SMM December 11 News:

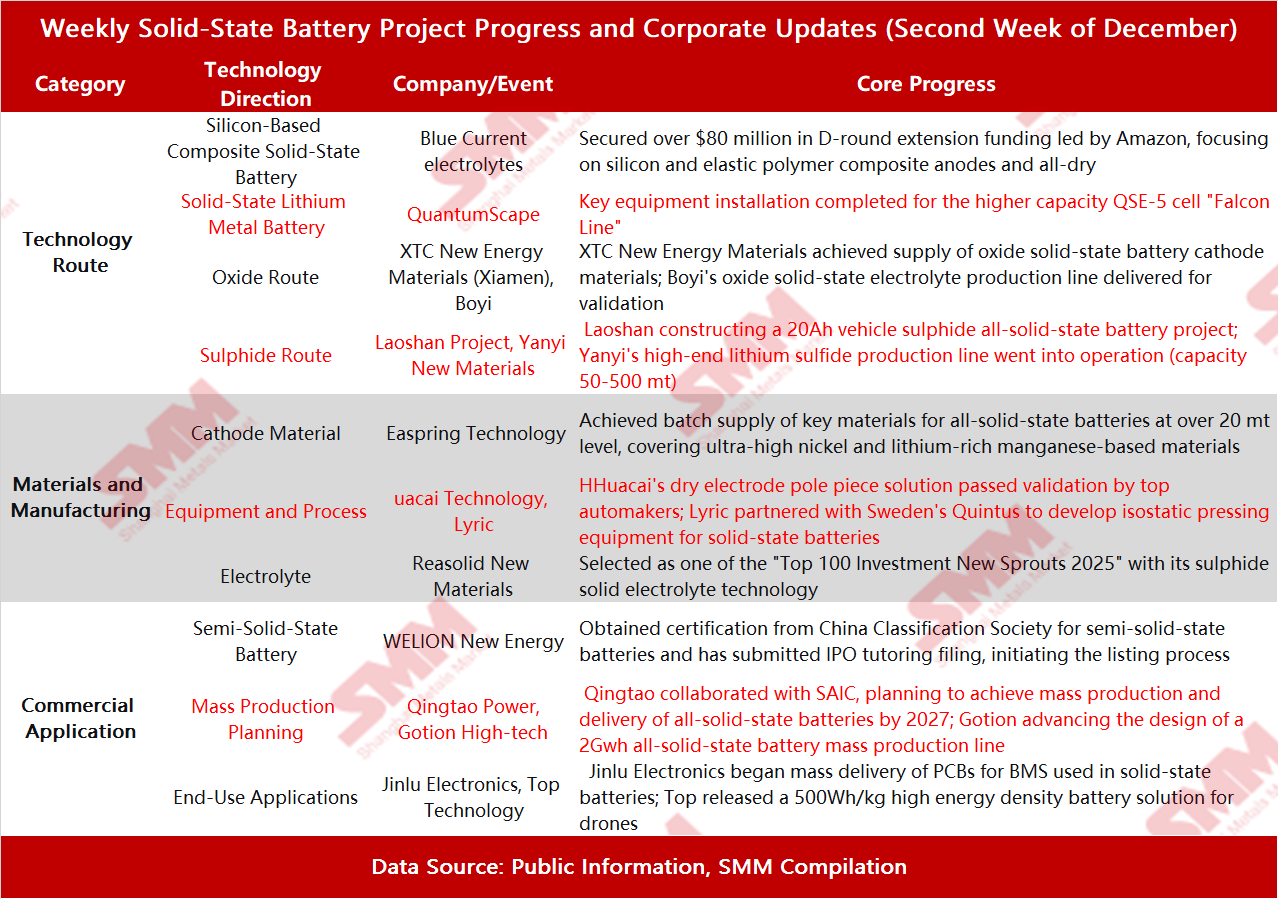

Key Points: This week, the solid-state battery sector gained significant momentum, with multiple domestic enterprises achieving key breakthroughs in environmental approvals, sample deliveries, and mass production, while overseas players in South Korea and the U.S. intensified technological competition. The industry chain advanced simultaneously across all segments, from cathode and anode materials and electrolytes to battery cell manufacturing, entering a phase of intensive validation and capacity building.

