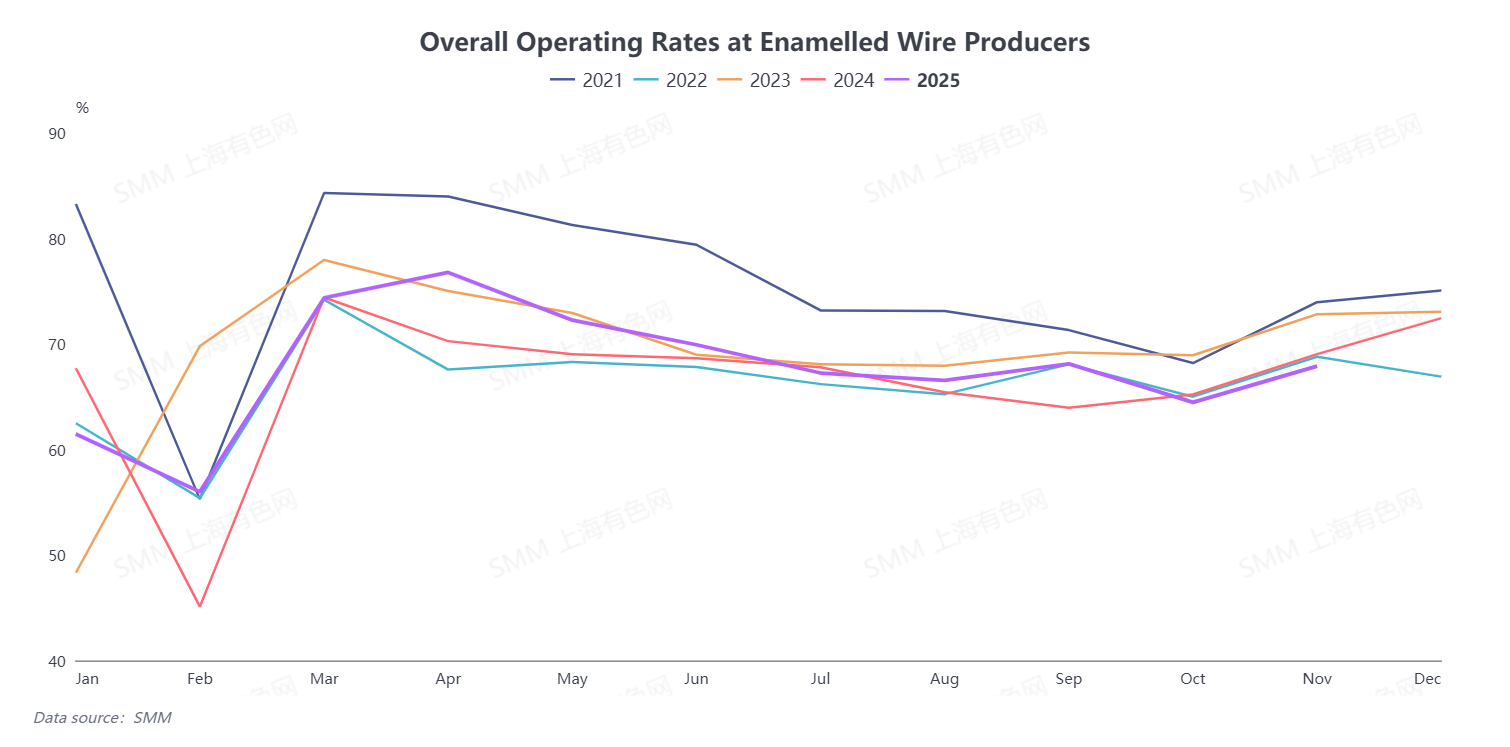

According to SMM, the comprehensive operating rate of the enamelled wire industry in November was 67.91%, up 3.44 percentage points MoM, but down 1.33 percentage points YoY. Among them, the operating rate of large enterprises was 68.38%, that of medium-sized enterprises was 66.05%, and that of small enterprises was 69.29%.

The operating rate of the enamelled wire industry rebounded as expected in November, with core driving factors showing multi-dimensional support characteristics. On one hand, disruptions from the National Day holiday completely subsided, and enterprises gradually returned to normal production pace, laying the foundation for the recovery of the operating rate. On the other hand, the pullback in the center of copper prices triggered a phased release of demand, coupled with marginal improvement in downstream market acceptance of high copper prices, directly driving a steady increase in order volumes. In terms of end-use demand structure, sectors such as NEV and power transformers performed strongly, while orders from the home appliance sector also showed signs of recovery, providing supplementary support for the industry's recovery. Overall, the enamelled wire market exhibited a weak recovery in November, without showing the robust scene typical of the traditional peak season.

In terms of finished product inventories, the industry's days of inventories for finished products in November stood at 11.82 days, down 0.71 days from October. Against the backdrop of high copper prices, enamelled wire enterprises continued the business strategy of "producing based on demand and prioritizing inventory reduction," coupled with marginal improvement in end-use demand. Although inventories remain at a relatively high level, overall pressure has eased somewhat.

SMM expects the comprehensive operating rate of the enamelled wire industry to edge up 0.48 percentage points MoM to 68.38% in December, but decrease 4.21 percentage points YoY. According to SMM, most enterprises tend to close the year steadily at the year-end stage. On one hand, there are no plans for large-scale production pushes, and on the other hand, efforts to control accounts receivable risks continue to strengthen. The core driver supporting the slight rebound in the operating rate mainly comes from marginal improvement in orders from the home appliance sector, with related order increments providing some support for industry production. However, current copper prices have climbed to a high of 91,000 yuan/mt, with a price difference exceeding 2,000 yuan/mt compared to the time of the survey. The recent decline in end-use orders is quite noticeable, and this factor will directly impact actual enterprise production. It is likely difficult for the enamelled wire industry's operating rate to sustain the rebound trend in December. Subsequent attention should continue to be paid to copper price fluctuations and the release of end-use demand.