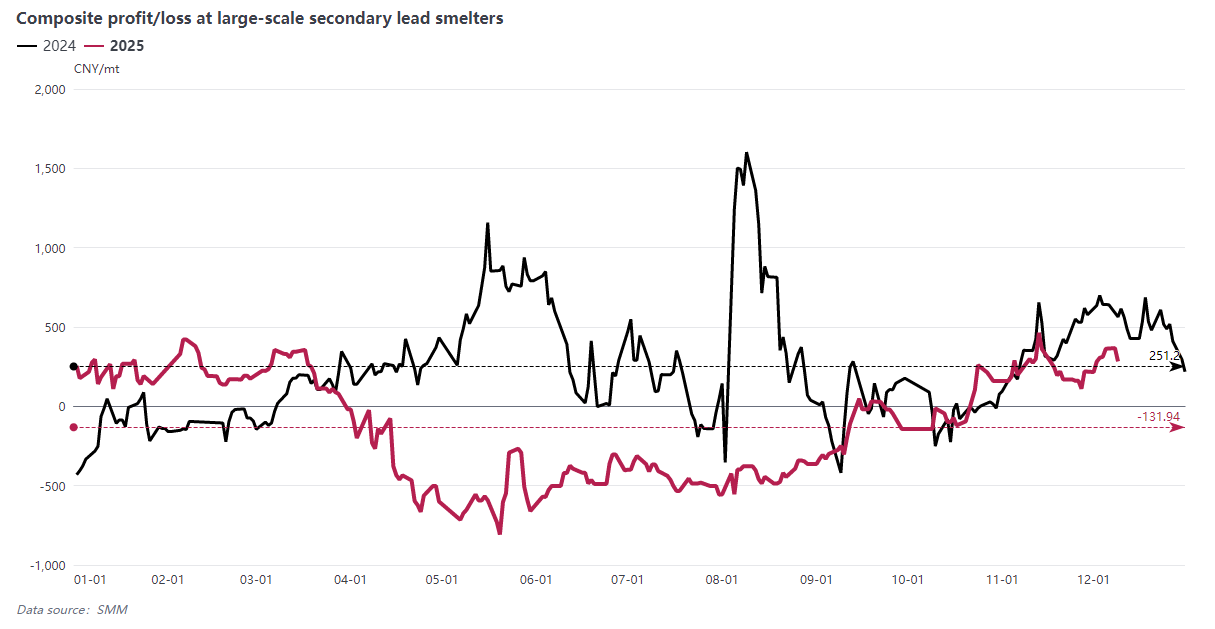

In 2025, the fluctuation range of lead prices narrowed YoY, with the SMM average price of secondary refined lead decreasing by 219.3 yuan/mt compared to 2024, a decline of approximately 1.28%. At the same time, the price of raw material waste lead-acid batteries remained high, putting significant pressure on the profitability of secondary lead smelting.

According to SMM data, the average annual comprehensive profit/loss of large-scale secondary lead enterprises fell by about 154% compared to 2024, indicating considerable operational pressure across the industry. It is worth noting that the by-product revenue in SMM's comprehensive profit/loss model for large-scale secondary lead enterprises only includes common by-products from smelters.

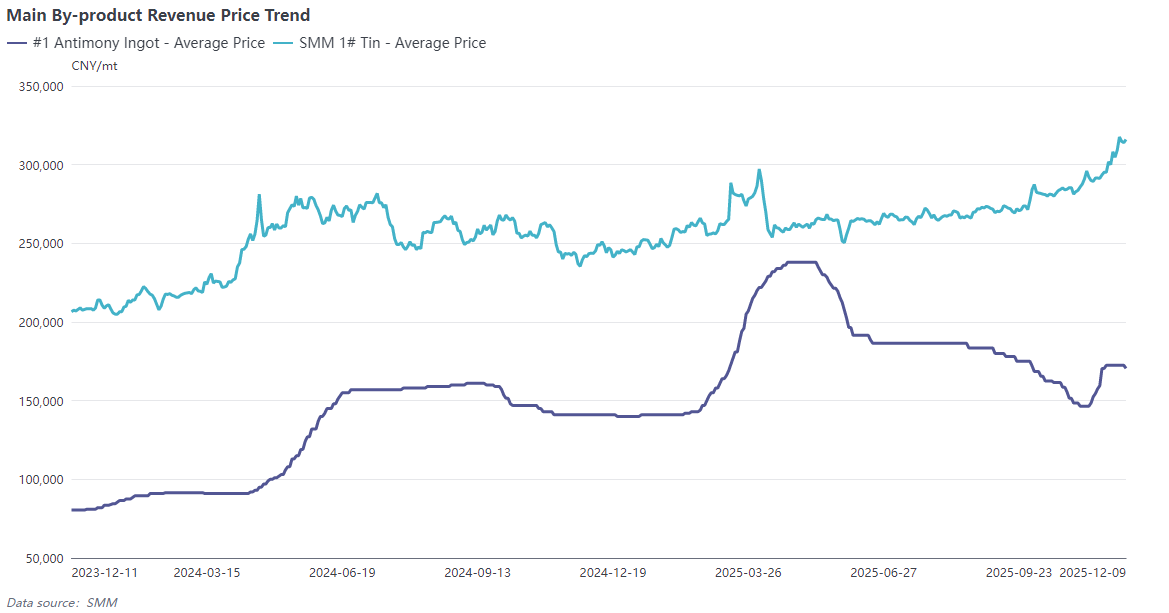

However, secondary lead enterprises with multi-metal comprehensive recovery capabilities, by extracting high-value metals such as antimony and tin, can effectively offset losses from the lead smelting process. The profit performance of such enterprises is significantly better than that of smelters with fewer types of by-products.

Looking ahead to 2026, lead prices are expected to continue fluctuating considerably. Although the price of raw material waste lead-acid batteries is anticipated to decline, the decrease is likely to be limited, while prices of by-product metals such as antimony and tin are expected to remain well-supported. If secondary lead capacity can be optimized and reduced, the supply-demand relationship in the industry may improve. Overall, driven by multiple factors including capacity optimization, technological upgrades, and support from by-product prices, there is room for improvement in the profitability of the secondary lead industry in 2026. However, the divergence in performance among enterprises may further intensify.

![LME Lead Bottomed Out, While SHFE Lead Retreated After Rapid Rise and Consolidated [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/EhsCj20251217171721.jpeg)

![Tight Warehouse Supply in Jiangsu, Zhejiang, and Shanghai, Stronger Support From Firm Spot Price Offers [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)