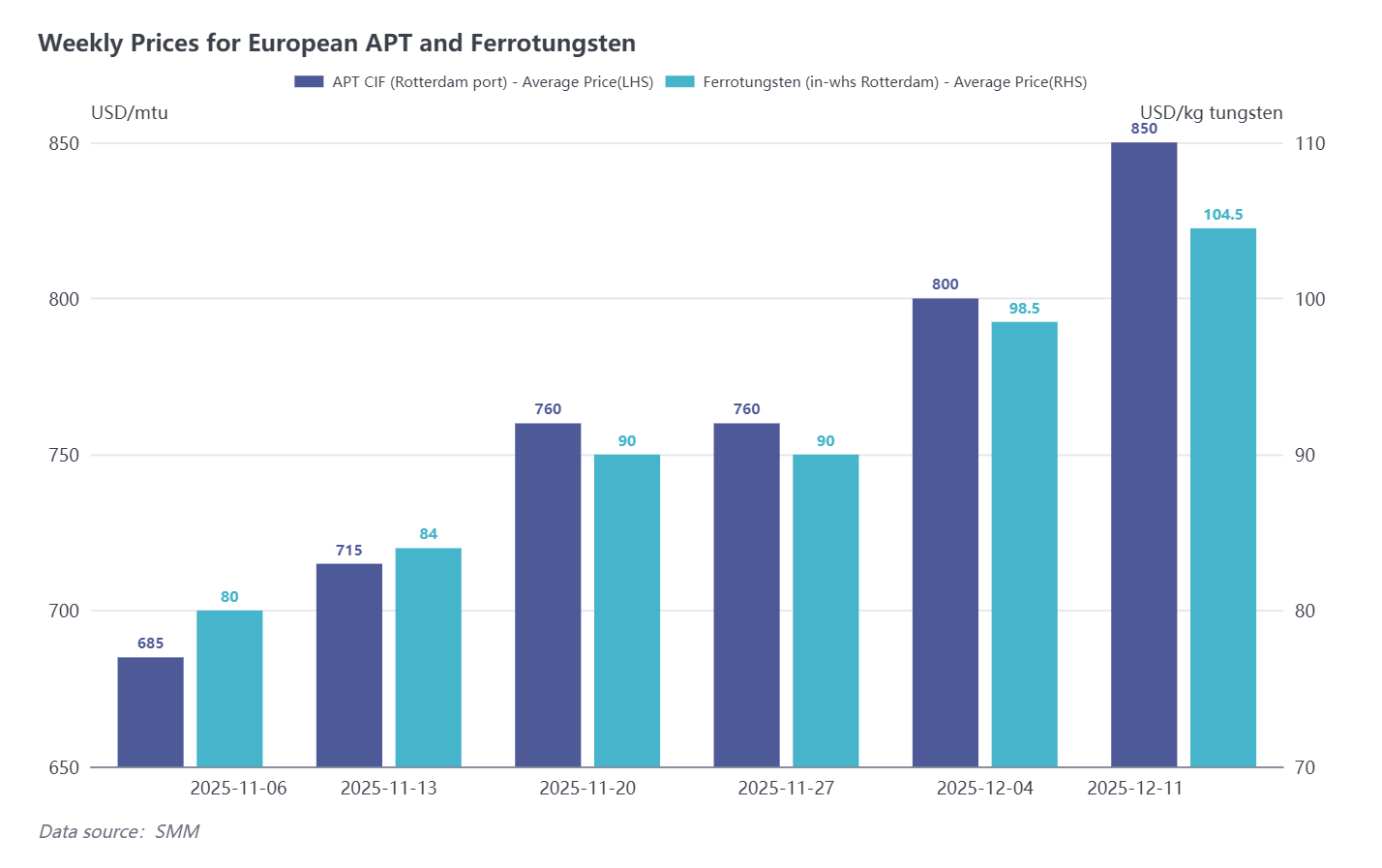

On December 12, SMM Ammonium Paratungstate (APT) CIF (Rotterdam port) price is USD 830-870 per metric ton unit (mtu), with an average of USD 850/mtu, up by USD 50/mtu from last week. Ferrotungsten (Rotterdam warehouse) price is USD 101-106 per kg W, with an average of USD 104.5/kg W, up by USD 6/kg W from last week.

European Tungsten Market Follows China's Gains; Supply Tightness May Push APT Offers to the Thousand-Dollar Mark

This week, European market prices continued to rise, following the upward trend in the Chinese tungsten market. According to SMM research, the latest European tungsten concentrate CIF offers have increased to USD 700-720/mtu. Regarding APT, due to limited domestic European APT production and scarce spot availability, actual tradable material is extremely limited. The latest transaction price still stands at USD 805/mtu. However, driven by rising ore price pressure and downstream demand support, APT offers have been pushed up to USD 835-870/mtu.

European traders stated: "As the Chinese market rises rapidly, the European market will inevitably follow, and European prices will be higher than China's because we lack raw materials, and supply is very tight. It is expected that European APT offers will soon reach USD 1000/mtu, and our end-users are willing to pay that price."

Currently, European smelters' production primarily relies on tungsten scrap recycling, along with small quantities of tungsten concentrate sourced locally, from Africa, and from Australia. Approaching Christmas, most producers plan to halt production earlier next week compared to previous years, precisely due to raw material shortages. This also means European market trading will largely stall next week, and prices may continue to follow the upward movement of the Chinese market.