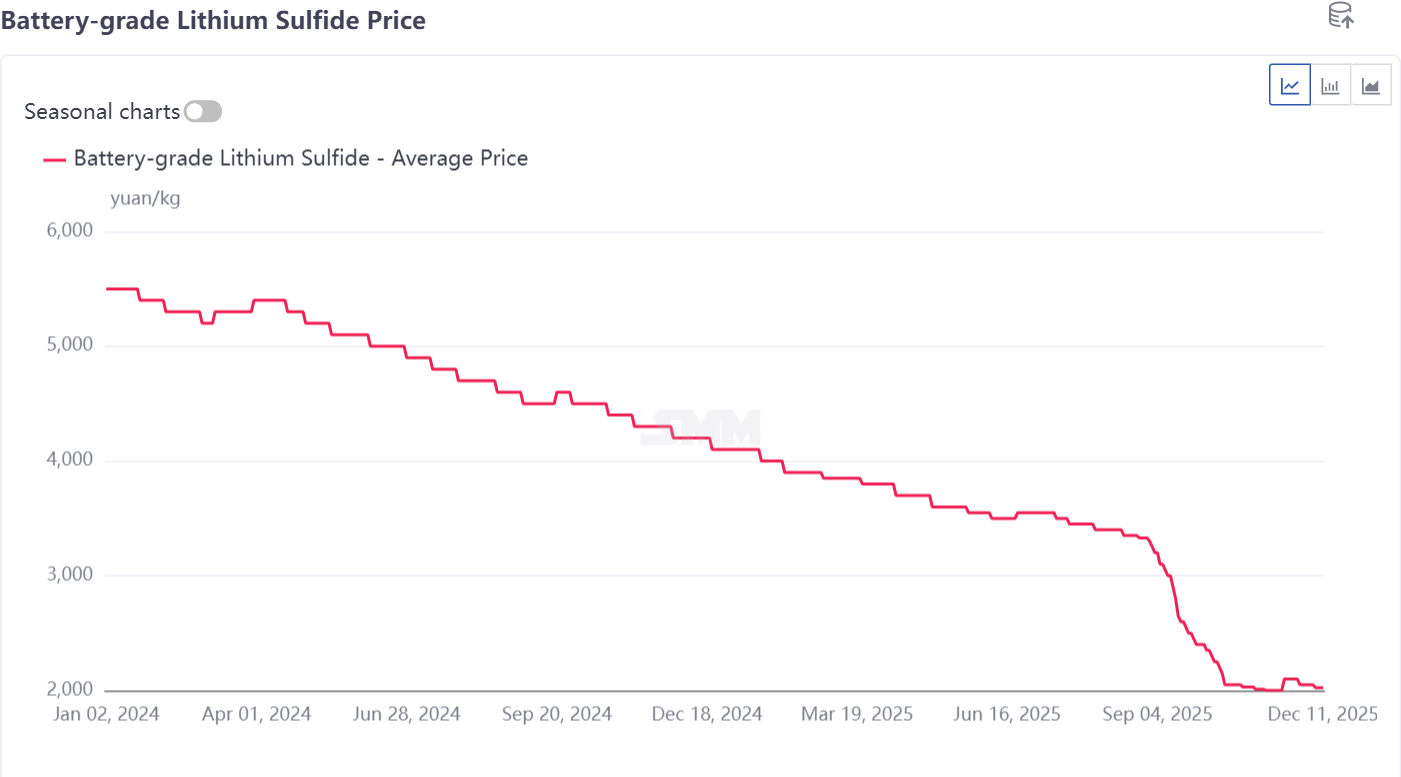

This week, lithium sulfide prices remained stable with a slight downward trend. Operating rates at lithium sulfide enterprises were relatively high, with shipments primarily consisting of small orders. The average price stood at 2,025 yuan/kg.

