In 2025, the global nickel pig iron (NPI) market, influenced by the interplay of supply-demand dynamics, cost fluctuations, and policy environment, exhibited an overall trend of "fluctuations in the first half of the year, followed by initial stability and subsequent weakness in the second half." Significant divergence was observed between the two core production regions, China and Indonesia. Price trends shifted from cost-supported increases at the beginning of the year to off-season demand-driven declines by year-end. Throughout the year, the industry revolved around two fundamental themes: "capacity release and cost constraints on the supply side, and volatility in the stainless steel industry on the demand side."

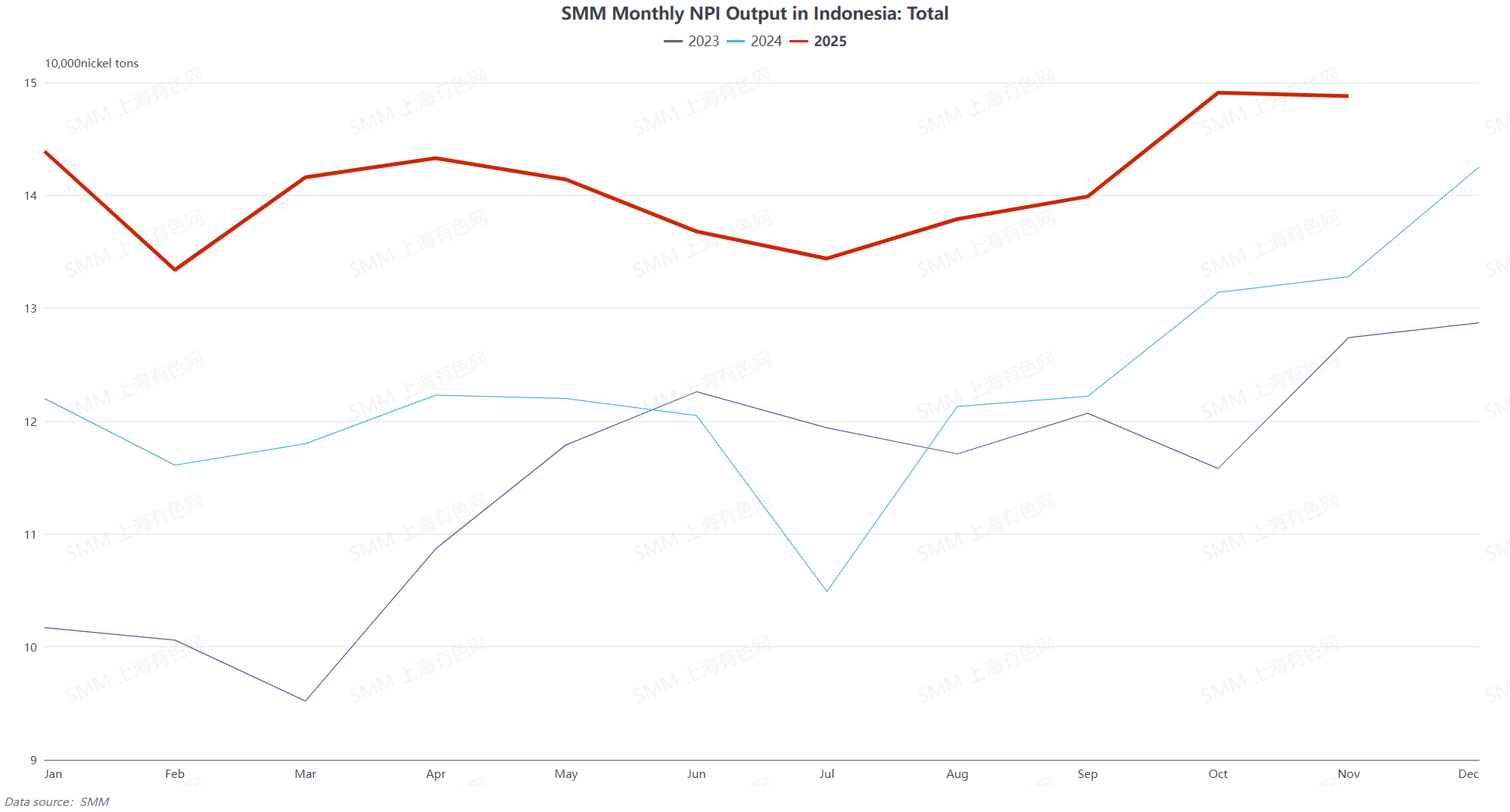

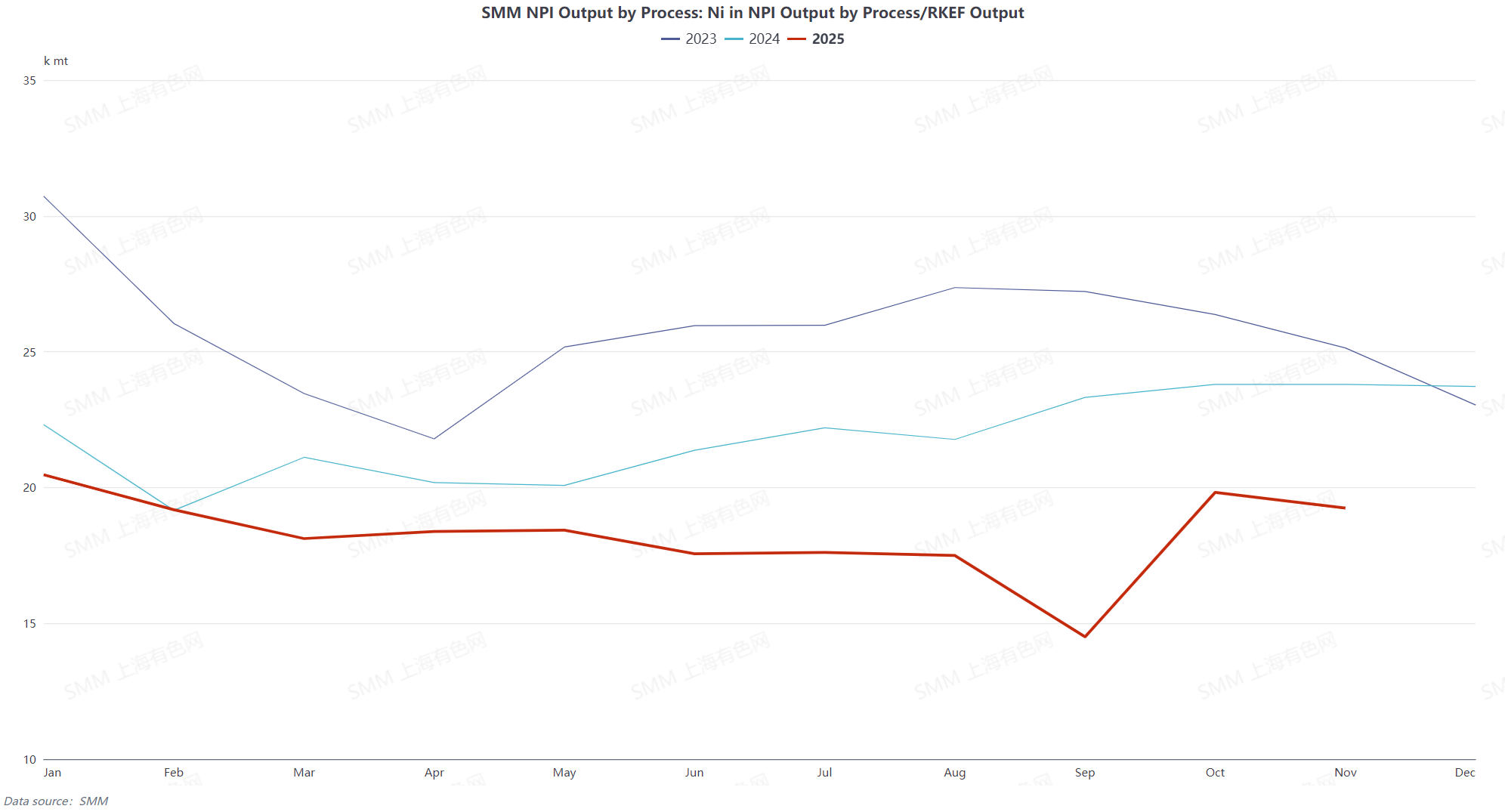

Supply side, global NPI production maintained YoY growth but with prominent regional divergence. Indonesia, leveraging the continuous release of new capacity and advantages in raw material supply, remained the core source of incremental output, with full-year production up 15.08% YoY. New capacity was concentrated in areas such as Obi Island and Halmahera. Overall, in H1, Indonesia was affected by the rainy season