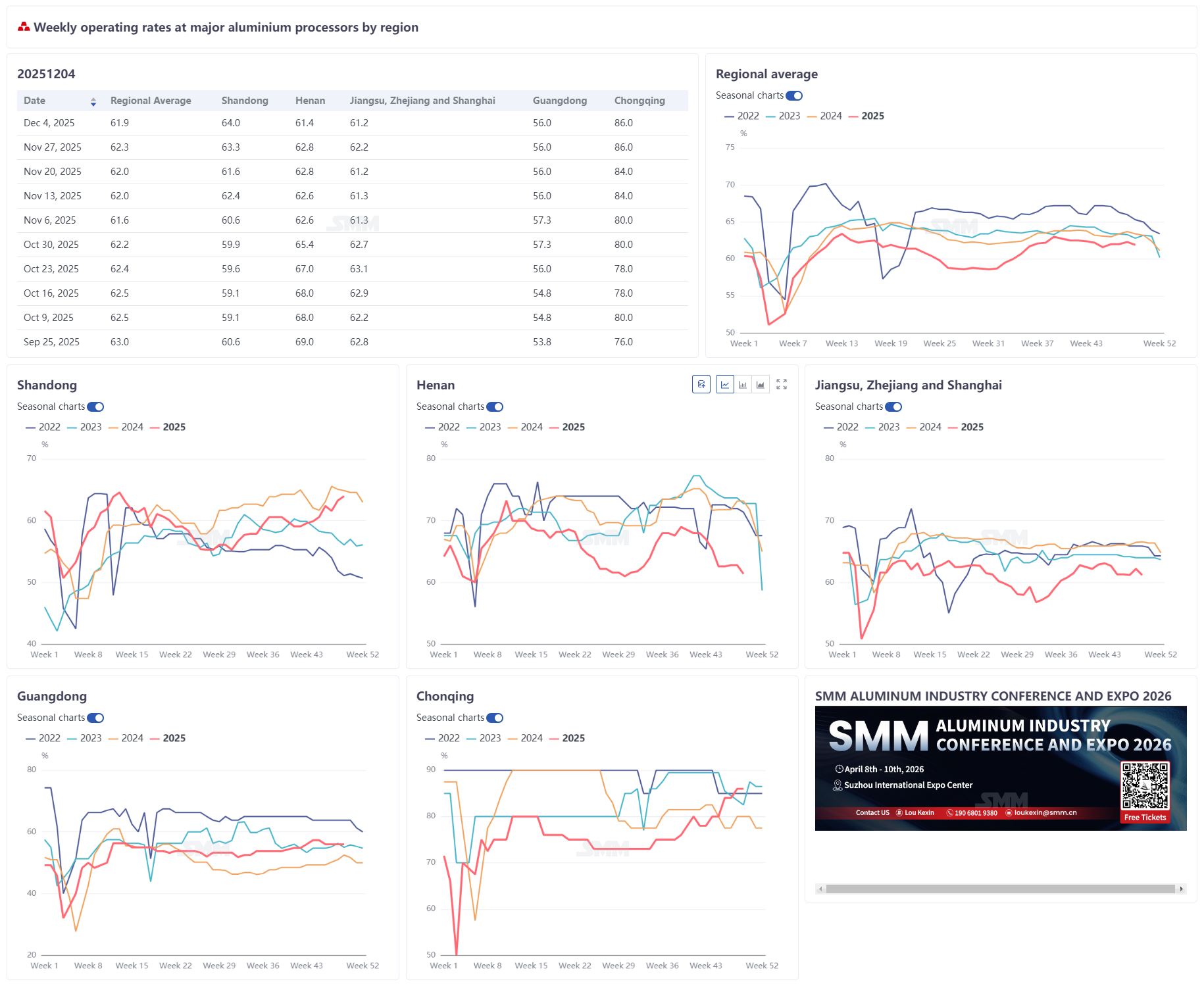

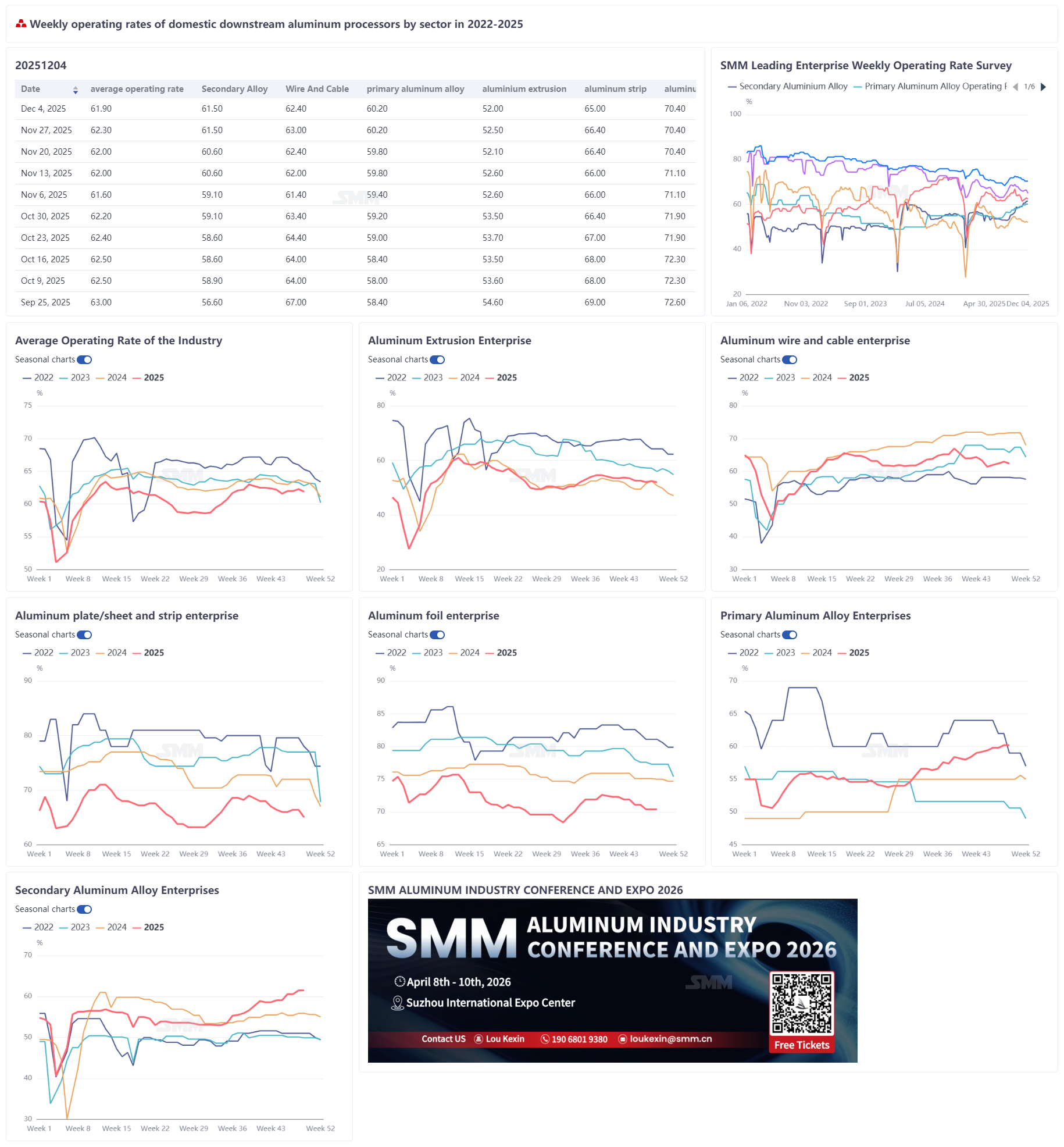

December 4, 2025:

The weekly operating rate of leading domestic aluminum downstream processing enterprises fell 0.4 percentage points WoW to 61.9%, with the market continuing to show structural divergence. The operating rate of primary aluminum alloy remained stable at 60.2%, as long-term contract deliveries at major enterprises were steady, but high aluminum prices suppressed spot order transactions, with cautious demand side sentiment. The operating rate of aluminum wire and cable pulled back 0.6 percentage points to 62.4%; although supported by power grid orders, insufficient cargo pick-up continuity coupled with weak year-end stockpiling willingness constrained the rebound in operating rates. The operating rate of aluminum extrusion edged down 0.5 percentage points to 52.0%, with construction-grade extrusions remaining sluggish and reduced production schedules in the PV sector dragging on industrial-grade materials, while only automotive and ESS extrusions remained stable. The operating rate of aluminum plate/sheet and strip dropped 1.4 percentage points to 65.0%, pressured by intensified environmental protection-driven production restrictions in Henan and other regions and high aluminum prices, leading to a noticeable decline in construction and packaging orders; although can stock processing fees are expected to increase, this is unlikely to reverse the overall weakness. The operating rate of aluminum foil was recorded at 70.4%, with traditional air-conditioner foil and decorative foil demand weakening, while single-zero packaging foil received slight support from year-end stockpiling, and new energy products such as battery foil provided limited incremental demand. The operating rate of secondary aluminum producers held steady at 61.5%, with leading plants maintaining high utilization rates due to sufficient orders, but small and medium-sized producers faced constraints on capacity release due to high aluminum scrap costs and production cuts at die-casting plants. SMM expects the sector's operating rates to continue weakening in the short term, with rates likely to remain weak and consolidate as the off-season deepens and high aluminum prices persist.

