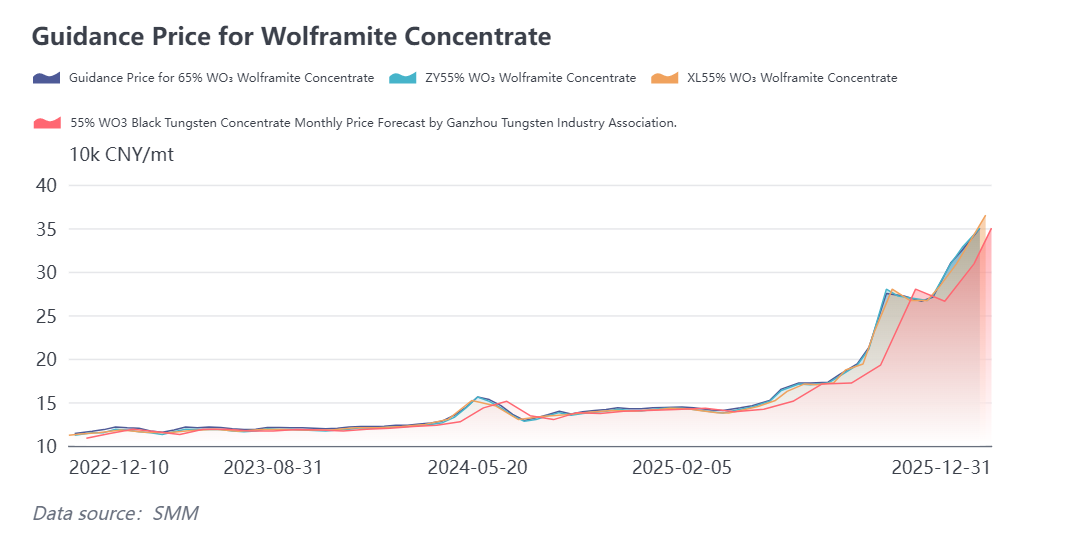

SMM December 9 News:

Driven by multiple favorable factors including tight raw material supply, tungsten prices have been on a sustained upward trend since mid-to-late October, with historical highs being frequently set! From the supply side, the tungsten raw material market remains tight. Coupled with the gradual issuance of domestic tungsten mining quotas across various provinces in November, the market anticipates the total annual quota volume will be lower than the 2024 level. Looking at the long-term contract prices set by major tungsten enterprises, companies like Jiangxi Tungsten and Zhangyuan Tungsten have successively raised their long-term contract offers, further supporting the price increase. As of December 9, the average price of Wolframite Concentrate (≥65%) has climbed to 356,500 CNY/mt, with a staggering year-to-date increase of 149.74%.

Jiangxi Tungsten, Zhangyuan Tungsten, and Other Tungsten Enterprises Raise Long-Term Contract Prices Again

Several tungsten enterprises have raised their long-term contract prices for the first half of December, details as follows:

Ganzhou Tungsten Industry Association: 55% black tungsten ore at 350,000 CNY/mt, up 41,000 CNY/mt month-on-month; APT at 510,000 CNY/mt, up 57,000 CNY/mt month-on-month; Medium-grain tungsten powder at 880 CNY/kg, up 150 CNY/kg month-on-month. (Prices are for reference only, commercial risks are borne by the parties involved.)

Chongyi Zhangyuan Tungsten Co., Ltd.: 55% black tungsten concentrate: 350,000 CNY/mt, up 22,000 CNY/mt from the previous offer; 55% scheelite concentrate: 349,000 CNY/mt, up 22,000 CNY/mt from the previous offer; Ammonium Paratungstate (APT): 510,000 CNY/mt, up 32,000 CNY/mt from the previous offer.

Jiangxi Tungsten Holding Group Co., Ltd.: 65% black tungsten concentrate is 350,000 CNY/mt, up 25,000 CNY/mt from the second half of November.

Xiamen Tungsten: Long-term APT procurement price for the first half of December 2025 is set at 500,000 CNY/mt, up 30,000 CNY/mt from the second half of November.

Guangdong Xianglu Tungsten Co., Ltd. :55% Wolframite Concentrate, the price was set at 365,000 CNY/mt, an increase of 34,000 CNY/mt from the previous period; for 55% Scheelite Concentrate, it was priced at 364,000 CNY/mt, also up 34,000 CNY/mt; and for Ammonium Paratungstate (APT), the price reached 530,000 CNY/mt, reflecting an increase of 49,000 CNY/mt.

Tungsten Prices Continuously Rise, Wolframite Concentrate Up Nearly 150% This Year

Tungsten prices have been rising steadily, frequently setting new historical records! According to the latest SMM quotations, on December 9, the price for Wolframite Concentrate (≥65%) ranged from 356,000 to 357,000 CNY/mt, with an average price of 356,500 CNY/mt, up 0.56% from the previous trading day! Compared to the average price of 142,750 CNY/mt on December 31, 2024, this new high of 356,500 CNY/mt represents an increase of 213,750 CNY/mt year-to-date, a surge of 149.74%.

This year's tungsten price increase is primarily attributed to the combined effect of tightened supply, smooth cost transmission, and support from downstream rigid demand: China's annual tungsten mining quota is expected to be lower than 2024's. Quotas in major producing regions showed no increase, with some provinces seeing year-on-year declines. Additionally, quota utilization rates were low in regions like Yunnan and Guangdong. Coupled with major mines slowing their sales pace at year-end, market circulation volume has further contracted. The ongoing deepening of domestic tungsten mining quota control policies ensures strategic resource management at the source. Simultaneously, the high price transmission path for tungsten is smooth. APT smelting has turned profitable, and industry operating rates are steadily recovering. In downstream mid-to-high-end applications, there is a lack of substitutable materials for tungsten, leading to orders concentrating towards leading enterprises. Cost pressures are forcing end-product price hikes. In the overseas market, influenced by China's export controls, production cuts at Vietnamese tungsten enterprises, and tungsten being listed as a strategic metal in Europe and the US, tungsten product premiums have seen some recovery. However, the overall market shows weak supply and demand, leaving room for price catch-up.

Market Outlook

Overall, strongly supported by tight mine-side supply, tungsten prices have risen steadily recently. Entering December, the tight supply situation for tungsten raw materials has not improved, and the supply-demand imbalance remains unresolved. The trend of high tungsten prices is expected to continue.

Specifically, the tungsten market in December will continue to face a dual scenario: on one hand, supply-side constraints from mining quotas make it difficult to change the tight supply of tungsten raw materials; on the other hand, downstream end-use application sectors are undergoing structural adjustment. In the absence of new materials capable of large-scale substitution for tungsten, the tight supply situation in the tungsten market is likely to persist, thereby supporting tungsten prices to close out 2025 at high levels. Looking ahead to Q1 2026, the market needs to focus on changes in mine shipment pace and the release of a new round of downstream restocking demand.

![[SMM Analysis] What Drove Global Tungsten Markets in March? Offshore Prices Up 30%, China Enters Consolidation](https://imgqn.smm.cn/usercenter/eGQFu20251217171723.jpeg)