and slow RKAB quota approvals, leading to tight nickel ore supply which pushed up costs. NPI metal content fluctuated MoM from January to June, with some smelters operating at low rates due to losses. After July, as the rainy season subsided and quotas were secured, nickel ore prices pulled back, alleviating cost pressure. In H2, with the arrival of the peak consumption season, NPI physical content and metal content rebounded MoM from August to October. Smelter profitability improved, coupled with new capacity releases, leading to steady production growth. Entering the traditional off-season in November-December, stainless steel demand decreased and inventories remained high, putting NPI prices under pressure. Some smelters conducted maintenance and implemented production cuts, resulting in a marginal decline in output.

Domestic supply in China remained under persistent pressure except for improvements during the peak season. In 2025, the Chinese NPI market showed a trend of "fluctuating downward throughout the year with ongoing supply-demand tug-of-war." Full-year high-grade NPI production was down 19.31% YoY. In H1, affected by the rainy season in the Philippines, tight nickel ore supply pushed up raw material costs. Coupled with low NPI product prices, smelters generally faced losses. Production declined MoM for two consecutive months in January-February. Although there was a slight recovery from March to May due to the end of maintenance at some smelters and a recovery in stainless steel demand, production fell significantly again in June as product prices dropped to the year's low. In H2, high-grade NPI continued to operate at low rates in July due to losses. From August to October, benefiting from the peak consumption season, production resumptions at enterprises, and steady growth in stainless steel demand, production staged a rebound. Entering the traditional off-season in November-December, end-use demand was weak, NPI prices hit a five-year low, and persistent cost pressure led to increased production cuts and maintenance at smelters, resulting in consecutive monthly production declines. The core market contradiction throughout the year centered on the tug-of-war between high raw material costs and weak downstream demand. Environmental protection policies and adjustments to stainless steel production schedules further exacerbated production volatility, keeping overall industry profitability under pressure.