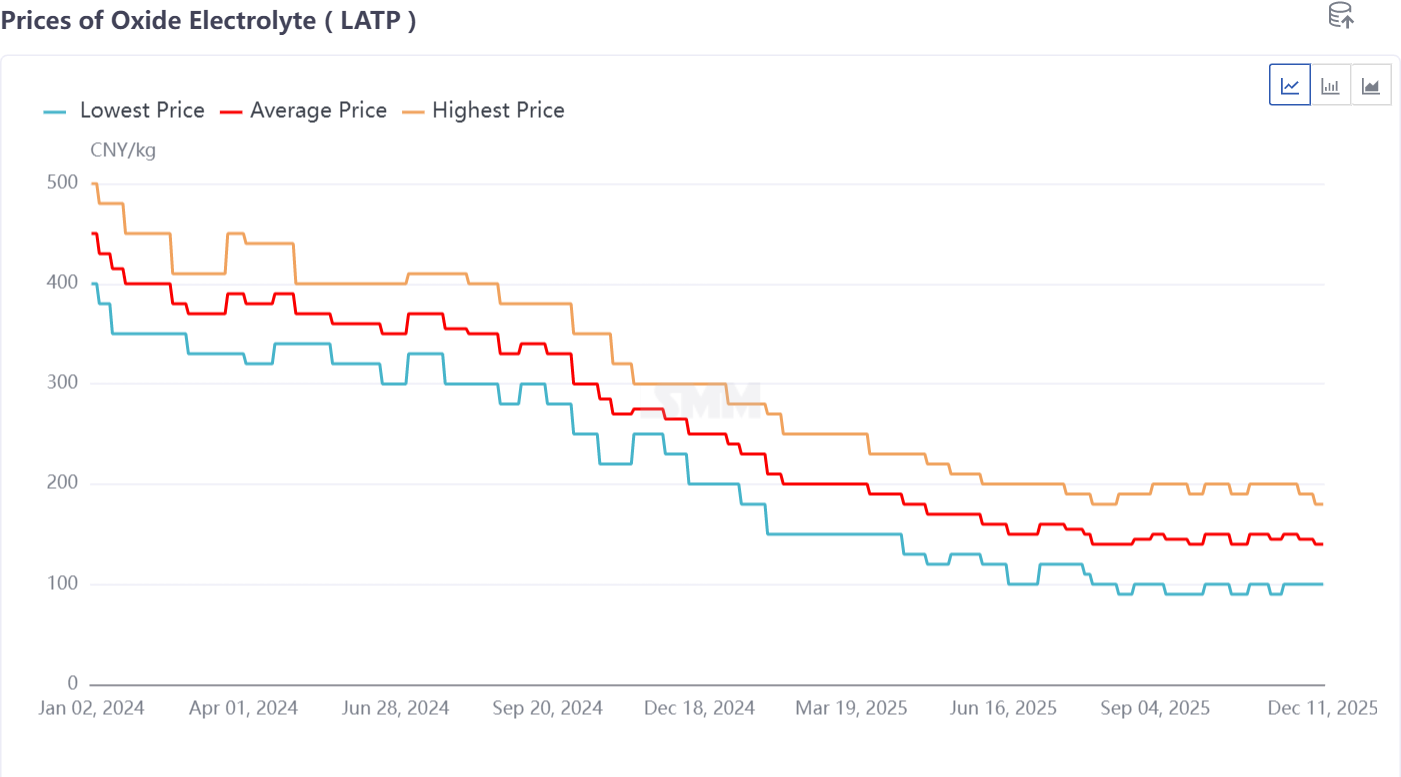

Meanwhile, the price of oxide electrolyte LATP experienced a minor decline. Its application remained focused on the downstream semi-solid battery industry, with an average price of 140 yuan/kg.

Regarding this week's developments in solid-state batteries, the domestic and international situation can be understood at a glance.

I. Key Materials: Electrolyte + Cathode

Materials are the core of breakthroughs in solid-state battery technology. This week, domestic enterprises made substantial progress in both electrolyte and cathode materials.

In solid-state electrolytes, Boyi Technology successfully delivered production lines for oxide solid-state electrolytes (such as LATP and LLZO) and completed batch verification. Yanyi New Materials officially put its high-end lithium sulfide production line into operation, with an annual capacity of 50–500 mt, providing key raw material support for sulfide electrolytes.

The sulfide route also saw specific application projects, with Qingdao Laoshan’s high-performance 20Ah vehicle-grade sulfide all-solid-state battery project under construction.

