, 26.38% of the semi-steel tires exported by China in 2024 were shipped to the European Union region. From January to October 2025, domestic exports of semi-steel tires to the EU reached 76.68 million units, with the proportion rising again to over 26%, reaching 26.6%.

Meanwhile, starting from July 2025, the EU implemented mandatory customs registration for new pneumatic rubber tires imported from China, which will last for nine months, casting a pessimistic outlook on the export prospects of China's semi-steel tires. Currently, the EU's anti-dumping and countervailing investigations into China's semi-steel tires have not yet announced final rulings, and the cases remain under investigation, but both are expected to be completed by the end of 2026. If tire exports face obstacles in the future, it will have a certain impact on the domestic demand for zinc oxide and deal a blow to small and medium-sized enterprises that primarily rely on export orders.