SMM December 6:

Mixed trends in supply and demand! Domestic aluminum billet supply-side operating performance remained generally stable in November, with the final production figure meeting off-season expectations. As the September-October peak season concluded, some aluminum billet enterprises planned ahead to switch production to aluminum bus bars, primary alloys, aluminum rods, and other products. Additionally, some group enterprises, due to poor overall annual performance, implemented marginal production cut adjustments in November, showing signs of supply contraction during the off-season. However, due to the stronger-than-expected performance of aluminum billet processing fees, particularly in south China, some billet plants in south-west China increased production accordingly. Coupled with some newly commissioned capacities entering the ramp-up phase in Q4, domestic aluminum billet supply achieved a temporary stable transition amid mixed trends. The daily average production of primary aluminum billets in November pulled back slightly to around 50,000 mt/day MoM, in line with previous expectations. However, SMM expects that as the off-season deepens in December and high aluminum prices further suppress processing fees and downstream demand, enterprise inventory and capital pressures will intensify. Some enterprises already have plans for sizable production cuts, and daily average production is expected to continue pulling back to 48,000 mt/day.

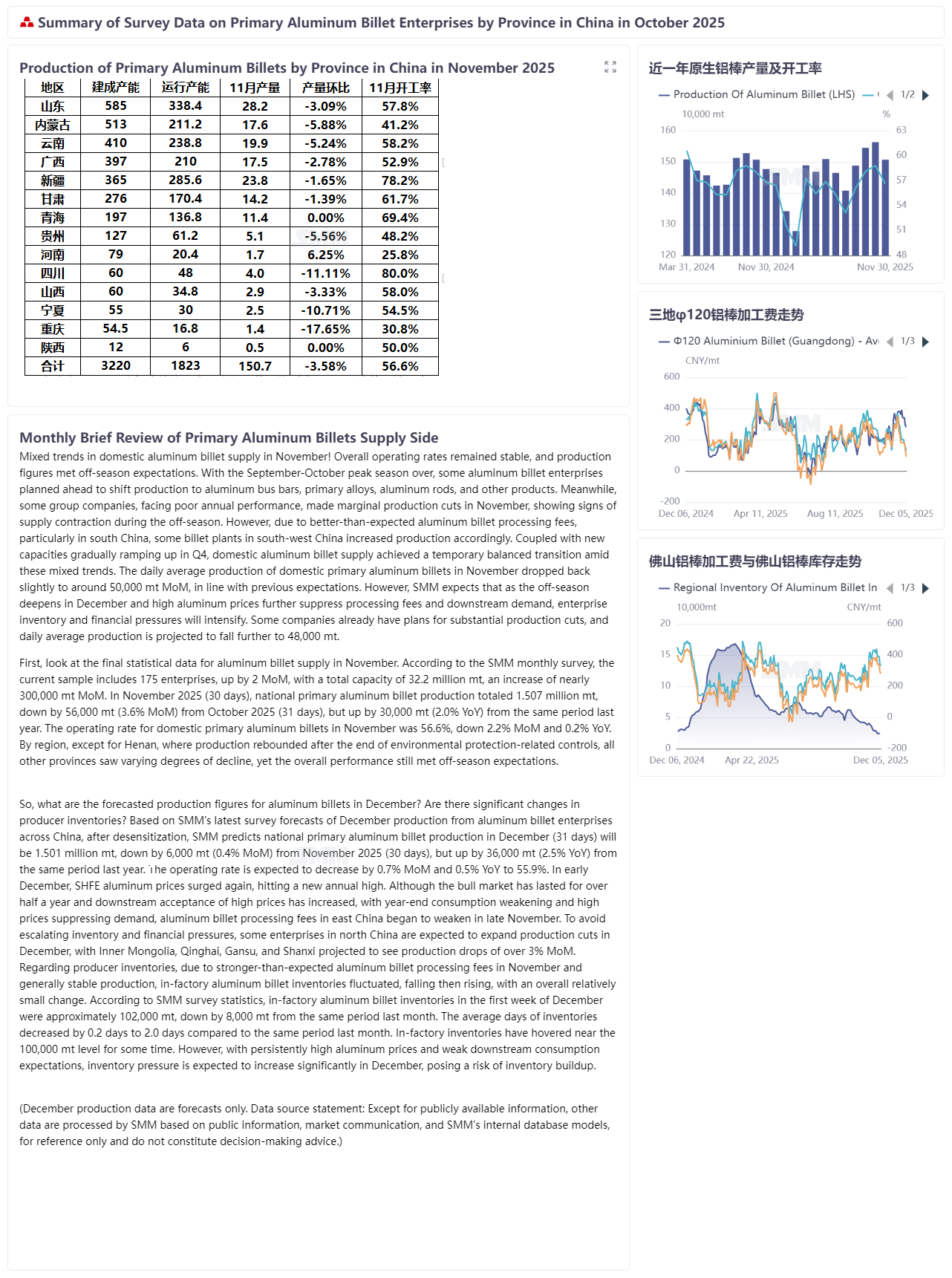

First, looking at the final statistics for aluminum billet supply in November. According to the SMM monthly survey, the current sample for the monthly primary aluminum billet survey includes 175 enterprises, an increase of 2 from the previous month, with total capacity of 32.2 million mt, an increase of nearly 300,000 mt MoM. National primary aluminum billet production in November 2025 (30 days) totaled 1.507 million mt, down 56,000 mt MoM from October 2025 (31 days), a decrease of 3.6%, but up 30,000 mt YoY, an increase of 2.0%. The domestic operating rate for primary aluminum billets in November was 56.6%, down 2.2% MoM and down 0.2% YoY. By region, except for Henan, where production rebounded against the trend after the end of environmental protection-related controls, production in other provinces declined to varying degrees, but the overall performance remained in line with off-season expectations.

So, what are the predicted values for aluminum billet production in December? Have there been significant changes in producer inventory? According to the latest predictive survey by SMM on the production plans of domestic aluminum billet enterprises by province for December, after desensitization, SMM forecasts national primary aluminum billet production in December (31 days) to be 1.501 million mt, down 6,000 mt MoM from November 2025 (30 days), a decrease of 0.4%, but up 36,000 mt YoY, an increase of 2.5%. The operating rate is expected to decrease 0.7% MoM and 0.5% YoY to 55.9%. In early December, SHFE aluminum prices surged again, reaching a new annual high. Although the bull market has persisted for over half a year and downstream acceptance of high prices has increased, with year-end consumption weakening and high prices exerting pressure, aluminum billet processing fees in east China began to weaken in late November. Some aluminum billet enterprises in north China, aiming to avoid escalating inventory and capital pressure, are expected to expand production cuts. Inner Mongolia, Qinghai, Gansu, and Shanxi are all forecast to see production declines exceeding 3% MoM in December. Regarding in-factory inventory, due to stronger-than-expected aluminum billet processing fees in November while production remained generally stable, in-factory aluminum billet inventory initially fell then rose during the month, with an overall relatively small change. According to SMM survey statistics, domestic aluminum billet in-factory inventory in the first week of December was approximately 102,000 mt, down 8,000 mt from the same period last month. The average days of inventory decreased by 0.2 days to 2.0 days compared to the same period last month. In-factory inventory has been around the 100,000 mt level for some time. Given persistently high aluminum prices and weak downstream consumption expectations, inventory pressure for aluminum billets in factories is expected to increase significantly in December, with a risk of inventory buildup. (December production data are forecast values only. Data source statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.)