As 2025 enters the countdown phase, the delivery cycle for most domestic aluminum ingot long-term contracts is about to end, and the new year's long-term contract cycle is set to begin. The 2026 domestic aluminum ingot long-term contract market exhibits core characteristics of stable prices with adjustments, declining willingness to sign orders, and a tight supply-demand pattern. Regional long-term contract pricing shows differentiated adjustments in premiums and discounts relative to the SMM A00 aluminum price. Influenced by multiple factors including aluminum prices fluctuating at highs, divergent downstream demand, and global supply deficits, the overall volume of long-term contracts signed is expected to decrease compared to 2025, with significant increase in market uncertainty.

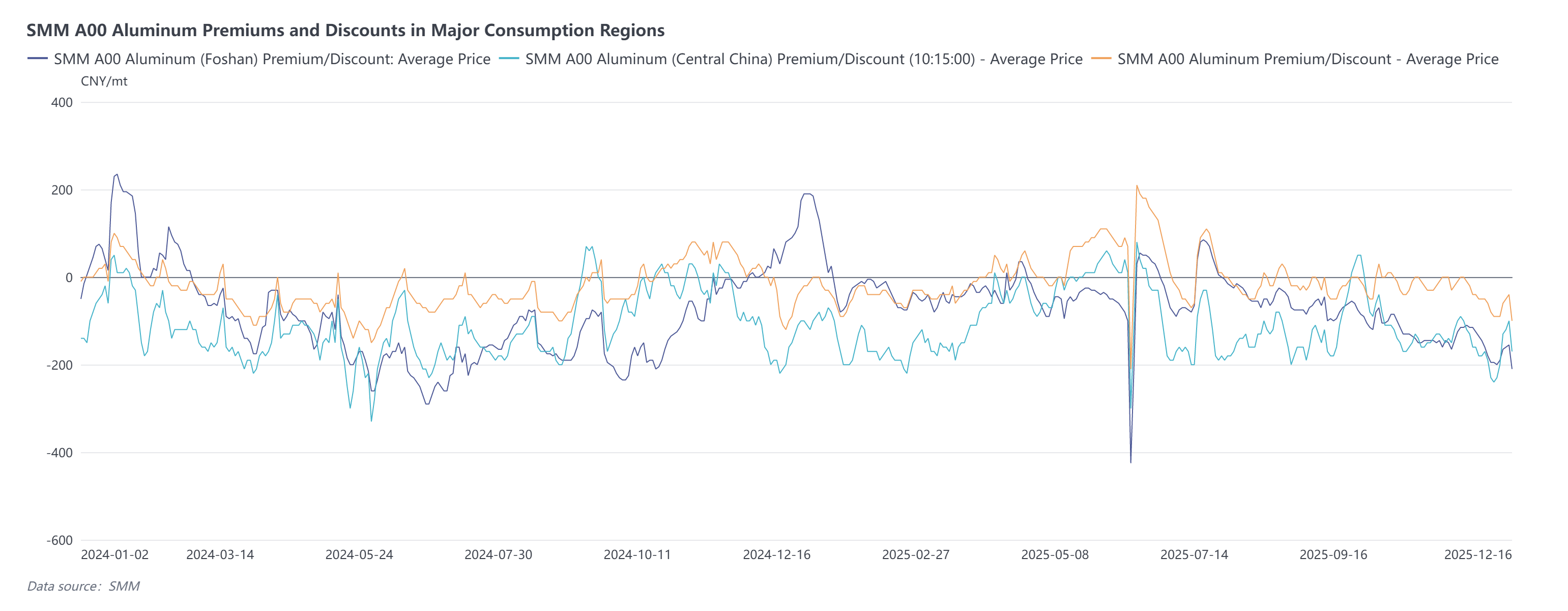

East China: Transactions among traders are mainly at parity with the SMM A00 aluminum price, slightly adjusted down by 0-10 yuan/mt compared to 2025; order signing volume is expected to decrease.

Central China: The mainstream price for 2026 long-term contracts between aluminum plants and traders is at a discount of 70-80 yuan/mt to the SMM A00 aluminum price for self pick-up, flat to slightly down by 10 yuan/mt compared to 2025. Negotiations between traders and downstream aluminum processing enterprises are intense with significant price divergences. Order signing volume is expected to decrease partially, with current indicative prices around a discount of 100 yuan/mt to the SMM A00 aluminum price.

South China: The 2026 long-term contract average offer is at a premium of 5-10 yuan/mt to the SMM A00 aluminum price (South China) or Nanchu price for self pick-up, with point price offers at a premium of 10-15 yuan/mt, flat compared to 2025; order signing volume is expected to be lower than in 2025. Notably, willingness to offer aluminum billet long-term contracts is even lower, indicative offers for dual-average price long-term contracts and fixed processing fee models are relatively scattered, with insufficient market participation.

North-east China: The mainstream price for 2026 long-term contracts is at a premium of 30-40 yuan/mt to the SMM A00 aluminum price (self pick-up), consistent with 2025. The market supply-demand pattern is relatively stable, and order signing volume is expected to maintain the previous year's level.