Primary aluminum alloy: The primary aluminum alloy industry operated steadily this week, with the operating rate unchanged WoW at 60.2%. Supply side, long-term contract deliveries remained stable, production pace was continuous, and the overall supply landscape showed no significant fluctuations. Demand side, influenced by high aluminum prices, downstream enterprises primarily focused on fulfilling long-term contracts, while spot order purchase willingness was generally cautious, and wait-and-see sentiment prevailed. According to the SMM survey, spot order transaction activity was limited this week, and demand weakened slightly WoW, but the impact on overall industry production schedules was relatively small. Overall, the current market is characterized by stable supply and slow demand. In the high aluminum price environment, downstream purchases have become more rational. It is expected that the industry will continue to operate steadily in the short term, with price fluctuations remaining a key variable affecting the market pace. Aluminum Plate/Sheet and Strip: The operating rate of leading enterprises in aluminum plate/sheet and strip fell 1.4 percentage points WoW to 65.0% this week. On the enterprise operation front, environmental protection-driven production restrictions reemerged in central China. Approaching year-end, air pollution control tasks intensified in Gongyi, Changge, Luoyang, and other areas of Henan, significantly limiting production and transportation, directly impacting local enterprises' production and delivery efficiency. Coupled with constraints from insufficient orders, even if some enterprises attempted to resume production lines, a full production resumption was difficult. Aluminum prices surged rapidly above 22,000 yuan/mt this week, up over 500 yuan/mt WoW. High aluminum prices intensified enterprises' fear of high prices in raw material procurement and finished product shipments, dampening downstream enthusiasm for cargo pick-up and putting overall demand under further pressure. Structural differences in industry orders were significant, with continuous declines in construction and packaging sectors; the curtain wall downstream planned early production cuts wrap-up in December due to poor financial conditions. For can stock, processing fee increase negotiations advanced and have already been transmitted to end-user beverage consumption ahead of time, with results expected soon, but actual demand is unlikely to see substantial improvement before the Chinese New Year. Looking ahead to next week, as the off-season deepens, with environmental protection-related controls and aluminum price rise risks coexisting, and orders lacking strong support, the industry operating rate will continue to contract, with no substantial improvement expected in the short term.

Aluminum Wire and Cable: The weekly operating rate for aluminum wire and cable fell 0.6 percentage points WoW to 62.4% this week, ending the previous mild rebound trend. The decline was mainly due to hindered winter project construction progress, weakened expectations for sustained power grid cargo pick-up, coupled with low year-end stockpiling willingness among enterprises, maintaining only normal delivery pace production. From an enterprise operation perspective, feedback from Hebei and Jiangsu indicated limited and unsustainable new matched power grid orders last month, providing weak support; enterprises in Shandong reported tight schedules for overseas EPC projects, with export orders maintaining rigid demand; manufacturers in Sichuan noted good performance in export orders, with orders on hand lasting until March next year. Looking ahead to next week, although export orders show a good trend, domestic enterprises are constrained by high aluminum price fluctuations suppressing downstream operations, persistently weak year-end stockpiling willingness, and no significant order volume increase. The aluminum wire and cable operating rate is expected to continue weak consolidation in December. Aluminum Extrusion: The overall operating rate for the domestic aluminum extrusion industry this week was 52%, down 0.5 percentage points WoW, mainly affected by a decline in orders from the PV sector. In the construction extrusion segment, performance varied across the industry. Some medium and large enterprises in Shandong and Zhejiang maintained stable operating rates supported by export orders, while some small enterprises in central China operated at low levels, with the overall construction sector remaining sluggish. For industrial extrusion, PV extrusion was impacted by reduced downstream module production schedules, dragging down the industry's operating rate. Leading enterprises implemented relatively small production cuts, while some small and medium-sized PV frame manufacturers in east China saw their operating rates drop to 20%–30%. Automotive extrusion, ESS extrusion, and other industrial extrusion segments operated relatively steadily. SMM will continue to monitor order changes across various segments.

Aluminum Foil: The operating rate for leading aluminum foil enterprises this week was 70.4%. On the enterprise operation side, as the off-season deepened, demand for traditional products such as air-conditioner foil and decorative foil continued to decline, and leading enterprises saw a simultaneous reduction in orders on hand. Coupled with inventory and capital pressure from previous high aluminum prices, as well as fear of high prices triggered by aluminum prices breaking through 22,000 yuan/mt this week, production pace faced multiple constraints. On the other hand, consumption of single-zero packaging foil improved significantly compared to the summer period. As year-end approached, end-users began stockpiling, and some enterprises launched year-end production sprint plans in December. In the short term, weak demand in traditional consumption areas is difficult to reverse, and upward risks for aluminum prices remain. Only demand for battery foil and brazing foil in the new energy sector provides limited support. The industry's operating rate is expected to remain stable, lacking strong upward momentum in the near term.

Secondary Aluminum: The operating rate for leading secondary aluminum enterprises this week remained stable at 61.5%. Currently, leading enterprises have sufficient orders and maintained high production levels. However, the industry as a whole faces multiple constraints. First, aluminum prices surged to a yearly peak in December, dampening downstream willingness to pick up goods. Some die-casting plants saw compressed profit margins due to high raw material costs, even incurring losses, leading to lower operating rates which in turn affected orders for secondary aluminum producers. Second, aluminum scrap prices rose significantly along with aluminum prices during the week, and copper prices on the auxiliary material side broke a new high of 91,245 yuan/mt, exacerbating the risk of losses. In the short term, leading enterprises are expected to maintain high output thanks to their order advantages, but small and medium capacities may continue to shrink, and structural differentiation within the industry is likely to persist.