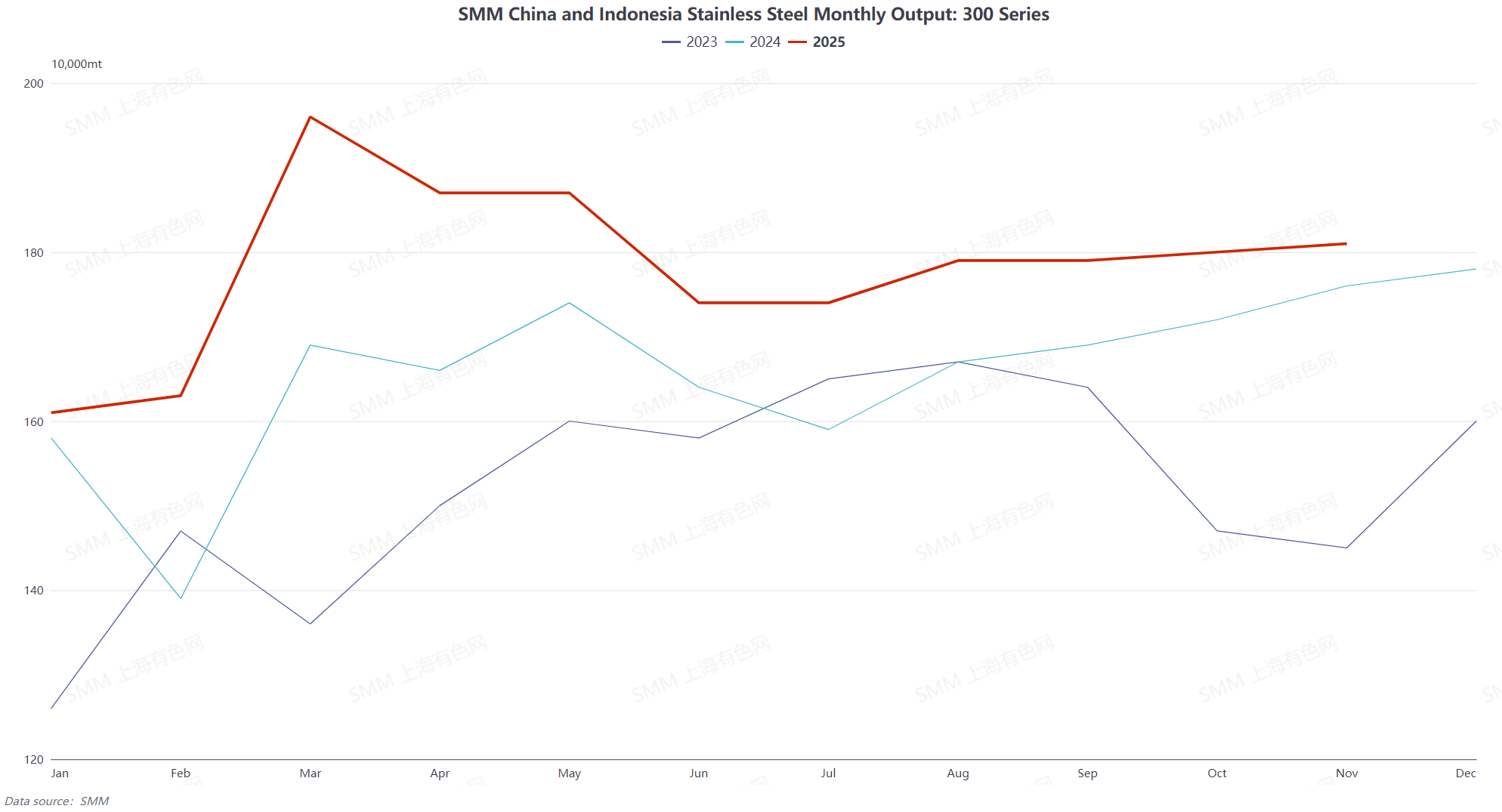

On the demand side, as the core downstream of NPI, 300-series stainless steel production increased by 7.48% YoY for the full year, but demand showed significant phased fluctuations. In H1, the Q1 "March peak season" materialized, with stainless steel demand recovering after the Chinese New Year. Disruptions in raw material supply pushed up spot prices, and expanded steel mill profits boosted production scheduling enthusiasm. In Q2, impacted by the mid-April U.S.-China tariff storm, stainless steel futures and spot prices fell sharply. Continuous losses at steel mills, coupled with the arrival of the traditional consumption off-season, led to noticeable social inventory buildup, slowing production growth, and phased soft demand. In H2, the Q3 "September peak season" began, with stainless steel production increasing MoM, correspondingly raising procurement demand for high-grade NPI and briefly supporting a rebound in NPI demand. After November in Q4, entering the traditional off-season, weak end-use consumption caused continuous declines in finished stainless steel prices and difficult destocking. Multiple stainless steel enterprises initiated production cut plans, with simultaneous contractions in 300-series and 200-series production. The better economics of stainless steel scrap further squeezed demand, weakening NPI buying interest and reducing demand-side support.