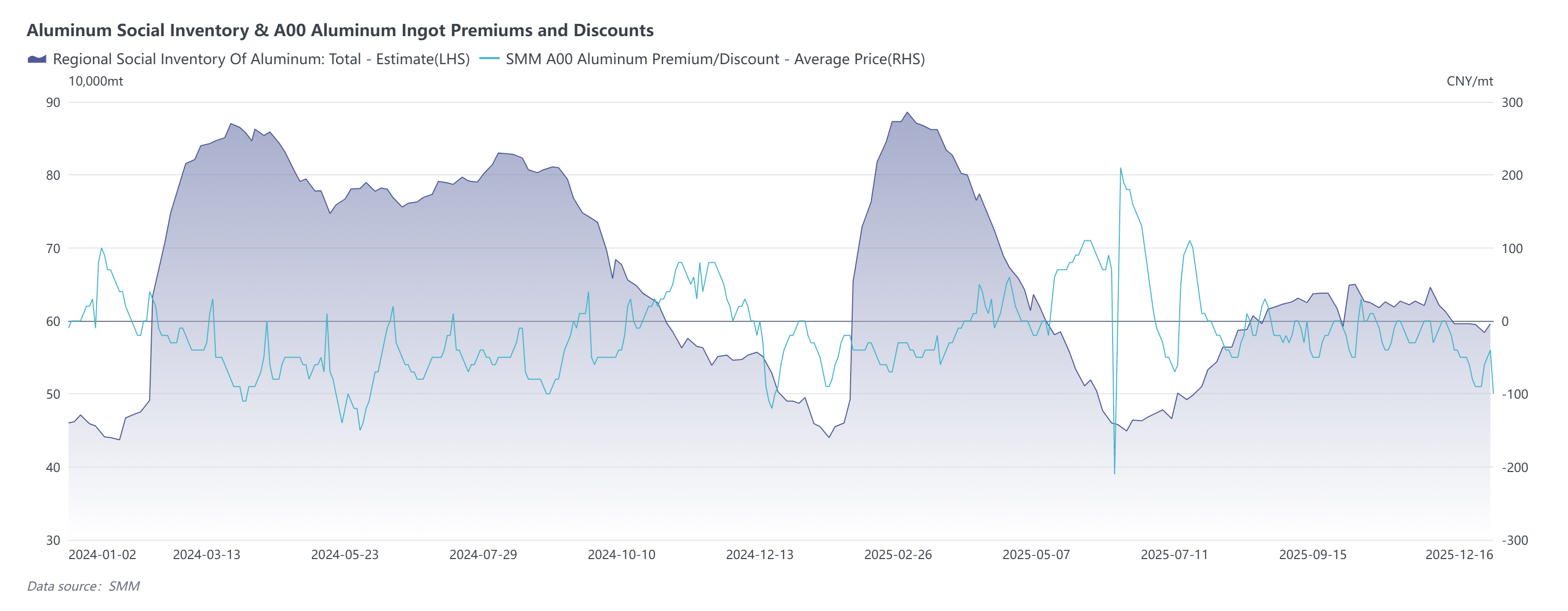

In 2025, domestic aluminum supply gradually approached its ceiling, with production growth rate nearing 0%. According to SMM statistics, by the end of November 2025, the proportion of direct alloying using liquid aluminum reached 77.31%. Coupled with continued resilience in downstream consumption supporting aluminum ingot inventory at persistently low levels, it is expected that under these conditions, aluminum ingot inventory will maintain its current state in the long term, and the 2026 market trend is more inclined towards a seller's market.

Based on 2026 market long-term contract information, most traders and aluminum processing enterprises show reduced willingness to sign long-term contracts, and protracted price negotiations will lead to a decline in the proportion of long-term contracts. SMM analyzes the reasons as follows:

I. Increased aluminum price volatility leads to enterprise strategy adjustments: The surge in copper prices at the end of ͏2025 drove aluminum prices higher, entering a range of high fluctuations with intense volatility in premiums and discounts. Some downstream enterprises focus more on absolute prices, shifting towards flexible purchasing models like "restocking on dips," leading to an adjustment in the ratio between long-term contracts and spot orders.

II. Downstream demand under pressure, pessimistic expectations: Demand in the traditional construction sector is expected to contract, while growth in other traditional end-use sectors slows down. Simultaneously, affected by environmental protection-driven production restrictions and equipment updates, some aluminum processing enterprises face production suspension risks, adopting a cautious and pessimistic attitude towards long-term orders, resulting in decreased signing willingness.

III. Global supply deficits put pressure on premiums and discounts: Overseas aluminum faces production reduction risks, and the commissioning cycle for new project capacity is long, leading to limited incremental global aluminum supply. A supply deficit pattern is expected. Against the backdrop of high aluminum prices, long-term contract premiums and discounts are expected to be under downward pressure, further exacerbating price divergences between buyers and sellers.

Overall, multiple factors including the characteristics of a seller's market under a tight supply-demand balance, aluminum price volatility risks, divergent downstream demand, and global supply deficits collectively introduce significant uncertainty to the signing of 2026 aluminum ingot long-term contracts. The overall volume of long-term contracts signed is expected to decrease compared to 2025, and the market will tend more towards trading models combining short-term flexible purchasing and phased long-term contracts.

![High-Level Consolidation in Secondary Aluminum[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)