Progress in cathode materials was equally notable. XTC New Energy Materials (Xiamen) already achieved supply of cathode materials compatible with oxide solid-state batteries. Easpring Technology further announced that its key materials for all-solid-state batteries achieved batch supply exceeding 20 mt, covering ultra-high-nickel materials with energy densities over 400 Wh/kg and lithium-rich manganese-based materials targeting 500 Wh/kg batteries.

II. Equipment First: Dry Electrode + Isostatic Pressing Equipment

Innovations in manufacturing processes are key to reducing costs and improving efficiency for solid-state batteries. This week, Huacai Technology announced that its integrated dry electrode pole piece solution passed rigorous testing and validation by a global top-tier luxury automaker.

Dry electrode technology eliminates the need for solvents, simplifies production, reduces costs, and is more compatible with solid-state electrolyte systems. It is considered one of the core future processes for mass production of solid-state batteries. Huacai planned to launch a “new-generation integrated dry electrode solution” in 2026.

Meanwhile, Lyric signed an agreement with Sweden’s high-pressure technology leader Quintus to jointly develop isostatic pressing equipment for solid-state batteries. High-pressure treatment is a critical process for improving interface contact and density in solid-state battery cells. The development of specialized equipment is vital for industrialisation.

III. Mass Production Progress: Semi-Solid-State + All-Solid-State + Production and IPO

In the transition from lab to market, semi-solid-state batteries, as an interim solution, already achieved commercial application. WELION New Energy was active in the semi-solid-state sector, with its battery products successively obtaining cell and battery pack certifications issued by the China Classification Society (CCS). This indicates that semi-solid-state batteries gained access approval in specific high-safety-demand sectors such as marine applications. Concurrently, WELION New Energy submitted its IPO tutoring filing, initiating the listing process and demonstrating clear intent to accelerate development via capital markets.

Regarding mass production planning for all-solid-state batteries, domestic companies provided clear timetables. Qingtao Power, in collaboration with SAIC, completed the integration of its Anting all-solid-state battery production line. It planned to deliver samples by the end of 2025 and achieve mass production and delivery in 2027.

Gotion High-tech also advanced the design of its 2 GWh Jinshi all-solid-state battery mass production line. The company’s first 0.2 GWh pilot line achieved a remarkable yield rate of 90%, laying the foundation for mass production.

IV. Auxiliary Material Market: Industry Chain Synergy: Comprehensive Upgrade from Materials to Applications

In upstream key auxiliary materials, Jinlu Electronics successfully developed and mass-produced PCB boards for solid-state battery BMS (Battery Management System), reflecting new requirements of the solid-state battery system for supporting electronic components.

V. Downstream Applications: Drones

In end-use application expansion, battery enterprises are actively exploring markets beyond automobiles. Top Technology released a drone-specific battery solution with an energy density of up to 500 Wh/kg and planned a technical target of over 600 Wh/kg by 2028.

VI. Capital Market: CATL’s 2.6 Billion Yuan + Canmax

CATL invested 2.6 billion yuan to become the second-largest shareholder of Canmax, which has an extensive layout in the solid-state battery materials field. This investment strengthened the industry leader’s positioning for future technology routes.

VII. Overseas Market: Blue Current + QuantumScape

The race for solid-state battery commercialization showed a clear dual-driver pattern of funding and capacity this week. Blue Current secured over $80 million in a Series D extension led by Amazon, signaling capital market recognition of the differentiated technology route of silicon-based solid-state batteries.

This funding not only injected strong momentum into Blue Current’s commercialization process but also hinted at the strategic layout of tech giants like Amazon for next-generation battery technology in ESS and future transportation applications.

Across the ocean, QuantumScape announced that key equipment installation was completed for its higher-capacity QSE-5 battery cell “Falcon Production Line” in San Jose. This was a critical step in the company’s roadmap toward scaled production of lithium-metal anode solid-state batteries.

The progress of the two presented a sharp contrast: Blue Current emphasized safety and compatibility with existing production lines through its unique silicon-composite anode and all-dry electrolyte process, while QuantumScape continued betting on its disruptive “anode-free” design and flexible ceramic electrolyte, pursuing extreme energy density and fast-charging performance.

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!