- SMM Cold Rolling Production Schedule: Cold Rolling Production at Steel Mills Slightly Decreased in December

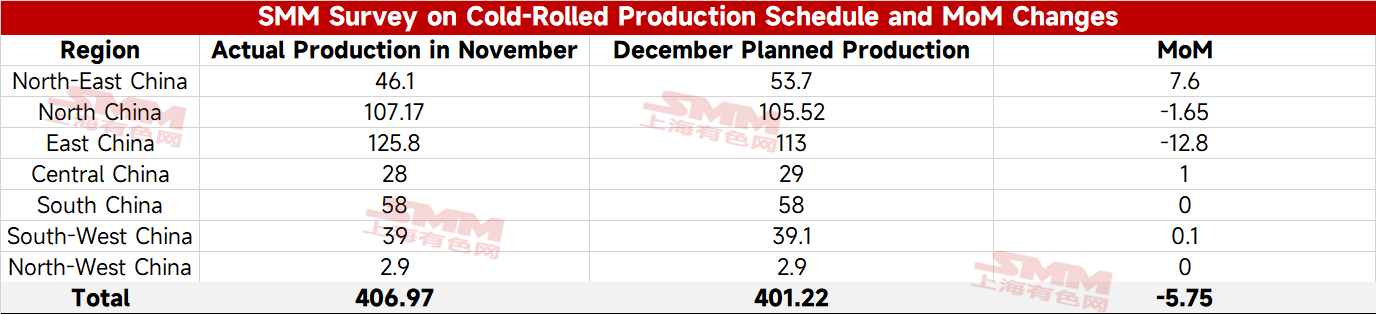

According to the latest SMM tracking, the planned volume of commercial cold-rolled sheet and strip from 31 mainstream steel mills totaled 4.0122 million mt this month, down 57,500 mt MoM from the actual production of commercial cold-rolled materials in the previous month, a decrease of 1.4%.

On a daily average basis, with December having one more day than November, the daily average production schedule for commercial cold-rolled materials in December was 129,400 mt, down 4.6% MoM from the daily average actual production of commercial cold-rolled materials in the previous month.

- SMM HRC Production Schedule: December HRC Production Down 2% MoM, Daily Average Down 5%

According to the latest SMM tracking, the planned HRC commodity output from 39 mainstream steel mills totaled 13,570,500 mt this month, down 279,800 mt MoM from the actual HRC commodity production last month, a decrease of 2.0%.

On a daily average basis, with December having one more day than November, the daily average HRC commodity production schedule this month was 437,800 mt, down 5.2% MoM from the daily average actual HRC commodity production last month.

Domestic Trade: This month's HRC domestic trade production schedule was 12.4135 million mt, down 369,800 mt MoM from the actual domestic production last month, a decrease of 2.9%. On a daily average basis, December has one more day than November. This month's sample steel mills' average daily HRC domestic trade production schedule was 400,400 mt, down 6.0% MoM from the average daily actual commodity HRC production last month.

Summary: In December, the production schedule for hot-rolled products at steel mills decreased 2.0% MoM. Due to the fact that December has more days than November, the daily average production schedule for hot-rolled products actually decreased 5.2% MoM from the previous month's actual output. Affected by maintenance at multiple steel mills in the north, east China, and central China, hot-rolled coil production is expected to decline MoM, potentially easing supply pressure.

Demand side, entering the off-season, construction and machinery industry activities are expected to gradually weaken. As for the home appliance sector, according to the latest production schedule report for the three major white goods released by ChinaIOL, the total planned production of air conditioners, refrigerators, and washing machines in December 2025 is 30.18 million units, down 14.1% YoY. Regarding the automotive industry, as the final month of the year, with the tail-end effect of policies and the year-end sales push, demand in the automotive sector is expected to maintain strong resilience. Overall, under the backdrop of the off-season, steel consumption release is under pressure, and the demand for sheets & plates in December is expected to slightly decrease compared to November, with inventory likely to continue declining, albeit at a slower pace than in the same period in previous years.

In other aspects, as the opening year of the "14th Five-Year Plan," recent macro expectations have significantly warmed up. Influenced by this, there is an opportunity for hot-rolled coil prices to rise at the end of the year. However, against the backdrop of high inventory, actual demand from end-users remains mainly purchasing as needed, making it difficult for prices to resonate strongly between macro and industry trends. It is expected that the price center for cold-rolled and hot-rolled products will move up MoM in December, but the increase will be limited.

![[SMM Hot-Rolled Arrivals] Arrivals in Major Mainstream Markets Pulled Back in the First Week After the Holiday](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)