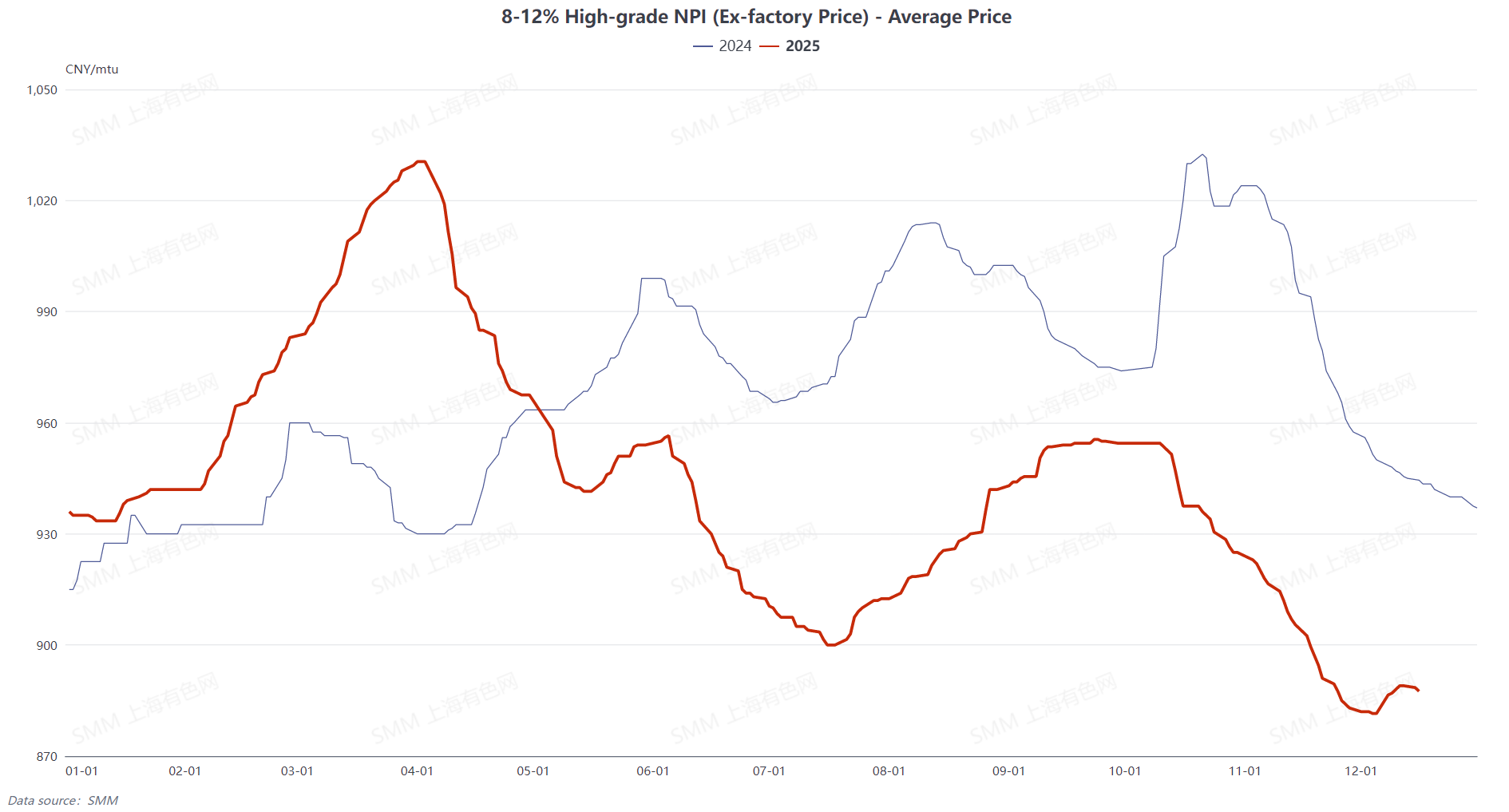

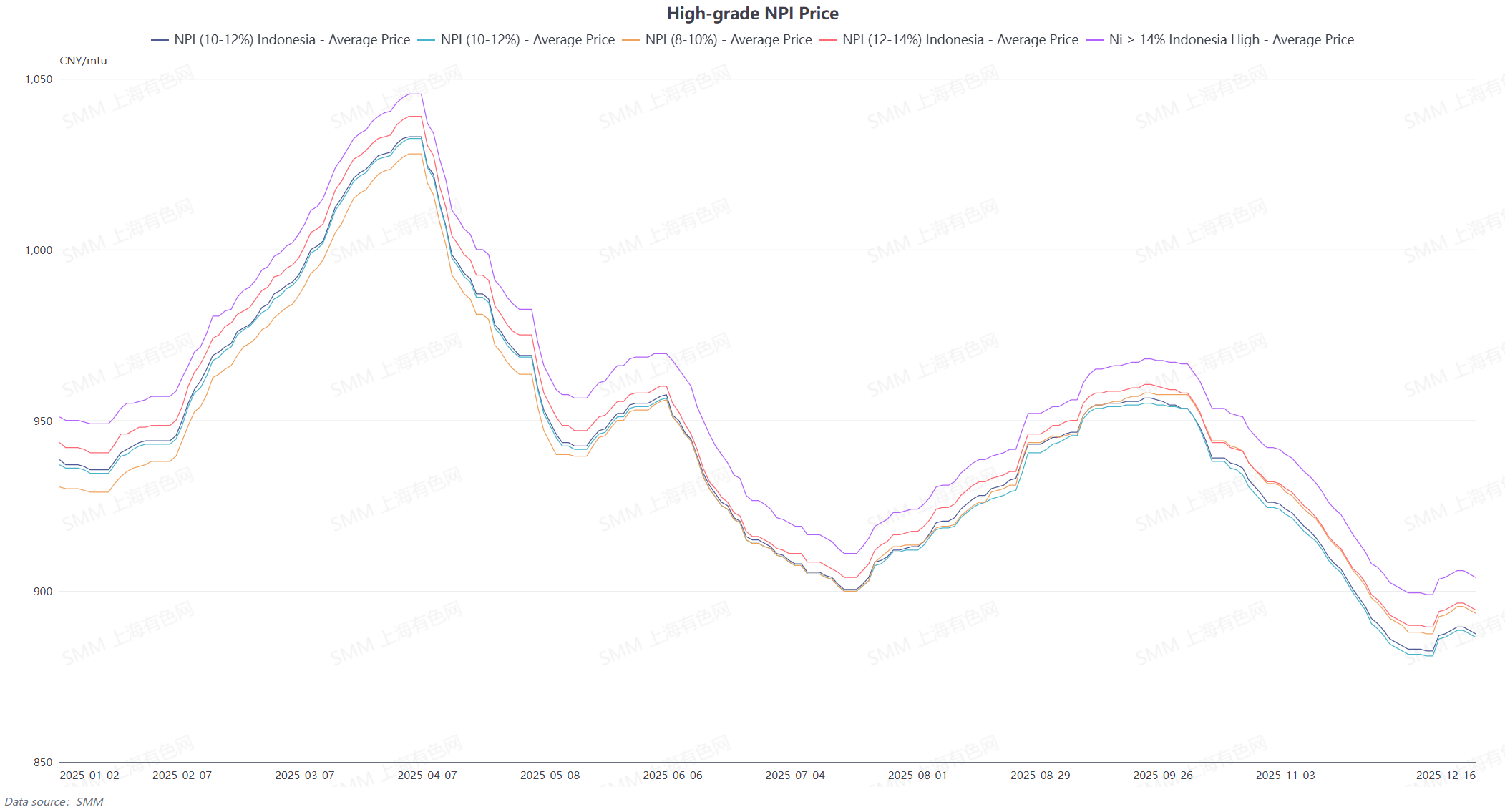

Price-wise, high-grade NPI movements were highly linked to supply-demand fundamentals, showing an "N"-shaped fluctuation pattern: rising in Q1, correcting in Q2, stabilizing in Q3, and falling sharply in Q4. In Q1, supported by recovering stainless steel demand and short-term supply contraction in Indonesia, the average price of 10-12% Indonesian high-grade NPI (delivered port, duty-paid) rose from a low of 935.5 yuan/mtu (delivered port, duty-paid) to 1,033 yuan/mtu, a gain of 10.42%. In Q2, escalated U.S.-China tariffs triggered negative feedback in the stainless steel market, causing high-grade NPI prices to fluctuate downward from highs, with a cumulative drop of 11.62% within the quarter. In Q3, both supply and demand sides provided support during the traditional peak season, keeping prices hovering at highs. In Q4, demand collapsed and prices fell below the cost support line, hitting a five-year low in November, with a slight stabilization near year-end relying on the cost floor.

