SMM December 12 News:

Abstract: Recently, the special meeting on ensuring supply and stabilising prices for phosphate fertilizers and the release of Yuntianhua’s initiative aimed to stabilise the domestic fertilizer market for spring plowing. However, the underlying reality of "high sulfur prices" and the strong regulatory measures of "domestic priority and export restrictions" may have a significant impact on the new energy industry, particularly in the field of LFP batteries.

I. Industry Hot Topics: Phosphate Fertilizer Market Symposium + Yuntianhua’s Initiative + Ensuring Supply and Stabilising Prices

[Phosphorus Chemical Industry: Beijing Phosphate Fertilizer Market Symposium Reaches Four Consensus Points Involving Exports, Price Stability, and Sulfur]

On December 11, 2025, under the guidance of the National Development and Reform Commission (NDRC)’s Department of Economy and Trade, the China Agricultural Means of Production Circulation Association and the China Phosphate and Compound Fertilizer Industry Association organized a special meeting with key phosphate fertilizer producers and distributors to ensure supply and stabilise prices for phosphate fertilizers. Four recommendations were proposed:

1. Maintain high operating rates without production cuts and refrain from arranging exports before August 2026;

2. Refrain from adjusting purchase and sales prices until the end of the 2026 spring plowing season;

3. Coordinate key raw materials such as sulphuric acid with "domestic priority";

4. Ensure market prices reflect genuine supply and demand.

[Phosphorus Chemical Industry: Yuntianhua Releases Initiative to Ensure Supply and Stabilise Prices for Phosphate Fertilizer Products]

On December 9, 2025, Yuntianhua released an initiative to ensure supply and stabilise prices for phosphate fertilizer products. Due to the impact of rising sulfur prices on the cost of sulphuric acid, a key raw material for phosphate fertilizer production, the cost per metric ton of phosphate fertilizer increased by approximately 1,000 yuan. This cost pressure has led to meager profits or even losses for phosphate fertilizer enterprises. Given that phosphate fertilizers are critical to food security, Yuntianhua proposed that the industry strive to ensure supply and stabilise prices, jointly maintain market order, and support increased production and harvests. On May 10 of this year, amid rising sulfur prices, the China Phosphate and Compound Fertilizer Industry Association solemnly put forward an industry self-discipline initiative aimed at ensuring stable supply and reasonable prices in the fertilizer market.

II. Hot Topic Interpretation: Special Symposium on the Phosphate Fertilizer Market (Ensuring Supply + Restricting Exports + Stabilising Prices + Regulating Sales + Securing Raw Materials + Domestic Priority + Strengthening Coordination + Information Transparency), Yuntianhua’s Responsibility and Determination

The core of the special symposium on the phosphate fertilizer market can be summarised as "four sentences, eight key points."

Key Point 1: The preparation of fertilizers for spring plowing has entered a critical stage;

Key Point 2: Abnormal price fluctuations in local phosphate fertilizer markets require national coordination and regulation.

Key Point 3: The fundamental supply and demand of phosphate fertilizers show no gap, and supply in the later period is guaranteed;

Key Point 4: Price fluctuations stem from rising costs, periodic demand, and unstable market expectations, which can be mitigated through regulation.

Key Point 5: Producers are operating at high capacity and have voluntarily agreed not to export before August 2026;

Key Point 6: Production and sales are locked at reasonable prices, with no price increases before the 2026 spring plowing season, and strict prohibitions on stockpiling and price gouging;

Key Point 7: Raw materials such as sulphuric acid are given "domestic priority," and associations are organizing the signing of stable supply and sales contracts;

Key Point 8: Stabilise expectations, return fertilizer prices to reasonable levels, ensure sufficient and stable fertilizer supply for the 2026 spring plowing season, and protect farmers’ enthusiasm.

Yuntianhua’s release of the initiative to ensure supply and stabilise prices for phosphate fertilizer products demonstrates the company’s responsibility and determination. Although commercial companies are inherently market-oriented and profit-driven, the ability to pursue economic benefits while remaining committed to serving the industry is particularly commendable.