Domestic Shortage Coupled with Policy Barriers Leaves Little Motivation for APT Exports

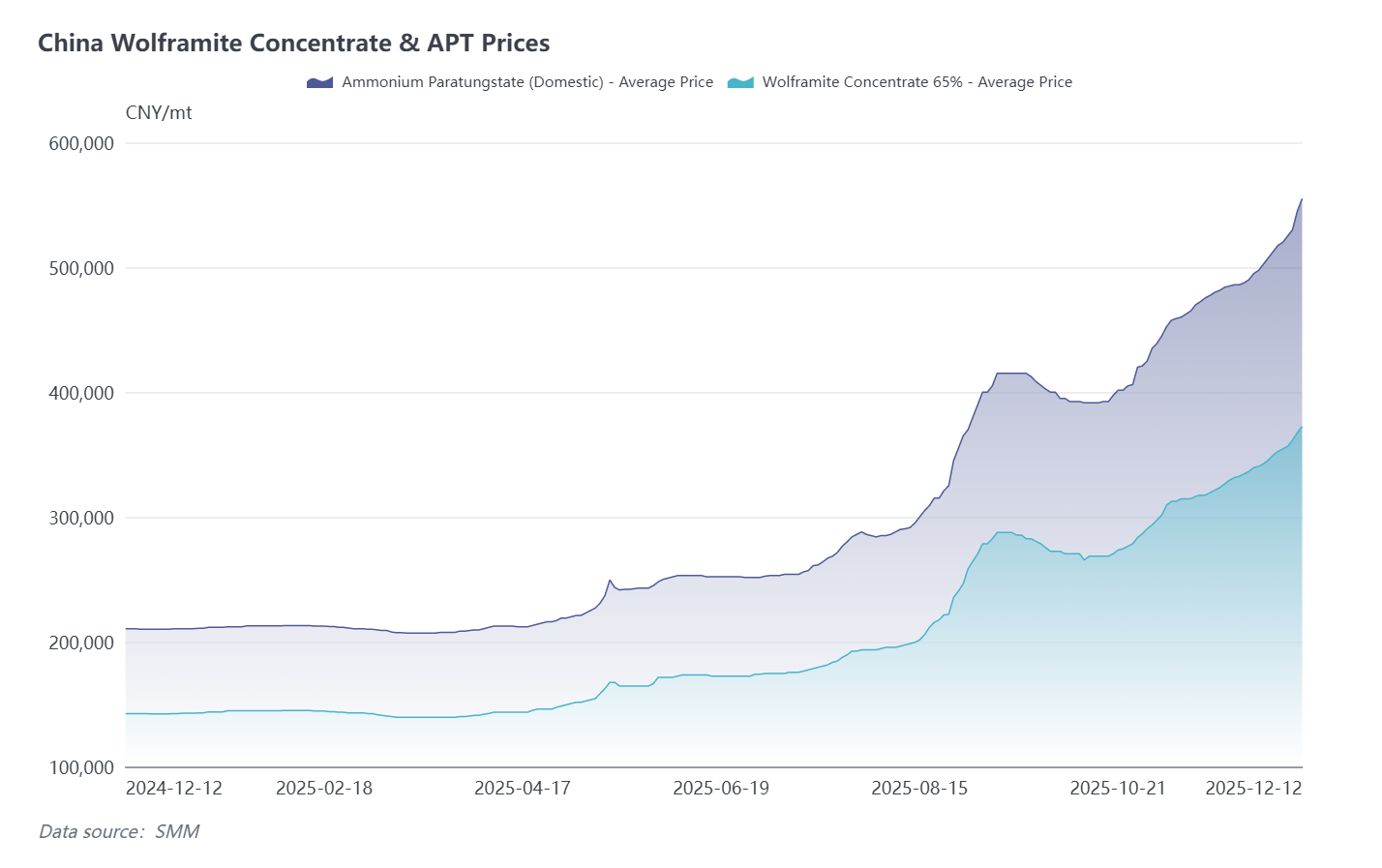

From the current situation in the Chinese tungsten market, domestic tungsten concentrate and APT supply remains consistently tight, with mine production quotas largely exhausted. Some APT producers have already halted production this month, exacerbating supply pressures and triggering a wave of panic buying in downstream markets. As of today, SMM price data shows domestic APT transaction prices have been pushed up to 555,000 yuan/ton (approximately USD 887/mtu).

According to SMM understanding, affected by China's export control policies on tungsten products, traders must obtain relevant qualifications and go through strict declaration and approval procedures before they can export APT and tungsten oxide products. Exporting to European end-users, from declaration to completion of transportation, takes nearly four months in total. This is also the main reason why October customs data showed APT exports had already dropped to zero.

Given the current situation, Chinese tungsten prices are rising rapidly, while European market prices have not yet formed a significant price gap with domestic prices. Therefore, domestic traders are more inclined to sell APT resources in the domestic market rather than investing the longer time cost required for export applications. For tungsten powder and other exportable downstream products, their export offers will follow the price trend of the domestic Chinese tungsten market and may be higher than domestic price levels due to supply tightness, logistics, and compliance costs.

Regarding the Future Outlook

The core dilemma of the European tungsten market remains the lack of raw material mineral supply, directly leading to continuous shortages of smelted products like APT and ferrotungsten. Currently, only some tungsten powder enterprises maintain production relying on stable prior supply sources. However, downstream demand remains robust, far exceeding market supply availability. Against this backdrop, overall trading activity in the European tungsten market is tending towards thinness, with the contradiction between severe supply shortages and strong demand becoming prominent. Prices are expected to continue their upward trend.

![[SMM Analysis] What Drove Global Tungsten Markets in March? Offshore Prices Up 30%, China Enters Consolidation](https://imgqn.smm.cn/usercenter/eGQFu20251217171723.jpeg)