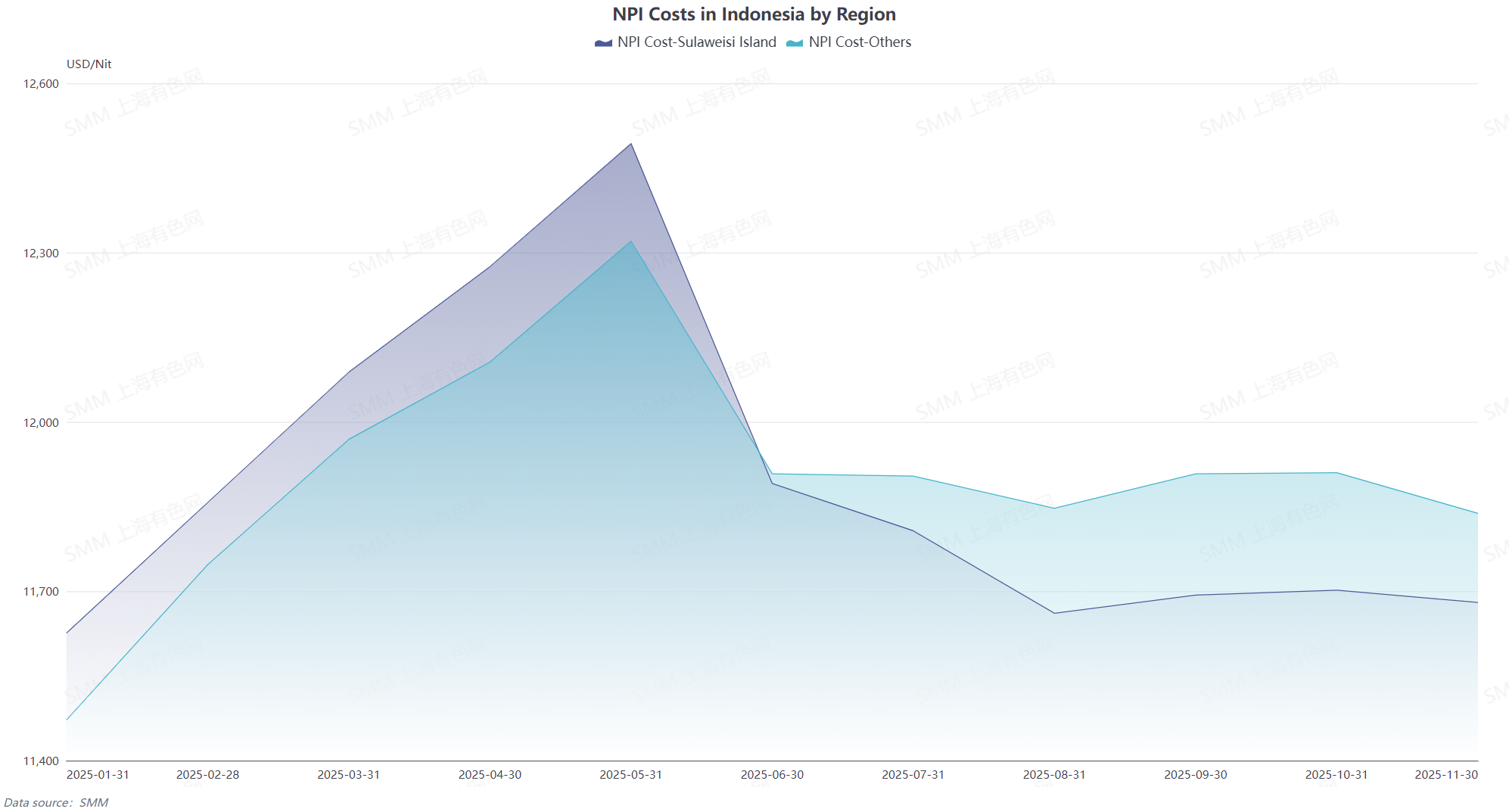

Cost side, nickel ore prices from the Philippines and Indonesia fluctuated due to the rainy season and demand volatility. RKAB quota issues also created sentiment tension. Rising auxiliary material costs domestically and in Indonesia jointly pushed up global NPI smelting costs. Domestic smelters operated at losses for most of the year. Although Indonesia had significant cost advantages, by Q4, price declines approached the cost line, making cost the key bottom support limiting the maximum price decline.

Overall, the core contradiction in the 2025 NPI market is the supply-demand mismatch between "supply increments driven by capacity release in Indonesia" and "slowing growth and periodic weakness in global stainless steel demand." Coupled with rising cost pressures, the industry remained trapped in a cycle of "profit recovery and loss contraction" throughout the year. The global supply center continued shifting toward Indonesia, while the linkage between prices and the stainless steel industry chain significantly strengthened.

![[SMM Analysis] Indonesian nickel ore quota headlines whipsaw China's stainless futures](https://imgqn.smm.cn/usercenter/WNjzM20251217171732.jpeg)