III. LFP: Analysis of Multiple Impacts on the New Energy Industry

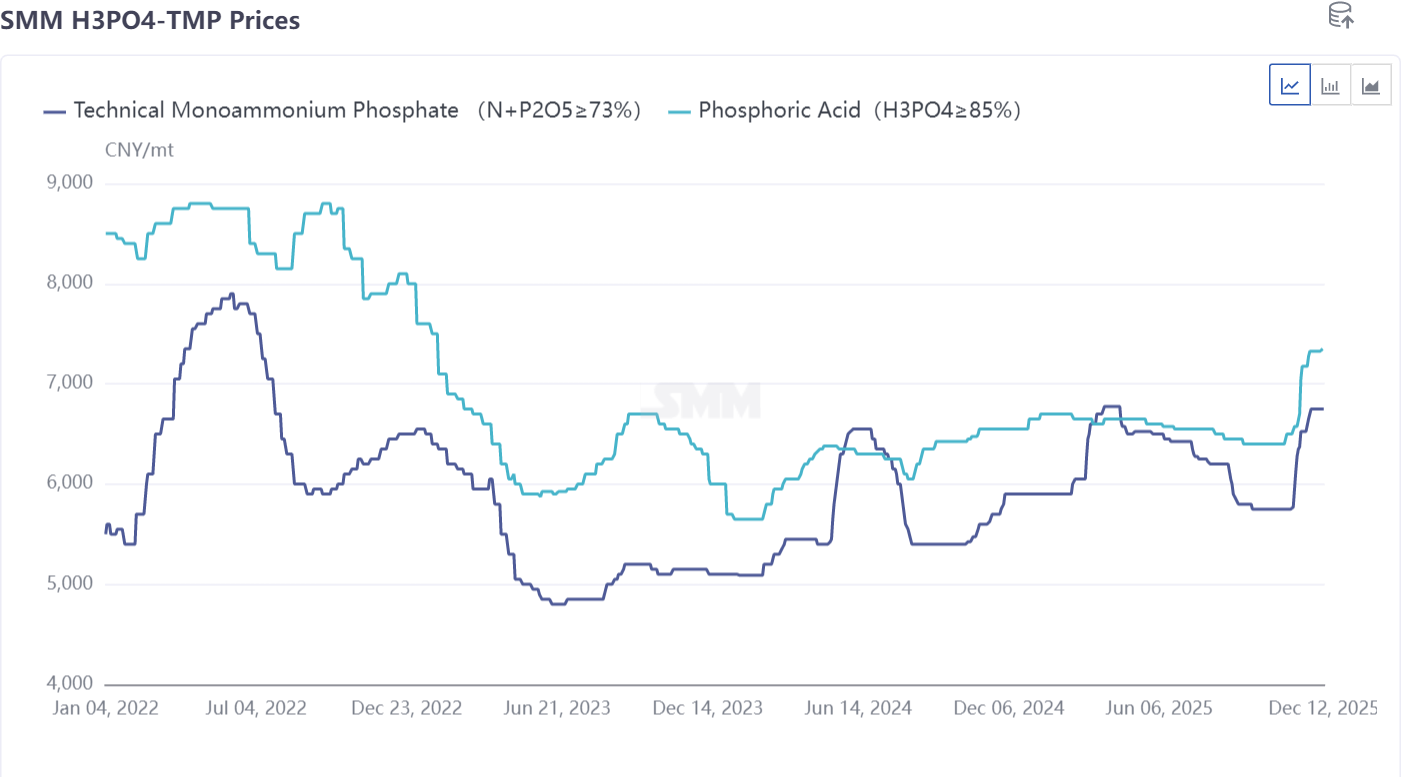

Phosphorus sources for LFP and sulfur prices.

High sulfur prices have stopped rising and begun to decline after prices stabilised. Currently, the prices of phosphoric acid and industrial-grade MAP continue to rise.

In the new energy industry chain, particularly for LFP cathode materials, the upstream consists of high-purity phosphoric acid/monoammonium phosphate (MAP), which shares the same origin as the phosphate fertiliser industry. Regulatory measures in the phosphate fertiliser market are transmitted to the new energy sector through the following pathways:

1. Intensified competition for resources, leading to tightening supply of industrial-grade MAP and purified wet process phosphoric acid.

Logic: Policies require sulphuric acid to be prioritised domestically for phosphate fertiliser production, and phosphate fertiliser prices are frozen. This may result in high-grade phosphate ore and sulphuric acid resources, which could be used to produce industrial-grade MAP and purified wet process or food-grade phosphoric acid, being allocated preferentially to fertiliser-grade ammonium phosphate production lines with heavy supply assurance tasks.

The allocation of capacity and raw materials by phosphorus chemical enterprises may lean toward fertilisers, potentially squeezing the supply of raw materials for industrial phosphoric acid and its downstream products (such as iron phosphate).

The release of capacity for iron phosphate, the precursor to LFP cathode materials, may be constrained by the availability of raw materials (phosphorus and sulphur sources), increasing supply uncertainty.

2. Blocked cost transmission, reshaping the profit structure of the industry chain.

Against the backdrop of strict prohibitions on hoarding and price gouging, along with price freezes, cost pressures in the phosphate fertiliser segment (high sulphur prices) cannot be smoothly passed on to downstream agricultural consumers. These pressures must inevitably be absorbed within the entire phosphorus chemical system.

To maintain overall profits, phosphorus chemical enterprises may be more motivated to shift costs toward sectors with higher marketisation levels and smoother price transmission, such as industrial-grade MAP, phosphoric acid, and new energy materials. This directly increases the manufacturing cost of LFP cathode materials.

3. Export restriction warnings, curbing the pace of price increases.

The current regulatory measures require that phosphate fertiliser exports not be arranged for nearly three quarters (until August 2026). In the face of food security and strategic resource supply assurance, commercial export demands may be temporarily sidelined.

New energy enterprises need to reassess the long-term supply security of upstream phosphorus chemical resources. Enterprises with phosphate ore resources may use profits from phosphate ore to offset losses in phosphate fertilisers, while those without phosphate ore resources will face survival pressures. Although the current restrictions target fertiliser exports, in extreme scenarios, policies might guide or restrict the export of industrial phosphates to ensure raw materials for the domestic new energy industry chain. This prompts downstream battery and automaker enterprises to consider ways to secure phosphorus resources through long-term agreements, joint ventures, equity investments, or even upstream integration. 4. Conclusions and Outlook

This phosphate fertiliser supply assurance and price stabilisation initiative, ostensibly a regulatory measure in the agricultural sector, is in fact a rebalancing of "sulfur–phosphate resources" across different strategic industries (agriculture vs. new energy) at the national level.

In the short term, the new energy sector will primarily bear the pressure of rising costs and tight raw material supply. The cost advantages of the lithium iron phosphate (LFP) route may be somewhat eroded.

In the medium and long term, this will strongly drive deeper integration and strategic positioning of the new energy industry chain toward the upstream phosphate resource segment. The strategic importance of chemical enterprises with advantages in phosphate ore, sulfur, and integrated industry chains—such as Yuntianhua, SD Lomon, Yuntianhua, Xingfa Group, Chanhen, Xinyangfeng, and YunTu—will become more prominent. At the same time, it will compel the industry to develop new technological pathways, such as the utilization of low-grade phosphate ore and cost-reducing innovations in phosphoric acid processes.

In summary, high sulfur prices and phosphate fertiliser regulation have sounded an alarm for the rapidly advancing new energy sector: in the grand narrative of transitioning to green energy, foundational reliance on traditional chemical resources and associated geopolitical risks remain critical challenges that must be directly confronted and resolved.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!

![Electrolyte Prices Remained Temporarily Stable This Week (2026.3.30-4.2) [SMM Lithium Battery Electrolyte Market Weekly Review]](https://imgqn.smm.cn/usercenter/QxQbN20251217171727.jpg)

![[SMM Analysis] Cobalt Chloride: The Stalemate of Holding Prices Firm Remained Unbroken, with the Transaction Center Holding Steady Near 115,000 Yuan](https://imgqn.smm.cn/usercenter/HySQT20251217171731.png)

![[SMM Analysis] Co3O4: Tight Inventory Provided Cost Support, While Demand Awaited Clarity and Prices Remained Stable Amid a Wait-and-See Sentiment](https://imgqn.smm.cn/usercenter/wzbHd20251217171731.jpg)